This company helps satisfy your sweet tooth, but after all that it’s milled, it’s only reaping a TRUE earning power of 3%.

At various points in history, countries were defined by their top commodity export. The United States was known for their steel, China for silk, Ethiopia for coffee, and most Middle Eastern countries for crude oil.

The Philippines used to be renowned for sugar, but has since lost its status as other countries were able to produce and sell the commodity at a cheaper price.

This company has built itself up to be the largest sugar miller in the country, yet its recent fundamentals haven’t been as strong as it may seem.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Centuries ago, before table sugar became known, honey was the only sweetener that people used. It was only in Southeast Asia after the first century when the cultivation of sugarcane began.

Slowly, the knowledge about this plant reached India, where people learned how to crystallize sugarcane. With this new discovery, sugar soon became a valuable commodity and was traded all over Asia and the Middle East throughout the centuries.

The craze for sugar spread to Europe as well, but the cold climate was inhospitable to the crop. As such, the European nations turned to their colonies.

In the Philippines, sugarcane farming expanded with the arrival of the Spanish and became the country’s main agricultural export during their rule.

The Philippine sugarcane industry continued to prosper under the Americans, as the former had preferential access to the largest economy in the world.

One of the largest sugar producers in the Philippines, Victorias Milling Company, Inc. (VMC:PHL), took advantage of this sugar boom.

The company was one of the first in the country to establish an industrial sugar mill, becoming one of the largest sugar millers in Asia and grinding as much as 1,500 tons of sugarcane daily.

However, the industry rapidly declined during the 1970s when the United States relaxed import restrictions on other countries. To mitigate the lost revenue, the company tried to diversify to other businesses.

Some of the notable business ventures it made were its golf club business in 1945, its food processing business in 1968, and its residential real estate business in 1975.

Its food processing business expanded and remains strong up to this day, exporting canned light tuna chunks to Canada.

The company also faced serious challenges during the Asian financial crisis in 1995. Cheap imported sugar was entering the market while the company was only partially operating during this time.

In addition, the company experienced legal troubles by borrowing extensively and serving false sugar quedans (warehouse receipts) as collateral. When the case became public, Victorias Milling had to file for bankruptcy, though not all of its debts were relieved.

In October 1997, the company was suspended from trading. Victorias Milling’s stock price closed at PHP 0.87 in 1997 from an initial price of PHP 21.00 in 1994, a 96% stock price devaluation. The company’s stock was only allowed to be traded again in 2012.

In 2014 to 2018, Victorias Milling underwent a major restructuring program, to finally pay off its restructured loans and redeem the remaining convertible notes.

Nowadays, the company is facing another set of challenges, this time concerning the COVID-19 pandemic. While the company has been affected by the recent market volatility in the recent weeks, its stock price has overall behaved similarly to its historical trend.

For Victorias Milling, their ability to supply sugar remains unchanged during the pandemic, considering that the milling season is still ongoing. However, the closure of many food establishments has caused sugar prices to drop by 18% from PHP 1,580 per 50kg to PHP 1,300 per 50kg.

Still, as-reported financials are showing higher profitability than what Uniform metrics reflect, overstating the company’s TRUE earning power.

In 2019, as-reported metrics posted a 4% ROA, but when removing the accounting distortions, Victorias Milling’s Uniform earning power is even lower at 3%.

One of the main contributing factors is how Philippine Financial Reporting Standards (PFRS) accounts for property, plant, and equipment (PPE).

According to PFRS, PPE is recorded at historical costs – that is, in the purchasing power the year the fixed asset was recorded. But to better reflect reality, PPE should be adjusted for inflation.

In Uniform Accounting, adjustments have to be made so that the asset and cash flow values are reflecting the current purchasing power each year.

Since the sugar milling business is capital intensive, the company should have recognized PHP 2.5 billion more in fixed assets in 2019 when adjusting for inflation.

When we add PHP 2.5 billion more to Victoria Milling’s asset base and with the many other adjustments Valens makes, we arrive at a TRUE earning power of 3%.

Victorias Milling’s earning power is weaker than you think

As-reported metrics distort the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a stronger business than real economic metrics highlight.

Uniform ROA has actually been lower than as-reported ROA for over twelve of the past sixteen years. For example, in 2019, Uniform ROA was 3%, a quarter lower than as-reported ROA of 4%. When Uniform ROA fell to negative levels in 2009, as-reported ROA was at a positive 4%.

Through Uniform Accounting, we see that the firm’s true ROAs have actually been weak. After ranging from 3%-4% levels in 2004-2005, Uniform ROA rose to 10% in 2006 and fell to negative levels in 2009. Thereafter, Uniform ROA recovered to 5%-6% levels in 2010-2012 and during its return to stock trading, the company improved further to a peak of 14% in 2014.

However, this improvement did not last as the company’s profitability gradually declined to below cost-of-capital levels of 2%-3% in 2017-2019.

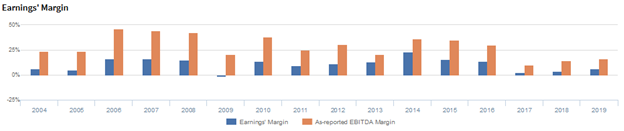

Victorias Milling’s earnings margin is much weaker than you think

Trends in Uniform ROA have largely been driven by similar trends in Uniform earnings margin.

Uniform margins ranged from 5%-6% in 2004-2005, before jumping to 15%-17% levels in 2006-2008 and breaching negative territory in 2009.

Then, Uniform margins recovered to a high of 23% in 2014, before fading to current 6% levels in 2019.

Every year, as-reported earnings margins have been overstated, making the company appear to be a stronger business than real economic metrics highlight.

At current valuations, markets are pricing in expectations for improvement in both Uniform earnings margin and Uniform asset turns.

SUMMARY and Victorias Milling Company, Inc. Corporation Tearsheet

As our Uniform Accounting tearsheet for Victorias Milling highlights, Uniform P/E trades at 22.8x, which is around the market average but below the company’s historical average levels.

Average P/Es require average EPS growth to sustain them. In the case of Victorias Milling, the company has recently shown a robust 31% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Victorias Milling’s sell-side analyst-driven forecast is to see immaterial growth in Uniform earnings in 2020-2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify PHP 2.49 per share. These are often referred to as market embedded expectations.

To meet the current market valuation levels of Victorias Milling, the company would need to immaterially grow its Uniform earnings over the next three years.

What sell-side analysts expect for Victorias Milling’s earnings growth is near the current stock market valuation required in 2020.

The company’s earning power is below the corporate average, and the company has high dividend risk, with an intrinsic credit risk of 630bps above than the risk-free rate.

To conclude, Victorias Milling’s Uniform earnings growth is slightly below peer averages in 2020 and the company is trading above peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com