This PNB fund invests in established companies—undervalued by as-reported metrics—that pay dividends!

Professional money managers utilize different strategies to generate good investment returns.

There are investors, like Warren Buffett, who employ value investing, where they basically invest in under-priced companies. Some use complex mathematical methods and quantitative models like Jim Simons of Renaissance Technologies. They study patterns and make predictions from stock price movements.

Still, there are growth investors who focus on companies exhibiting above-average growth. Meanwhile, others prefer stability in their portfolio by investing in high-dividend companies.

In today’s Philippine Markets Daily (PMD), we take a look at the first domestic equity unit investment trust fund (UITF) that focuses on investing in established companies that offer high, regular dividend payouts.

In addition, we’re including a fundamental analysis of one of the fund’s largest holdings, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Philippine Markets Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

Stock market investors can generate investment returns through stock price appreciation, dividends, or both.

While it’s more common for investors and money managers to look for intrinsically under-priced companies, dividend investing is not new to many.

In fact, John Bogle, the founder of the Vanguard Group—the largest mutual fund provider in the world—understood the importance of dividend yields.

“In the long run, it is dividend yields and earnings growth that are the fundamental driver of stock returns.” – John Bogle

Dividends are shares of a company’s profit paid out in cash to shareholders on a regular basis—monthly, quarterly, or annually.

It is important to note that not all companies pay dividends. Companies decide whether to distribute dividends or not based on several fundamental factors, such as the general state of the economy, their ability to sustain dividend payments, and growth prospects.

Smaller firms may opt to reinvest in their assets to pursue growth opportunities. Meanwhile, the more steady ones may choose to pay out dividends to attract investors. Typically, it is the established and stable companies who consistently provide dividends to their shareholders.

Fund managers utilizing a dividend investing strategy rely on these stable, high-paying firms with the hopes of generating income and capital appreciation.

This is exactly what the Philippine National Bank (PNB) had in mind in the second quarter of 2012 when it launched the country’s first dividend UITF—the PNB High Dividend Fund.

The PNB High Dividend Fund is a UITF primarily focused on investing in companies with high dividend yields and in established and stable companies with regular dividend payouts to generate higher investment returns for its investors.

Since its inception, the PNB High Dividend Fund has generated 30% cumulative investment returns. However, the fund underperformed its benchmark, the Philippine Stock Exchange Index (PSEi), which delivered 59% investment performance over the same period.

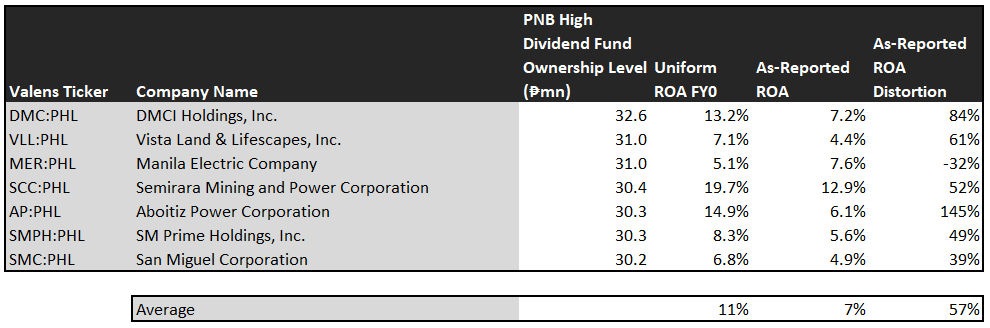

The table below shows the top non-financial holdings of the PNB High Dividend Fund along with their Uniform return on assets (ROA), as-reported ROA, and ROA distortion—the difference between Uniform and as-reported ROA.

Looking solely at the as-reported ROA numbers, one may see a portfolio with slightly above-average profitability. In 2019, the PNB High Dividend Fund generated an average ROA of 7%, versus global corporate average returns of 6%.

However, on a Uniform Accounting basis, this UITF has actually delivered stronger earnings, with an average Uniform ROA of 11%, which is well above cost-of-capital levels. Uniform Accounting adjusts for the distortions in companies’ financials brought about by the inconsistencies in the Philippine Financial Reporting Standards (PFRS) to reveal the true underlying performance of companies.

As such, it should not be surprising that when analyzing the non-financial holdings of the PNB High Dividend Fund, the figures that easily stand out are the double-digit discrepancies between Uniform ROA and as-reported ROA for these companies.

While the difference in raw figures may not seem too distant, the distortion in percentage ranges from -32% to 145%, with Aboitiz Power Corporation (AP:PHL) having a distortion greater than a hundred percent.

As-reported ROA understates the earning power of AP, suggesting that it is an average firm when in reality, it is a high quality firm with Uniform ROA more than twice global corporate average returns.

Similarly, DMCI Holdings, Inc. (DMC:PHL) is not just a 7% ROA firm. It is a high performing company that generated +10% returns over the past three years.

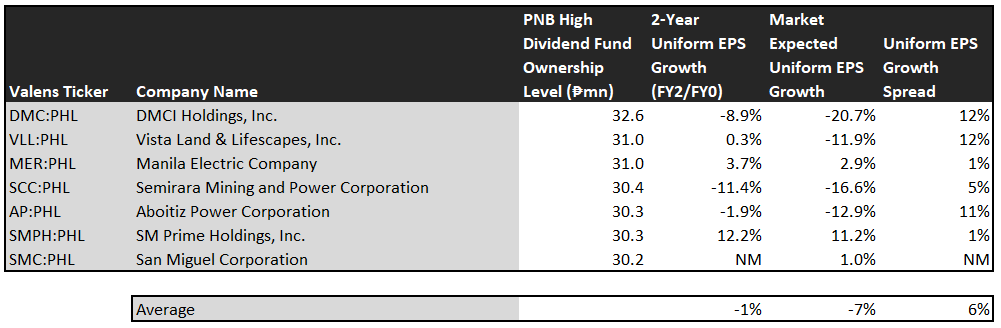

This table shows the earnings growth potential of the top holdings of the PNB High Dividend Fund. It features three key data points:

- The two-year Uniform EPS growth represents the Uniform earnings growth the company is likely to have for the next two years. The earnings number used is the converted value of consensus sell-side analyst estimates to the Uniform Accounting framework.

- The market expected Uniform EPS growth represents what the market thinks Uniform earnings growth is going to be for the next two years. Here, we show by how much the company needs to grow Uniform earnings in the next two years to justify the current stock price of the company. This is the market’s embedded expectations for Uniform earnings growth.

- The Uniform EPS growth spread is the difference between the two-year Uniform EPS growth and market expected Uniform EPS growth.

On average, Philippine companies are expected to have a 6% annual Uniform earnings growth over the next two years. Meanwhile, PNB High Dividend Fund’s top holdings are forecast to lag that with 1% projected Uniform earnings shrinkage in the next two years.

The market expresses a more bearish sentiment, forecasting these companies to decelerate by 7% a year over the next two years.

Among these companies, DMC and Vista Land & Lifescapes, Inc. (VLL:PHL) have the highest Uniform earnings growth dislocation.

The market is pricing DMC’s Uniform earnings growth to weaken by 21% in the next two years. Meanwhile, sell-side analysts are less bearish, seeing DMC’s Uniform earnings growth to slow down by 9% moving forward.

Meanwhile, the market is seeing 12% Uniform earnings shrinkage for VLL. However, analysts are forecasting flat earnings for the firm in the next two years.

Given the importance of profitability and earnings growth potential in the sustainability of dividend issuance, which is the core of this fund’s investing strategy, PNB may need to take another look at Semirara Mining and Power Corporation (SCC:PHL) and Manila Electric Company (MER:PHL).

Both the market and the analysts are seeing double-digit earnings shrinkage for SCC moving forward. Meanwhile, as-reported numbers overstate MER’s profitability with an as-reported ROA of 8%, when in reality it is a subpar firm with 5% Uniform ROA.

Overall, one might think that this portfolio seems unimpressive, with middling ROAs and depressed earnings growth prospects. However, through the lens of Uniform Accounting, investors can now see the reality—that the PNB High Dividend Fund comprises mostly of above-average companies with healthy profitability levels, albeit with muted earning power potential.

DMCI Holdings Tearsheet

Today, we’re highlighting one of the largest individual stock holdings in PNB High Dividend Fund—DMCI Holdings.

As our Uniform Accounting tearsheet for DMCI Holdings, Inc. highlights, Uniform P/E trades at 7.2x, well below global corporate averages and its historical averages.

Low P/Es require low, and even negative, EPS growth to sustain them. In the case of DMCI Holdings, the company has recently shown a 19% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that poorly track reality. However, sell-side analysts have a strong grasp on near-term financial forecasts like revenue and earnings.

We take sell-side forecasts for PFRS earnings as a starting point for our Uniform earnings forecasts. When we do this, DMCI Holdings’ sell-side analyst-driven forecast shows that Uniform earnings will shrink by 36% in 2019 and grow by 30% in 2020.

Based on the current stock market valuations, we can back into the required earnings growth rate that would justify PHP 5.29 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels of DMCI Holdings, the company would have to have Uniform earnings shrink by 21% each year over the next three years. What sell-side analysts expect for DMCI Holdings earnings growth is above what the current stock market valuation requires.

The company has an earning power greater than long-run corporate averages—based on its Uniform ROA calculation. Moreover, with cash flows and cash on hand consistently exceeding obligations in the next five years, DMCI Holdings has a low credit and dividend risk.

To conclude, DMCI Holdings’ Uniform earnings growth is well below peer averages in 2019. However, the company is trading well below peer average valuations.

About the Philippine Markets Daily

“Friday Uniform Portfolio Analytics”

Investors who don’t engage in the buying or selling of securities for a living oftentimes rely on professionals to manage their own investments within the scope of their investment policies.

With so many funds and managers out there, it can get confusing and difficult to decide which one best suits your needs as an investor.

Every Friday, we focus on one fund in the Philippines and take a deeper look into their current holdings. Using Uniform Accounting, we identify the high-quality stocks in their portfolio which may not be obvious using the as-reported numbers.

We also identify which holdings may be problematic for the fund’s returns that they would need to reconsider from a UAFRS perspective.

To wrap up the fund analysis, we highlight one of their largest holdings and focus on key metrics to watch out for, accessible in our tearsheets.

Hope you’ve found this week’s focus on the PNB High Dividend Fund interesting and insightful.

Stay tuned for next week’s Friday Uniform Portfolio Analytics!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com