This real estate company has not only built a solid foundation of properties, but also leads the industry with its 9% TRUE earning power.

After experiencing one of the most extreme market sell-offs, stock prices of most major Philippine companies have started rallying recently.

Investors have realized that valuations have become far too low than warranted, paving the way for a buying opportunity.

This real estate company is the biggest property developer in the country and has seen a similar stock rally. However, it continues to trade below recent averages relative to Uniform (UAFRS-based) earnings.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine – listed Focus

Powered by Valens Research

Makati city is currently the Philippines’ richest city and is one of the main central business districts in the country. But it hasn’t always enjoyed this prestige.

Makati used to be an undeveloped marshland, owned by the Zobel de Ayala family. In the wake of World War II, however, demand for real estate outside the then-devastated Manila grew.

In addition, Makati’s close proximity to the former U.S. military base Fort Bonifacio made it a desirable place for military families to settle.

Seeing this unpassable business opportunity, the Ayalas ventured into the real estate business through Ayala Corporation (AC:PHL).

By building the multi-lane Ayala Avenue, they literally paved the way for the construction of some of the country’s first high-rise buildings. They also built one of the most well-known private subdivisions, Forbes Park, and many other establishments including shopping malls and hotels.

As the company grew from its various property developments, they started expanding their business interests, even entering the electronics manufacturing industry in the early 1980s.

After venturing into other businesses, the company had expanded so much that it needed to spin off its core real estate business. That business is now known as Ayala Land Inc. (ALI:PHL).

With Makati on its way to cityhood in the 1990s, one would think that that’s all there is to it with Ayala Land. For most companies, to build a prospering city from the ground up would have been enough to call it a day.

Even so, Ayala Land continued to take on bigger projects.

In the 1970s, they built a new community out of a simple mango orchard in Muntinlupa city. Today, it is a bustling suburb.

Decades later, in 2003, they acquired a stake in Bonifacio Land Development Corporation. This consortium was charged with the development of Fort Bonifacio, what would become today as Bonifacio Global City (BGC).

BGC was one of the newest commercial and financial districts, becoming a hotspot for companies to establish their headquarters. Even the Philippine Stock Exchange, after years of operating in Makati and Pasig city, chose to relocate its trading floor to BGC in 2018.

Yet, despite all of these achievements, Ayala Land may still have room to grow.

The 2009 REIT Act allowed property companies to set up Real Estate Investment Trusts (REITs) or another company that exclusively owns a portfolio of income-producing properties. However, the regulations were too strict for any real estate company to incorporate a REIT.

In January 2020, the REIT Act was amended, which relaxed the requirements for property companies. Ayala Land became the first to apply for a REIT offering.

If successful, this could unlock a substantial amount of liquidity, enabling them to capitalize on a whole host of investment opportunities.

Unfortunately, the COVID-19 pandemic has caused unforeseen delays in the company’s plans as operations have temporarily ceased. This resulted in Ayala Land’s stock price plummeting in the past month. It now trades at valuations last seen in 2008, during the global financial crisis.

While fueled by the ongoing pandemic and a slowdown in sales of residential properties, this bearish sentiment is likely to have been aggravated by a misunderstanding of the firm’s TRUE profitability.

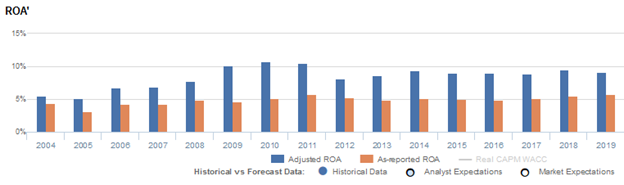

As-reported metrics suggest that the company posted a 6% ROA in 2019, whereas by removing the accounting distortions, Ayala Land’s Uniform earning power is actually higher at 9%.

One of the said distortions stems from how Philippine Financial Reporting Standards (PFRS) classifies interest expense.

According to PFRS, interest expense is an operating cash flow. In reality, interest expense represents the cost of debt and is rightfully a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

For example, in 2019, Ayala Land recognized an interest expense of PHP 11.4 billion, a third of as-reported net income of PHP 33.2 billion. When we add the PHP 11.4 billion back to earnings, because it is not an operating expense, net income increases. This adjustment alone represents a 1.6% jump in Uniform earning power.

Cross-comparison against peers also becomes possible since the performance, expectations, and valuations of companies are now evaluated irrespective of the amount of leverage.

Ayala Land’s earning power is stronger than you think

As-reported metrics are significantly understating Ayala Land’s profitability.

For example, Uniform ROA was 9% in 2019, higher than as-reported of 6%. In addition, Uniform ROA has been 1.5x higher than as-reported ROA since 2013 and has been higher than as-reported ROA for over the past sixteen years.

As-reported metrics have distorted the market’s perception of the firm’s historical profitability trends. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Historically, Ayala Land has seen stable and somewhat cyclical profitability. From 2004-2011, Uniform ROA improved from 6% to 11%, before falling to 8% levels in 2012. Thereafter, Uniform ROA slightly recovered to 9% levels where it remained until 2019.

Ayala Land’s asset turns are stronger than you think

Trends in Uniform ROA have largely been driven by similar trends in Uniform asset turns, suggesting that the firm has relied more on efficient asset utilization for earnings growth.

From 2004 to 2010, Uniform asset turns continuously improved from a low of 0.3x to an all time high of 0.6x. Then Uniform turns declined from 0.5x in 2011 to 0.4x levels in 2012, where it has remained at this level since.

In every year, as-reported metrics have understated the company’s true asset turns, making the company appear to be less efficient in the use of assets than real economic metrics highlight.

SUMMARY and Ayala Land, Inc Corporation Tearsheet

As our Uniform Accounting tearsheet for Ayala Land highlights, its Uniform P/E trades at 15.9x, which is below the market average and the company’s historical average levels.

Low P/Es require low EPS growth to sustain them. In the case of Ayala Land, the company has recently shown a 1% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Ayala Land’s sell-side analyst-driven forecast is to see Uniform earnings growth of 8% in 2020, before seeing a strong 17% growth in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify PHP 32.00 per share. These are often referred to as market embedded expectations.

To meet the current market valuation levels of Ayala Land, the company would need to shrink its Uniform earnings by 4% each year over the next three years.

What sell-side analysts expect for Ayala Land’s earnings growth is higher than what the current stock market valuation requires.

The company’s earning power is 2x the corporate average, while the company has low dividend risk, with cash flows and cash on hand greater than total obligations.

To conclude, Ayala Land’s Uniform earnings growth is above peer averages in 2019, and the company is trading below peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com