This husband and wife tandem has struck gold in this business but investors still aren’t sold. TRUE Earnings Margin of 5% may warrant such bearishness

At the peak of the Asian Financial Crisis, husband and wife Lucio and Susan Co started a supermarket that turned into a retail chain success, becoming the second largest supermarket company in the country in 2018 with around 300 branches.

On an as-reported basis, the company appears to have high returns and the means to sustain them. However, market expectations continue to be bearish.

UAFRS-based (Uniform) Metrics may shed some light as to why this is, allowing us to reveal what the company is hiding: that returns are actually trending differently.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

The plan of budding grocery chain MerryMart to go public speaks to the competitiveness of the Philippine supermarket space.

The top three largest supermarket chains only account for around 20% of the industry’s total revenue while the rise in sari-sari and convenience stores is limiting room for growth for supermarkets.

Brand loyalty is almost nonexistent, with a recent consumer behavior study showing that Filipinos value convenience most when purchasing fast-moving consumer goods (FMCG).

In addition, the country’s growing e-commerce landscape aims to revolutionize the way people shop for groceries, with the rise in online stores and delivery.

Nonetheless, the supermarket giants have plans of their own.

Puregold Price Club, Inc. (named after its namesake supermarket chain) is differentiating itself from the competition by simultaneously catering to both customer groups, the small buyers and the bulk purchasers.

The Puregold supermarket’s target market is the average Filipino, those who often purchase in relatively small quantities at a time.

In 2012, the company acquired S&R, a membership-only warehouse store similar to the likes of Costco, which enabled them to sell to more affluent consumers who prefer to buy goods in bulk.

With these two subsidiaries, Puregold expanded rapidly across the country.

As of 2018, they own 289 Puregold stores and 16 S&R warehouses, with blueprints for 25 more Puregold stores and two S&R warehouses.

In the ecommerce field, Puregold has endeavored to make huge strides.

They recently launched a mobile app called Sally (short for Shopping Ally), where people can shop for groceries on their phone, with pickup at the chosen branch.

Despite these ambitious initiatives, Puregold has failed to excite the market.

Puregold’s stock price has been on a downtrend ever since early 2019, falling by almost 25% from PHP 49 to PHP 37.

The market may be unconvinced about the ability of their projects to generate sufficient returns.

Uniform Metrics are reflecting the same.

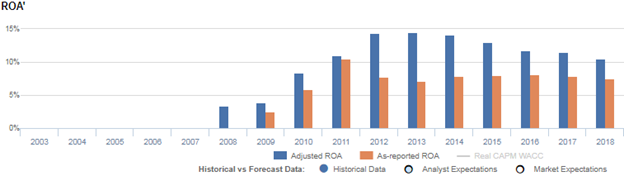

While the company’s TRUE performance has been better than what as-reported financials state, it has been deteriorating since 2013 from 15% to 11% in 2018 as the firm ramped up usage of operating leases.

The use of operating leases pre-2019 has had the effect of hiding assets from the company’s balance sheet, leading to an understatement of their actual ROA.

As such, Puregold’s as-reported financials do not provide a full picture of its actual performance.

Capitalizing this expense to reflect the company’s true asset base shows PHP 19.3bn in additional assets in 2018 from PHP 12.9bn in 2013.

Meanwhile, as-reported ROA claims that the company has generated return on assets of around 7%-8% levels since 2012, leading investors to think that the company isn’t actually recording declining earning power.

Puregold’s earning power is stronger than you think

Despite the converging trend, as-reported ROA continues to understate Puregold’s (PGOLD:PHL) profitability. Uniform ROA of 11% in 2018 is more than a third higher than as-reported ROA of 8%, making Puregold appear to be weaker than real economic metrics highlight.

Historically, Puregold has seen robust profitability. From 2008 to 2012, Uniform ROA improved from 3% to a near peak of 14% levels in 2012 as they acquired S&R. Returns rose marginally to 15% in 2013 before falling gradually to 11% levels in 2018.

As-reported ROA will tell you that the company’s performance has performed worse since the aforementioned acquisition and that returns have been stable at 7%-8% levels since 2012.

Puregold’s asset turn is stronger than you think, but earnings margin drives the downward trend

Puregold’s strength in Uniform ROA has come from Uniform Asset Turns, but its trend has been driven by Uniform Earnings Margin. This implies that the company is more concerned about generating sales rather than maximizing price relative to cost.

Historically, Uniform asset turns for Puregold have been stable in the range of 2.3x-2.9x since 2008, with the exception of outlier 4.4x in 2011.

Meanwhile, Uniform earnings margins have been more volatile. It was below 2% levels in 2008-2010, reached 4% in 2011, and achieved a peak of 6% in 2013-2015. It fell soon after to 5% in 2018 where it currently sits.

At current valuations, markets are pricing in expectations for continued stability in Uniform Turns, but further reduction in Uniform Margins.

SUMMARY and Puregold Tearsheet

As our Uniform Accounting tearsheet for Puregold highlights, Uniform P/E trades at 17.9x, which is below market average and historical average levels.

Low P/Es require low EPS growth to sustain them. In the case of Puregold, the company has recently shown 5% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Puregold’s sell-side analyst-driven forecast is for Uniform earnings to shrink 1% in 2019, before showing growth again of 14% in 2020.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify PHP37.00 per share. These are often referred to as market embedded expectations.

To meet the current market valuation levels of Puregold, the company would need to maintain current levels of Uniform earnings each year over the next three years.

What sell-side analysts expect for Puregold’s earnings growth is lower than what the current stock market valuation requires in 2019.

To conclude, Puregold’s Uniform earnings growth is above peer averages in 2019 and the company is trading below average peer valuations.

The company’s earning power is almost twice the corporate average, and the company has low dividend risk, signaling that their cash flow risk to the company’s operations and credit profile in the future is low.

About the Philippine Markets Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com