This soda producer is chugging down its new costs, with TRUE Uniform margins fizzling out at 1% and not 5% as reported

As more people wisen up to the dangers of excessive sugar consumption, sugar-dependent businesses should be worried about the future. Even the Philippine government has stepped in by enacting a tax directly aimed at sweetened beverages.

As-reported metrics think this soft drink manufacturer’s margins continue to thrive after the said regulation passed, but Uniform Accounting shows the firm to be barely hanging on to a small positive amount.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

With Christmas drawing closer, Filipinos are setting their minds to the celebrations ahead, including the feasts they will be preparing.

The food served in such feasts usually varies per family or by region, but the one item that always seems to be present is soft drinks. Found in almost every retail store, soft drinks have become the go-to beverage of those looking for something tastier than plain water.

However, even though soft drinks are satisfying to consume, its high sugar content can be detrimental to one’s health. A can of soda easily exceeds one’s recommended daily amount of sugar intake.

Filipinos’ overconsumption of sugar has prompted the Philippine government to intervene, by disincentivizing the purchase of sugary drinks. In 2017, as part of the TRAIN Act, an excise tax was implemented by as much as PHP 12 per liter on sweetened beverages.

The tax severely impacted the industry. Many fruit juice brands were forced to offer 100% natural fruit juice, while ready-to-drink coffee brands had to cut back on its sugar content just to evade the tax.

That said, the regulation affected soft drinks the hardest. Unlike the fruit juice and ready-to-drink coffee businesses, soft drink companies are heavily reliant on sugar so the same strategy could not be applied.

The only options the soft drink companies had were to either raise their prices or absorb the cost. The former choice would lead to a substantial loss in customers, but the latter will not.

Macay Holdings, Inc. (MACAY:PHL), owner of the RC Cola brand in the Philippines, chose the latter option. Since the company offers cheaper sodas than its competitors Coca-Cola and Pepsi-Cola, Macay Holdings wanted to maintain its competitive advantage.

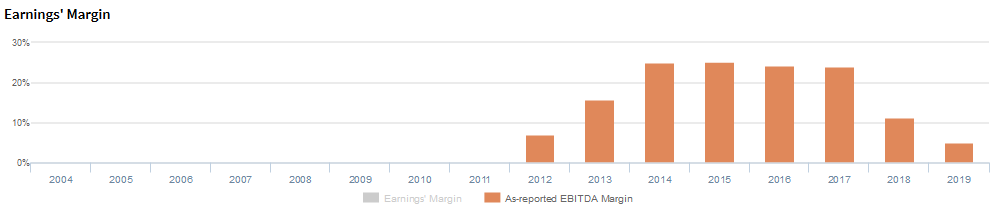

Macay Holdings has been able to generate a profit each year despite the new excise tax, but the firm’s as-reported margins have drastically collapsed. From 2017 to 2019, as-reported margins dropped from 24% to only 5%.

However, even with such a steep decline, as-reported metrics are presenting Macay Holdings’ margins to still be strong. In reality, when looking at the firm’s Uniform margins, it eroded much quicker from 22% in 2017 to a historical low of 1% in 2019.

As-reported metrics overstate Macay Holdings’ cost efficiency primarily because of how interest income, among many other accounting distortions, is treated.

Interest income arises from the earnings related to the firm’s investment in stocks, deposits, and associates/affiliates, which are not essential to the company’s core operations. Therefore, interest income should be subtracted from a company’s earnings.

In 2019, Macay Holdings recognized PHP 80.9 million of interest income from its bank deposits, making up a third of its net income.

Removing PHP 80.9 million from Macay Holdings’ earnings along with the many other adjustments made leads to just 1% Uniform earnings margin in 2019, lower than as-reported earnings margin of 5%.

Macay Holdings’ historical earning power is stronger than you think

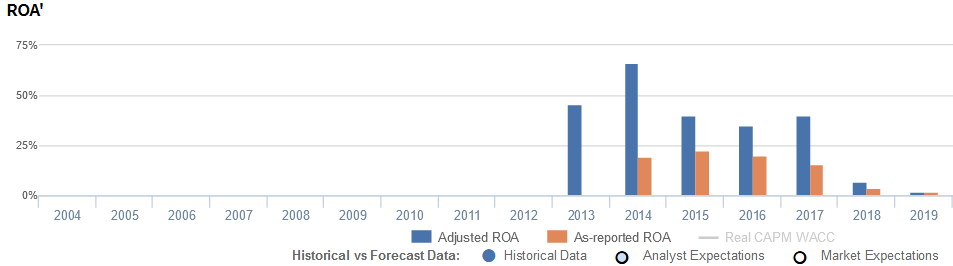

As-reported metrics distort the market’s perception of the firm’s profitability prior to 2019. If you were to just look at as-reported ROA, you would think Macay Holdings’ profitability has been relatively stable without notable years of high profitability from 2014-2018.

In reality, Macay Holdings’ true profitability had been higher than its as-reported ROA. Specifically, as-reported ROA peaked at only 23%, but Uniform ROA had gone as high as 66%.

As-reported ROA rose from 19% in 2014 to 23% in 2015, before declining to 16% in 2017 and dropping further to just 2% in 2019.

Meanwhile, after contracting from 66% in 2014 to 35% in 2016, Uniform ROA recovered to 40% in 2017, but has since collapsed to a low of 2% in 2019.

Macay Holdings’ historical asset turns are stronger than you think

Strength in Uniform ROA has historically been driven by strong Uniform asset turns, offset by weak Uniform earnings margin. In fact, Uniform turns have been higher than as-reported asset turnover in each of the past seven years.

As-reported asset turnover rose from 0.8x in 2013 to 1.5x levels in 2014-2015, before declining to 0.8x in 2018 and subsequently recovering to 1.1x in 2019.

Meanwhile, Uniform turns drastically fell from a peak of 4.7x in 2013 to 1.8x in 2015, before improving to 2.1x in 2016. Thereafter, Uniform turns contracted to 1.2x in 2018, before rebounding to 1.5x in 2019.

Looking at the firm’s turns alone, as-reported metrics are making the firm appear to be a less asset efficient business than is accurate.

SUMMARY and Macay Holdings, Inc. Tearsheet

As the Uniform Accounting tearsheet for Macay Holdings (MACAY:PHL) highlights, the Uniform P/E trades at 43.8x, which is above corporate averages, but below its own history.

High P/Es require high EPS growth to sustain them. However, in the case of Macay Holdings, the company has recently shown an 83% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Macay Holdings’ sell-side analyst-driven forecast calls for a 116% Uniform EPS growth in 2020 and 16% Uniform EPS decline in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Macay Holdings’ PHP 8.78 stock price. These are often referred to as market embedded expectations.

The company needs to grow Uniform earnings by 29% each year over the next three years to justify current valuations. What sell-side analysts expect for Macay Holdings’ earnings growth is well above what the current stock market valuation requires in 2020, but below that requirement in 2021.

Furthermore, the company’s earning power is below the long-run corporate averages. That said, cash flows and cash on hand are more than 3x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Macay Holdings’ Uniform earnings growth is well above peer averages, and the company is trading well above peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com