This FMCG company brushed their competition away by making their brand unforgettable and Uniform ROAs of 27%+ prove it

Frankly, all toothpastes function the same. So logically, consumers should just buy the cheapest one.

But in a sea of branded, cheaper toothpastes, this fast-moving consumer goods (FMCG) giant managed to establish customer loyalty by successfully executing a branded recall strategy.

This strategy put the company at the top of the industry.

Though as-reported metrics indicates that this strategy might not be doing so well, TRUE UAFRS-based (Uniform) analysis shows that this company has been able to maintain their robust profitability and will continue to do so in the years ahead.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Out of sight but not out of mind.

When you’re selling the same product as everyone else, you have to get creative with your advertising and marketing campaigns.

One powerful strategy used by businesses to get an advantage when it comes to consumer preference is through brand recall.

Brand recall gauges how much a product leaves a mark on their customers’ minds.

If someone were to stop you on the street and ask you to name a brand of soda, you’d say Coke. Or a phone network and you’d say Globe. Or a razor and you’d say Gillette.

This is an example of unaided brand recall.

As opposed to aided brand recall, this type of recall determines how well a consumer remembers a brand without any sort of external clues.

Businesses prefer unaided over aided because it proves that their advertising efforts are working as intended.

So when a customer is choosing which product to buy, they’re pulled towards what they already know. And once this product runs out, that customer would instinctively want to buy from the same brand.

It creates a cycle of repeat sales, and the company gets what they want the most: loyalty.

In the Philippines, Colgate’s unaided brand recall is so effective that the term “Colgate” becomes synonymous with “toothpaste.” You don’t go to the sari-sari store to buy toothpaste, you buy Colgate, regardless of what the actual brand is.

But it’s not enough that consumers remember the product.

For the strategy to be effective, the product has to be of high quality. The brand has to be as visible to the buying public as possible. Having a catchy tagline or a unique brand name wouldn’t hurt, either.

Luckily for Colgate, it has it all. It’s not the number 1 selling toothpaste in the world for nothing.

Their toothpastes go through a lengthy process of research and development before they get rolled out to market, so you know they’re top quality.

Clinical trials are done in order to study and design products that are useful in teeth whitening and overall oral health.

Even the flavor of the toothpaste is carefully and thoroughly researched, based on global preferences. Spearmint is more popular in Latin America while in Europe, peppermint appeals more to consumers, so products in these regions vary.

In terms of visibility, Colgate has done an amazing job of making sure that their products are seen.

They have an extensive distribution network in both urban and rural markets. Thanks to their broad portfolio of successful products, they are given more shelf space on grocery stores, further increasing visibility.

Their marketing and advertising strategies propelled them to the top of the industry, raking in almost half of the market share in oral care hygiene products.

The success of the company in being the market leader is reflected in their Uniform earning power.

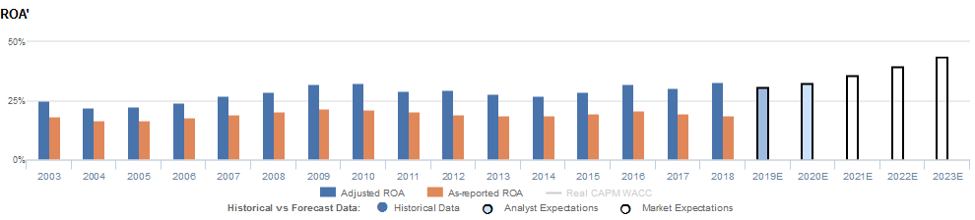

As-reported return on assets (ROA) were at 17%-22% in the past 16 years but UAFRS shows that returns have actually been more robust, with Uniform ROAs of 22%-34%.

While market expectations are for the company’s Uniform ROA to return to previous highs of 34%, management’s concerns over product growth, price increases, and brand relatability may make it more difficult for the company to realize these expectations.

Colgate-Palmolive’s earning power is actually more robust than you think

As-reported metrics significantly understate Colgate-Palmolive Company’s (CL:USA) profitability. For example, as-reported ROA for Colgate-Palmolive was 17% in 2019, which is materially lower than Uniform ROA of 27%, making Colgate-Palmolive appear to be a much weaker business than real economic metrics highlight

Moreover, as-reported ROA has slightly decreased from 21% in 2016 to current 17% levels, while Uniform ROA also decreased from 34% to 27% over the same period, significantly distorting the market’s perception of the firm’s historical profitability trends.

Historically, Colgate-Palmolive has seen somewhat cyclical but overall improving profitability. From 2004-2010, Uniform ROA improved from 22% to 32% before falling to 27% levels in 2014. It then increased to a peak of 34% in 2016 before declining again to 27% in 2019.

Colgate-Palmolive’s earnings margins are overstated while asset turns are understated

Trends in Uniform ROA have largely been driven by its stability in Uniform earnings margin and trends in Uniform asset turns.

From 2004-2010, Uniform earnings margin improved from 13% to 18%, before declining to 16% in 2014 and expanding to 18% in 2019.

Meanwhile, after falling from 1.9x in 2008 to 1.8x in 2009, Uniform asset turns further declined to 1.5x in 2019.

At current valuations, markets are pricing in expectations for continued stability in Uniform earnings margin, coupled with slight improvements in Uniform asset turns.

SUMMARY and Colgate-Palmolive Tearsheet

As the Uniform Accounting tearsheet for Colgate-Palmolive highlights, the Uniform P/E trades at 23.3x, which is around corporate average valuation levels and its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of Colgate-Palmolive, the company has recently shown a -5% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Colgate-Palmolive’s Wall Street analyst-driven forecast is 6% into 2019, and also in 2020.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Colgate-Palmolive’s $68 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 4% each year over the next three years.

What Wall Street analysts expect for Colgate-Palmolive’s earnings growth falls below what the current stock market valuation requires.

The company’s earning power, based on its Uniform return on assets calculation, is 4x the corporate averages. Together, this signals low cash flow risk to the current dividend level in the future.

To conclude, Colgate-Palmolive’s Uniform earnings growth is above peer averages in 2020. Also, the company is trading below average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com