This stock lights people’s homes, but its future is dim. True ROA can’t power as-reported 8% levels.

With a natural monopoly on a household and business need for at least 6.6 million people, you would think that this stock company is one of the most profitable in the country.

It’s not.

A quick industry analysis points out that the utilities sector this company operates in is plagued by regulations and government oversight, significantly inhibiting their earning potential.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earning Tearsheets – Philippine-listed Focus

Powered by Valens Research

During the Spanish colonial period, horses were the engines driving transportation and commerce in the Philippines.

We see this exemplified in Jose Rizal’s Noli Me Tangere. In Crisostomo Ibarra’s own carriage en route to visit his father’s burial site, he observed the streets of Manila bustling with carriages, carromatas, and calesas going about their business.

Industrialization slowly reached the country’s shores and horses were gradually phased out to make way for the steam engine.

The sequel El Filibusterismo mirrored this progress 13 years later as Spanish control neared its end, with Simoun and the other main characters aboard a steamboat voyaging through the Pasig river.

Modernization of the Philippines continued its advancement under the American regime. Concerted efforts were made for electric motors to power transportation and households.

The Taft Commission granted a franchise to an entrepreneur named Charles M. Swift, to combine Manila’s electricity distribution and tramway system.

From this, the Manila Electric Railroad And Light Company was born, or as it is more commonly known today, MERALCO (or Meralco).

Even to this day, Meralco is a company as recognizable as any in the metro, but historically remembered for getting caught up in the chaos of politics.

Most of Meralco’s assets were either destroyed or stripped away when the Japanese invaded.

Decades after, the Lopez family acquired the company, only to be nationalized later by President Marcos as part of the declaration of martial law.

Subsequent President Cory Aquino returned ownership back to the Lopez family, but the company had to surrender its transport business to a different government authority.

Meralco went public when conditions seemed to have normalized, but a new set of problems emerged.

Difficulties in addressing the surging demand for electricity forced the company to conduct unpopular planned blackouts. They also had to deal with government investigations, accused of charging rates that were too high.

Investors who are now looking at the as-reported financials may be pleased upon seeing that Meralco has performed well in the past decade, their rocky past now behind them.

Investors looking at the Uniform Accounting numbers share similar sentiments, but to a lesser degree.

This marked difference lies in how both sets of investors look at operating leases.

Pre-2019 IFRS and GAAP accounted for operating leases by spreading the cost of the asset expense over several years without requiring recognition in the balance sheet.

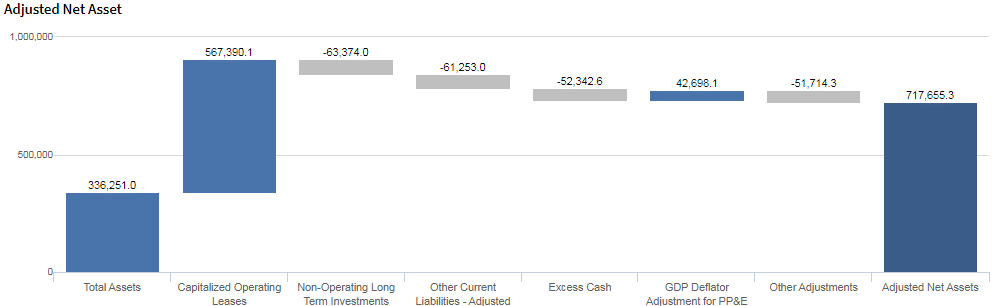

A lot of companies, including Meralco, opted for this “off balance sheet financing” to show higher return on assets (ROA) from the lower reported asset base.

Uniform Accounting has taken care of this by adding operating lease expense back to earnings and capitalizing the asset.

Doing so for Meralco shows us that in 2018 alone, they were materially underreporting their assets by more than 1.5x!

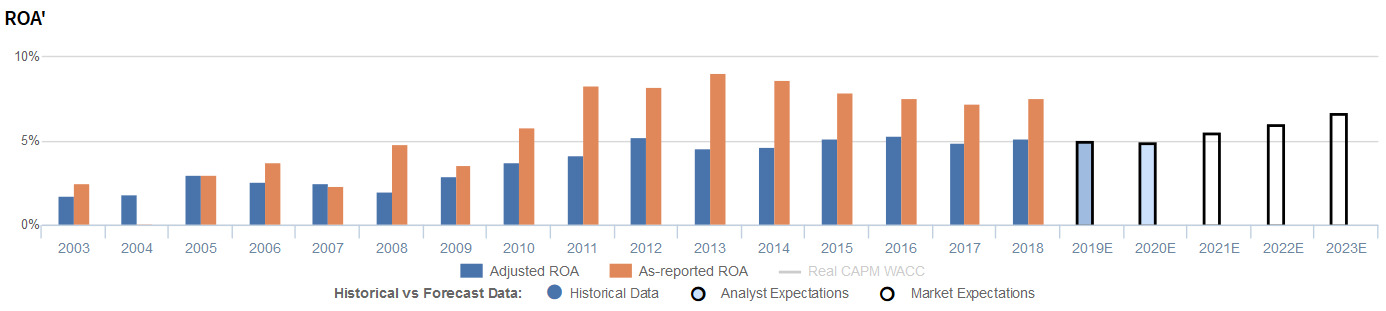

Meralco’s earning power is weaker than you think

Historically, Meralco has seen cyclical and generally low profitability, which is characteristic of a utilities firm. From 2003, Uniform ROA (blue bars) was at a low of 2% before hitting a peak of to 3% levels 2005, only to fall back to its low levels in 2008.

The as-reported ROA (orange bars) will tell you that the company managed to double and achieve near cost of capital ROA levels in 2008. From 2010 onwards, Meralco saw their earning power rise to historical highs and maintain 5% levels.

As-reported metrics would have you believe that Meralco has been performing above corporate average levels when in reality, the company has never surpassed 6% levels.

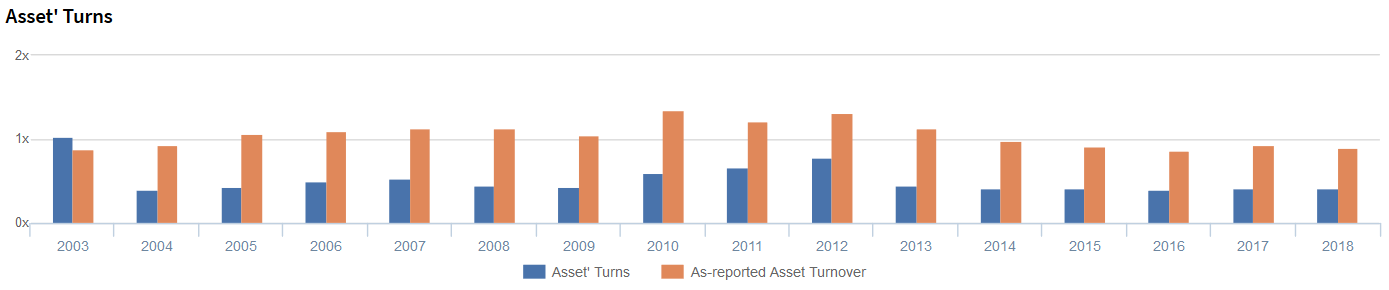

Meralco’s asset turns are a lot worse than you think

The weak performance of their ROAs is a result of the firm’s inability to offset declines in Uniform Asset Turns with sufficient improvements in Uniform Earnings margin. This implies that the company is less concerned about generating sales and managing expenses.

Since 2009, the difference between Meralcos’s Uniform and as-reported ROA has grown wider, as did the difference between their Uniform and as-reported asset turns.

To illustrate, the as-reported asset turns for Meralco have been 0.9x-1.0x since 2014, which is more than double Uniform Turns of 0.4x, making Meralco appear to be a much stronger business than real economic metrics highlight.

Moreover, as-reported asset turns have been almost twice as much as Uniform asset turns since 2004, significantly distorting the market’s perception of the firm’s historical profitability levels.

SUMMARY and Meralco Tearsheet

As our Uniform Accounting tearsheet for Manila Electric Company highlights, Meralco P/E trades above market averages at 25.2x, but below its historical averages.

High P/Es require high EPS growth to sustain them. In the case of Meralco, the company has recently shown a 12% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Meralco’s sell-side analyst-driven forecast is for Uniform earnings to grow at 5% in 2019, followed by a more sluggish growth of 2% in 2020.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify PHP318 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels of Meralco, the company would need to have Uniform earnings grow by 4% each year over the next three years.

What sell-side analysts expect for Meralco’s’ earnings growth is in line with what the current stock market valuation requires.

To summarize, Meralco’s Uniform earnings growth is in line with peer averages in 2019. However, the company is trading above average peer valuations.

The company’s earning power is slightly below the corporate average, but the company has low dividend risk given their available cash. This signals that their cash flow risk to the company’s operations and credit profile in the future is low.

About the Philippine Market Daily

“Tuesday Uniform Earning Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com