This gaming company captured the king and crushed the mobile gaming space, with returns that are 5x the as-reported

The software-as-a-service (SaaS) model revolutionized the tech industry. Instead of having to pay a large amount for a perpetual license for a particular software, users have now switched to a subscription-based periodic payment scheme that’s significantly cheaper.

This company pioneered the use of the SaaS model in the gaming space, as opposed to traditional software. Furthermore, it made an acquisition that enabled it to expand into the mobile gaming space.

With the additional revenue streams and a transformation of the business model, returns are expected to be more robust, as is the case for most SaaS businesses. However, as-reported metrics indicate that the SaaS model seems inappropriate when used in a gaming setting. It also implies the mobile game acquisition has not brought on the expected synergies.

In reality, Uniform Accounting shows that the company’s Uniform return on assets (ROAs) have been much stronger and stable, as is expected from SaaS firms, and thanks to the successful acquisition.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

With over 2.5 billion active gamers around the globe, the gaming industry is set to be worth about $200 billion by 2023 as industry trends continue to focus on digital innovation and market expansion.

Currently, the industry is outperforming the broader market as interest in gaming has spiked as people continue to stay at home to slow the spread of the coronavirus.

Among the gaming companies benefitting from this unprecedented tailwind are the leaders Take-Two Interactive (TTWO), Electronic Arts, Inc. (EA), and Activision Blizzard, Inc. (ATVI).

We’ve previously talked about how EA has strategically reorganized and invested heavily into its online and multiplayer platforms to revive profitability. Activision Blizzard did something similar, and more, to boost stagnating profitability.

Since Activision’s merger with Blizzard, the company has been developing and improving new and old game titles from all types of genres. It also helped revolutionize a different type of game to the industry—the massively multiplayer online role-playing game (MMORPG).

World of Warcraft, released by the company in 2004, was the most popular of its MMORPG franchises, clocking in at a peak of 12 million monthly active users.

More importantly, this game enabled Activision Blizzard to adopt the software-as-a-service (SaaS) model in the gaming space, as opposed to the traditional software setting.

This meant that users now require a monthly subscription to continue playing. It makes it more expensive for consumers, but they get the satisfaction of playing an interactive and dynamic game that’s constantly updated to expand the virtual universe.

To further expand its reach and to kickstart growth, the company entered into the mobile gaming industry when it acquired Candy Crush maker King Entertainment for $5.9 billion in 2016.

While free to download, Candy Crush uses a pay-to-win model—users who are willing to spend on in-game transactions can unlock special features (power ups, extra lives, etc.) that will significantly boost their chances of winning.

These incremental purchases cost almost nothing each time, but they stack up massively. In fact, in 2018 alone, the Candy Crush game made a whopping $1.5 billion because of these microtransactions.

Furthermore, in 2019, the company launched Call of Duty (COD) Mobile. The game had a record-breaking 150 million downloads in the first three months of its release, helping the company grow its player base from 40 million to 100 million in less than a year.

Like the Candy Crush saga, albeit at a smaller size, COD Mobile has made more than $2 million in microtransactions.

As a pioneer of the SaaS model in the gaming space, and with the success of its mobile gaming segment arising from its 2016 King acquisition, the company should have robust and stable returns.

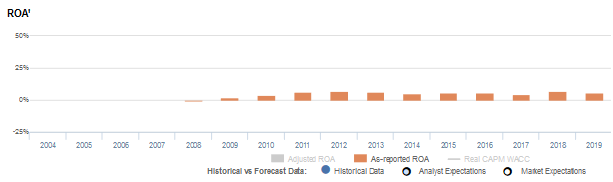

However, looking at as-reported metrics, it seems that wading through uncharted territory was a high-risk, low-return move. Return on assets (ROAs) were slightly below cost-of-capital, ranging from -1% to 7% in the past twelve years.

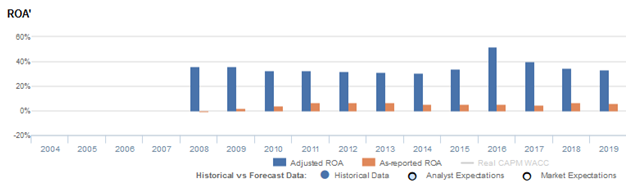

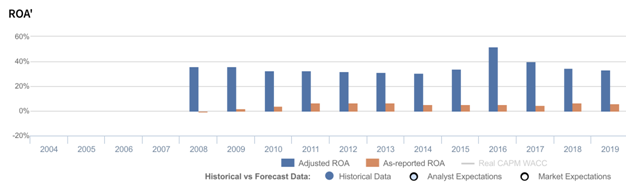

In reality, Uniform Accounting shows that Activision Blizzard’s mobile expansion and SaaS model have actually helped the company sustain ROAs over 30%, returns that are similar to traditional SaaS software firms.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of accumulated goodwill on Activision’s balance sheet, which sits at about $9.7 billion to $9.8 billion in recent years, stemming from the King acquisition.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Activision’s earning power. Adjusting for goodwill, returns are actually 5x-10x greater.

Activision Blizzard’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Activision Blizzard’s Uniform ROA has actually been higher than its as-reported ROA in all of the twelve years. Most recently, as-reported ROA was 6% in 2019, but its Uniform ROA was actually higher at 33%.

Historically, Activision Blizzard’s Uniform ROA has ranged from 31% to 52% in the past twelve years while as-reported ROA ranged only from -1% to 7% in the same timeframe.

Uniform ROAs have declined slightly from 36% in 2008 to 34% in 2015 before jumping to a peak of 52% due to the acquisition of King Entertainment. Uniform ROAs have since reverted to previous 33% levels.

Activision Blizzard’s Uniform earnings margins are weaker, but its robust Uniform asset turns make up for it

Activision Blizzard’s trends in profitability have been driven by stability in Uniform asset turns and to a lesser extent, Uniform earnings margins.

From 2008-2015, Uniform earnings margins remained fairly stable at 24%-27% levels, before expanding to a high of 36% in 2016, and fading to 30% in 2017.

Similarly, after falling from 1.3x in 2008 to 1.2x in 2013, Uniform asset turns gradually improved starting 2014 until it achieved a peak of 1.5x in 2016. Thereafter, Uniform turns decline once again until its lowest level of 1.1x in 2019.

At current valuations, the market is pricing in expectations for further declines in Uniform earnings margins, coupled with stability in Uniform asset turns.

SUMMARY and Activision Blizzard Tearsheet

As the Uniform Accounting tearsheet for Activision Blizzard, Inc. (ATVI) highlights, the Uniform P/E trades at 25.9x, which is around corporate average valuation levels but above its own recent history.

Average P/Es require average EPS growth to sustain them. In the case of Activision Blizzard, the company has recently shown a 13% Uniform EPS contraction.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Activision Blizzard’s Wall Street analyst-driven forecast is a 25% and 4% EPS growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Activision Blizzard’s $83 stock price. These are often referred to as market embedded expectations.

The company needs to grow its Uniform earnings by 7% each year over the next three years to justify current prices. What Wall Street analysts expect for Activision Blizzard’s earnings growth is above what the current stock market valuation requires in 2020, but below its requirement in 2021.

Furthermore, the company’s earning power is 6x the corporate average. Also, cash flows are almost 5x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Activision Blizzard’s Uniform earnings growth is in line with peer averages in 2020, but the company is trading below average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus ”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com