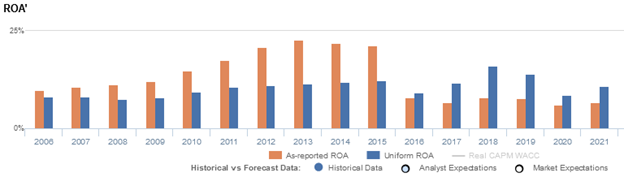

This brick-and-mortar store continues to thrive even in the digital era, with Uniform ROAs greater than what is reported

With the shift towards a more digital world, consumers have been inclined to rely more on the internet and their devices to do their activities from the comfort of their own homes. Online stores have become more prominent, especially during the pandemic, and brick-and-mortar stores who can’t keep up may find it hard to survive.

However, this brick-and-mortar store is still attracting customers and continuously expanding amidst the online retail revolution. Although as-reported data suggests that this company’s initiatives are not enough against e-commerce, Uniform Accounting shows us otherwise, with Uniform ROAs that are higher than as-reported ROAs in the past six years.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

In 2017-2018, major apparel and specialty retailers filed for bankruptcy and store closures as online retailers, particularly Amazon, boomed and started getting more traction. Among some of the retailers that struggled to compete with e-commerce include Toys R Us, Sears Holdings, Claire’s, Nine West, and more.

The pandemic has also dramatically changed the scene of online shopping, heightening the digital evolution around the globe. Businesses have been compelled to drive digital transformations, and consumer behavior has also been patterned after the At-Home Revolution.

Specifically, consumers have been more reliant on the internet for news, information, and entertainment. So even with brick and mortar retailers slowly recovering from government-imposed lockdown and restrictions, consumers are already inclined towards e-commerce due to its convenience and safety.

However, Dollar Tree, Inc. (DLTR) has managed to thrive as a brick-and-mortar store amidst the online retail revolution, thanks to its low-cost goods and its unique shopping experience.

Dollar Tree, formerly known as Only $1.00, is an American discount variety store company known for selling goods that cost only $1 or even less. The company’s business model is catered towards low-income households, but it has also enticed middle class consumers.

Furthermore, the company is able to compete with larger rivals like Walmart and Amazon because consumers are attracted not only to its low prices, but also the “treasure hunt” shopping experience it gives. It’s really just a different experience rummaging through aisles and not knowing what you will check out at the end of the day.

The rise of e-commerce has barely affected Dollar Tree’s business because customers are able to save on shipping costs. While it makes sense to order online for bulk purchases, the same cannot be said when people want to purchase items worth less than $10.

Currently, the company continues to open hundreds of stores, having more than 15,000 retail outlets all over the U.S. and Canada.

While much of the dollar store’s growth is organic, a considerable portion is also attributed to Dollar Tree’s consolidation-through-acquisition efforts.

Specifically, in 2015, Dollar Tree acquired fellow leading discount retailer Family Dollar, which also focuses on selling inexpensive discretionary goods, such as household cleaners, apparel, and other items targeted for families and households.

Initially, Dollar Tree has had some challenges realizing the synergies from the acquisition. In response to this, the company laid out a turnaround strategy to close down underperforming Family Dollar stores and renovate or rebrand hundreds of Family Dollar chains to the Dollar Tree banner.

Recently, Dollar Tree announced its renovation strategy for Family Dollar and Dollar Tree Combo Stores. The renovation efforts aim to better serve consumers while also improving the company’s margins and store productivity.

Additionally, the company launched Dollar Tree Plus!, offering products that are more than $1 and promoting “more choices, more sizes, and more savings” for consumers. Having these higher-priced products can help Dollar Tree offer diversification and a broader range of products for its customers.

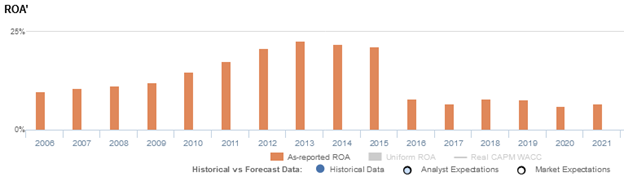

However, even with these strategic expansions and offerings, it appears that Dollar Tree is still struggling to compete with online retailers, with return on assets (ROA) dropping from 21% in 2015 to 6%-8% levels through 2021.

In reality, Uniform Accounting paints a completely different picture, with Uniform ROAs being sustained at 11%-12% levels in the same timeframe. This shows that even though the pandemic has created long-lasting consumer buying patterns towards e-commerce, there is still an allure to stores like Dollar Tree.

The distortion comes from as-reported metrics failing to consider the number of operating leases Dollar Tree has from its stores.

The decision management makes between investing in capex and investing in a lease is based on how management wants to finance their investments. Choosing to lease an asset, however, would not be treated as an investment, but as an expense that would impact the income statement.

Specifically, operating leases on Dollar Tree’s income statement are understating the company’s true earnings. Adjusting for the rent expense distortion, which historically has been about one-fifth of its total operating expenses, returns are actually stronger.

As a result, as-reported ROAs are not capturing the strength of Dollar Tree’s earning power. Adjusting for operating leases, we can see that the company’s profitability isn’t as weak as it seems, with Uniform ROAs at 10%+ in recent years.

Dollar Tree is actually more profitable than you think it is

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

Dollar Tree’s Uniform ROA has actually been higher than its as-reported ROA in the past six years. For example, Uniform ROA is at 11% in 2021, while as-reported ROA is only at 7%.

Specifically, Dollar Tree’s Uniform ROA has ranged from 9%-16% in the past six years while as-reported ROAs were only at 6%-8% levels in the same timeframe.

Uniform ROA gradually improved from 8% levels in 2006 to 12% levels in 2013-2015, before compressing to 9% in 2016 and rebounding to a peak of 16% in 2018. Then, Uniform ROA fell back to 9% in 2020 before increasing to 11% in 2021.

Dollar Tree’s Uniform earnings margin is weaker than you think, but its Uniform asset turns make up for it

Trends in Uniform ROA have been driven primarily by trends in Uniform earnings margin, coupled with stable Uniform asset turns.

After ranging from 5%-6% levels in 2006-2009, Uniform margins expanded to 9% levels in 2013-2015, before fading to 7% levels in 2016-2017. Thereafter, Uniform margins recovered to a high of 10% in 2018, before declining to 6% in 2020 and improving to 8% in 2021.

Meanwhile, Uniform turns remained at 1.3x-1.6x levels since 2006 and currently sits near the lower end of that range.

At current valuations, the market is pricing in expectations for Uniform margins to decline, accompanied by continued stability in Uniform turns, which seems overly pessimistic given the firm’s progress in integrating Family Dollar.

SUMMARY and Dollar Tree, Inc. Tearsheet

As the Uniform Accounting tearsheet for Dollar Tree, Inc. (DLTR:USA) highlights, the Uniform P/E trades at 21.7x, which is below the global corporate average of 23.7x but around its historical Uniform P/E of 20.7x.

Low P/Es require low EPS growth to sustain them. In the case of Dollar Tree, the company has recently shown a 43% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Dollar Tree’s Wall Street analyst-driven forecast is a 7% EPS shrinkage in FY2022 and a 7% EPS growth in FY2023.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Dollar Tree’s $115 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to have little or no growth over the next three years. What Wall Street analysts expect for Dollar Tree’s earnings growth is below what the current stock market valuation requires in 2022 but above that requirement in 2023.

Furthermore, the company’s earning power is 2x the corporate average. Also, cash flows and cash on hand are 2x higher than its total obligations—including debt maturities and capex maintenance. Together, this signals a low credit risk.

To conclude, Dollar Tree’s Uniform earnings growth is below its peer averages. However, the company is trading in line with average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com