This company thinks that diversification is not always the best strategy. With a 28% Uniform earning power, they’re proving how.

“Don’t put all your eggs in one basket!”

Odds are that every investor has heard of this golden rule of investing that has withstood the test of time: Diversification.

The returns of placing your entire portfolio in one investment or line of business rarely compensates for the high risk you have to take for not being diversified.

Yet one company in the Philippines has benefited from not diversifying, embedding this concept in their business philosophy.

As a result, this company is currently one of the most profitable PSEi companies according to Uniform Accounting metrics, and has become one of the Philippines’ most competitive international companies..

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

If the world economy is a human body, then cargo shipping is its lifeblood.

90% of global trade runs through cargo shipping.

It’s a shocking statistic, considering how aircrafts have been growing for years as the go-to mode of international transportation.

While transporting cargo by air is faster, airplanes face higher fuel costs and lower carrying capacity.

The Antonav AN-225, currently the world’s largest aircraft, carries up to 250 tons of cargo.

Meanwhile, the MSC Gulsun, currently the world’s largest container ship, has a deadweight tonnage of 197,500.

The difference between the two is massive, hence why maritime trade has continued to be an integral part of the global economy.

In the Philippines, our geography alone speaks for the importance of sea trade. Manila became the economic center of the country due to its proximity to the bay (now known as Manila Bay), which provided a natural harbor

From this harbor, the Port of Manila was built. It currently has three terminals:

– Manila North Harbor

– Manila South Harbor

– Manila International Container Terminal (MICT)

In 1988, the government made plans to privatize operations of the three terminals.

The company International Container Services Terminal, Inc. (ICT:PHL) won the bidding for the MICT contract.

Under the leadership and expertise of company chairman and president Enrique K. Razon, Jr. (also mentioned in last week’s Tuesday newsletter), International Container Terminal and its terminals flourished.

Coming from a family that has been in the marine cargo business for three generations, he realized the potential of specializing in the management of small- to medium-sized terminals.

By investing in ports of smaller scale, it becomes easier to operate the facilities and faster to apply technology, producing efficiency gains.

After going public in 1993 to raise capital, International Container Terminal began planning its expansion.

In 1999, the company made its first acquisition, obtaining minority control of Makar Wharf in General Santos City, Philippines.

Two years later, they started construction of Suape Container Terminal in Pernambuco, Brazil, which would become their first foreign terminal.

After decades of more port acquisitions, they now operate 32 terminals in 19 different countries spanning 6 continents. This includes a controlling interest in Manila North Harbor, the second terminal of the Port of Manila.

International Container Terminal has become the 8th largest box port operator in the world, despite their focus on small to medium ports in emerging markets.

However, cargo shipping can be a volatile market, often becoming subject to the politics of trade.

We’re seeing this today, most especially from the US-China trade war and Brexit where companies need to reorganize their global supply chain.

International Container Terminal’s foreign competitors are seeing this volatility, shifting more outside the port business.

PSA International, the largest box port operator in the world, recently bought a stake in an inland logistics company.

Similarly, Hutchison Port Holdings, the second largest, acquired a general logistics company.

With competitors diversifying operations, International Container Terminal has been pressured to follow suit.

Still, the company is resolute and has vowed to focus only on their port business, seeing an opportunity in the situation.

As the largest box port operator without an interest in any shipping line activity, they can treat every single carrier passing through their ports impartially.

As such, they are slowly building a reputation as a neutral operator.

They have managed to turn what was once deemed a downside of the company into their own competitive advantage.

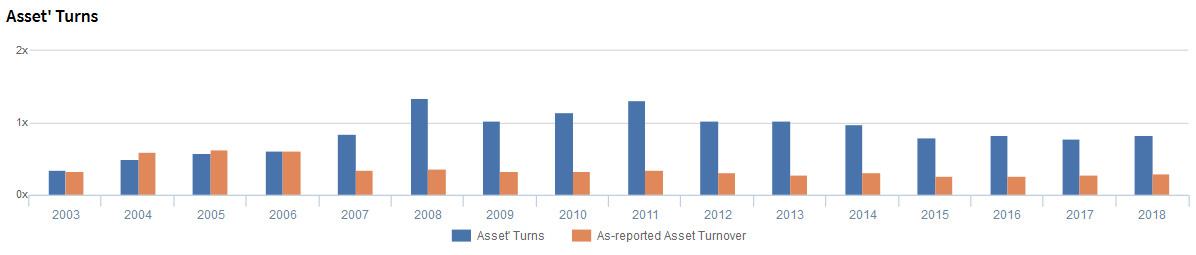

Yet, as-reported metrics state that the strategy has not paid off for the company, with as-reported asset turnover stagnating at 0.3x-0.4x levels since acquiring five foreign terminals in 2007.

While revenues have jumped up every year, their assets are reported to have grown at a similar pace.

However, their asset base is significantly made up of intangible assets, mostly in the form of concession rights from the aforementioned 2007 port acquisitions.

While important to the company’s operations, their balance sheet values are a poor representation of the assets’ true economic value.

Removing intangible assets from the asset turnover calculation leads us to a better understanding of the firm’s true asset efficiency.

Along with many more adjustments, International Container Terminal’s Uniform asset turnover actually ranges from 0.8x to 1.4x.

International Container Terminal’s earning power is more robust than you think

Historically, International Container Terminal has seen robust but generally cyclical profitability.

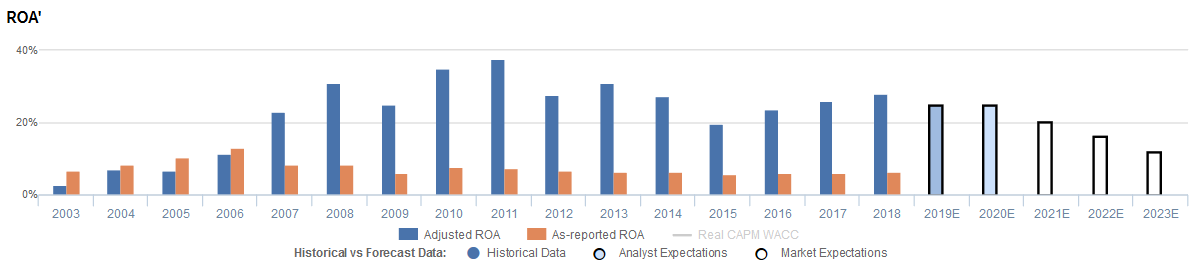

From 2003 to 2008, Uniform ROA (blue bars) improved from 3% to 31% levels, before declining temporarily to 25% the next year. The as-reported ROA (orange bars) will tell you the company only managed to peak in 2006.

From 2010-2011, International Container Terminal’s earning power increased further to 35% and to a peak of 38% levels, before declining to 28% in 2012. Uniform ROA then slightly recovered to 31% in 2013, but this recovery did not last as the company saw declining earning power until 2015, though Uniform ROA once again saw improvement in recent years.

As-reported metrics would have you believe that International Container Terminal Services profitability ranged only at 6%-13% historically, when in reality the company was able to perform 5x corporate average levels.

International Container Terminal’s asset turns are a lot stronger than you think

The strength of their ROA lies on their asset turns. This implies that the company is more concerned about generating sales for every dollar spent in assets.

In 2007, International Container Terminal acquired five port terminals. This was also the time when International Container Terminal’s Uniform and as-reported ROA widened, similar to the widening between Uniform and as-reported asset turns.

To illustrate, the as-reported asset turns for International Container Terminal have been in the range of 0.3x-0.4x since 2007, far lower than Uniform asset turns of 0.8x-1.4x.

The as-reported numbers make the company appear far less efficient in churning revenue out of their asset base than real economic metrics highlight, materially distorting the market’s perception of the firm’s historical asset efficiency trends.

SUMMARY and International Container Terminal Tearsheet

As our Uniform Accounting tearsheet for International Container Terminal highlights, Uniform P/E trades at 13.2x, which is below market averages but around historical average levels.

Low P/Es require low EPS growth to sustain them. In the case of International Container Terminal, the company has recently shown 17% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, International Container Terminal’s sell-side analyst-driven forecast is for Uniform earnings to grow immaterially in 2019, before showing strong growth of 13% in 2020.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify PHP128.00 per share. These are often referred to as market embedded expectations.

To meet the current market valuation levels of International Container Terminal, the company would need to have Uniform earnings shrink by 10% each year over the next three years.

What sell-side analysts expect for International Container Terminal’s earnings growth is far higher than what the current stock market valuation requires.

To conclude, International Container Terminal’s Uniform earnings growth is below peer averages in 2019. Yet, the company is trading below average peer valuations.

The company’s earning power is 5x the corporate average, and the company has low dividend risk, signaling that their cash flow risk to the company’s operations and credit profile in the future is low.

About the Philippine Markets Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com