This company has proven that the odds of winning in the gaming equipment business is high with the right partners, reaching Uniform ROAs of 26%+

“It only takes one lucky ticket to win it all”—a famous line people usually make when betting on their chosen lottery numbers.

This company leveraged that mentality and succeeded by putting all of its efforts into leasing its equipment and service, particularly to the country’s main government-controlled gaming corporation. However, looking at its as-reported metrics, it seems that mainly focusing on this business hasn’t been producing stellar returns.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

The lottery in some form or the other has been a part of the Philippine culture as early as the Spanish occupation. The first draw reportedly took place in 1851 under the patronage of the Empresa de Reales Loteria Españolas de Filipinas. With the amount of revenue the Spanish government was able to generate from it, the venture was deemed a success.

However, lottery activities were abruptly stopped due to the Spanish-American war in 1898. It was revived in 1932 by the American Insular government to gather funds for young Filipino athletes through the Philippine Amateur Athletic Federation (PAAF).

Since then, the game has become an unstoppable phenomenon in the country. Everywhere you go, you’ll see men and women lining up in front of lotto outlets, willing to bet away their fortunes in the hopes of gaining more fortune.

Just like its main regulator in the Spanish era, the lottery is managed by the government. Specifically, all lottery draws are under the guidance of the Philippine Charity Sweepstakes Office (PCSO)—an organization created by the Philippine legislature in 1934 to promote public health and welfare.

PCSO’s continued success in the segment led it to eventually go digital and launch its very first online lottery in 1995 through an Equipment Lease Agreement (ELA) with Pacific Online Systems Corporation (LOTO:PHL).

Established in 1993, Pacific Online Systems is involved in the development and management of online computer systems and terminals for the gaming industry.

The company’s deal with PCSO was the big break it needed. Due to this, Pacific Online Systems was able to open thousands of terminals all over the Philippines, strengthening its geographic presence in the country.

In addition, Pacific Online Systems also provided leasing equipment and gaming systems for the Keno games nationwide through Total Gaming Technologies.

Seeing that its leasing business accounts for 77% of its total revenue, the company’s focus on this segment has indeed brought it luck.

To further grow its business, Pacific Online Systems partnered with Scientific Games Corporation in 2005 and Intralot in 2006, which are considered as two of the best technology leaders in the global lottery and gaming industry. By doing so, Pacific Online Systems was able to increase its number of terminals and obtain a more effective lottery system, further improving its odds in the sector.

On top of that, Premium Leisure Corporation (PLC)—a subsidiary of Belle Corporation (BEL:PHL) that primarily focuses on the gaming industry—acquired a 50.1% stake of Pacific Online Systems from its parent company. This alone opened new expansion opportunities for the business.

While these milestones and achievements make it seem like the company had won the winning ticket with its business, Pacific Online Systems’ most challenging obstacle was yet to come.

In 2019, President Duterte suspended all lotto and keno operations in the third quarter of the year due to accounts of “massive corruption”. As a result, PCSO’s main equipment lessor Pacific Online Systems’ revenues dropped 49% from PHP 1.9 billion to only PHP 990 million.

Prior to the unexpected suspension, being the sole supplier of the most heavily controlled gaming corporation had its perks.

Taking its outlier 2019 performance off the picture, one would correctly think that Pacific Online Systems’ focus on its leasing business has historically helped the company fortify its position in the industry.

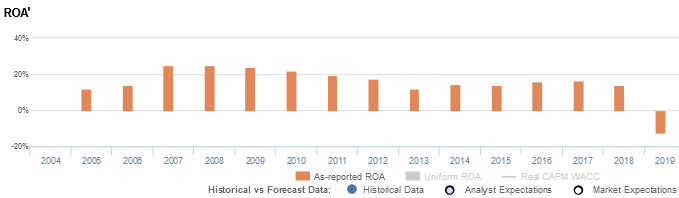

However, as-reported metrics make it seem like the company’s leasing activities are not up to par—with return on assets (ROAs) only ranging from 12% to 25% over the past fourteen years, or an average of 17%.

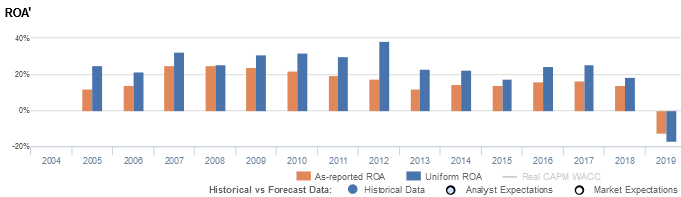

In reality, the company’s ability to mainly capitalize its gaming equipment business historically has actually led to strong returns, with Uniform ROAs ranging from 18% to 38%, or an average of 26%, far above as-reported numbers.

One of the said distortions for the discrepancy is due to the treatment of non-operating long-term investments according to the Philippine Financial Reporting Standards (PFRS).

Based on PFRS, non-operating long-term investments are part of the company’s balance sheet, but in reality, non-operating long-term investments are not essential to the firm’s assets and should be removed from the total assets.

For example, in 2018, Pacific Online Systems recognized a non-operating long-term investment of PHP 456 million, accounting for 22% of its as-reported total assets of PHP 2.1 billion.

After removing the PHP 456 million from the asset base and with the many other adjustments Valens makes, we arrive at a TRUE earning power of 18%.

Pacific Online Systems’ earning power is generally stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think Pacific Online Systems’ profitability has been weaker than real economic metrics have highlighted in fifteen of the past fourteen years.

In reality, Pacific Online Systems’ true profitability has generally been higher than as-reported ROA since 2005, excluding the decline in 2019. Specifically, Uniform ROA was 18% in 2018, but as-reported ROA was only 14% that year.

As-reported ROA has improved from 12% in 2005 to 25% levels in 2007-2008, before declining to 12% in 2013 and subsequently expanding to 17% in 2017. Since then, as-reported ROA declined massively to -13% in 2019.

Meanwhile, after expanding from 25% in 2005 to 32% in 2007, Uniform ROA declined to 26% levels in 2008 and improved to a peak of 38% in 2012. Thereafter, Uniform ROA compressed to 18% in 2015, before expanding to 26% in 2017 and falling to negative levels in 2019.

Pacific Online Systems’ earnings margin is generally weaker than you think

Trends in Uniform ROA have been primarily driven by trends in Uniform earnings margin.

As-reported margins improved from 24% in 2005 to 55% in 2007, before fading to 34% in 2013 and subsequently recovering to 41% levels in 2016. Since then, as-reported margins have declined to negative levels in 2019.

Meanwhile, Uniform margins expanded from 23% in 2005 to 29% in 2007, before compressing to 13% in 2013 and rebounding to 23% in 2017. Since then, Uniform margins have regressed to -32% in 2019.

Looking at the firm’s margins alone, as-reported metrics are making the firm appear to be a more cost efficient business than is accurate.

SUMMARY and Pacific Online Systems Corporation Tearsheet

As the Uniform Accounting tearsheet for Pacific Online Systems Corporation (LOTO:PHL) highlights, it trades at a Uniform P/E of -5.1x, below the global corporate average of 25.2x and its historical average of -3.2x.

Average P/Es require average EPS growth to sustain them. In the case of Pacific Online Systems, the company has recently shown 185% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Pacific Online Systems’ sell-side analyst-driven forecast calls for a 7% Uniform EPS growth in 2020 and a 1% Uniform EPS shrinkage in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Pacific Online Systems’ PHP 2.11 stock price. These are often referred to as market embedded expectations.

Furthermore, the company’s earning power is below the long-run corporate average, and cash flows and cash on hand are also below total obligations—including debt maturities, capex maintenance, and dividends, with intrinsic credit risk 400bps above the risk free rate. Together, this signals a moderate credit risk.

To conclude, Pacific Online Systems’ Uniform earnings growth is in line with its peer averages, and the company is trading in line with its peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com