This telco giant keeps you connected across the globe. At 1.1x Uniform P/B, the market is signalling bearish expectations.

One of the most successful investors, Warren Buffett, is famous for saying: Be fearful when others are greedy, and be greedy when others are fearful.

Evidenced by the market sell-off in the past couple of weeks, investors have become fearful of the stock market and have resorted to other ways of keeping their money safe.

The PSE had to shorten trading hours and reduce the lower static threshold as even recession-proof industries were being dragged down.

There’s no reason to believe that this telecom giant will see reduced demand in the coming months, so should we be greedy or fearful on this stock?

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

As the government continues to make efforts to flatten the COVID-19 curve, many establishments have suspended operations.

The exceptions are those industries that offer essential goods and services such as utilities, grocery and drug retail, and hospitals.

These industries are said to be more resilient, and they might even benefit from the quarantine period.

Globe Telecom, Inc.(GLO:PHL), one of the two largest telecommunication services in the Philippines, plays a key role in making the lives of Filipinos easier amid this pandemic.

Access to the internet enabled a large number of companies to test how well their business can still run under a work-from-home scenario.

Those who have adopted a work-from-home setup are now using text messaging, e-mails, and online video calls to easily collaborate with their co-workers in completing their tasks and projects.

On the other hand, people who are on work leave are choosing indoor activities to keep the family entertained, with the prominence of video streaming, online gaming, and social media browsing.

Within the first two weeks of community quarantine, the telecoms reported an increase in mobile data demand. Specifically, Globe saw a surge in mobile data traffic, voice calls, and SMS.

Globe responded to the increase in demand by offering more promos and additional data to help customers maintain connection at home.

This action is expected to increase Globe’s sales in the following months, and depending on how many companies permanently adopt a work-from-home system, this might increase sales beyond 2020 as well.

However, a point of contention is whether Globe’s facilities have the capacity to keep up with the increase in demand as many have criticized their broadband’s speed and quality.

Over the years, the company has made a lot of investments in its network to support the increasing demand for data-related services, which accounts for 65% of the company’s revenues.

In the past two years, they have also been aggressively utilizing fixed wireless solutions.

In 2019, the company spent a record capex of PHP 51.0 billion, an 18% increase from spending a year ago. This spending was mostly allotted to putting up 139% more sites, and adding 28% more 3G and 4G base stations.

This has driven Globe to enjoy 84% of fixed wireless broadband subscriber market share in 2019, while also enjoying a 53% market share of mobile subscribers.

The company now has more mobile subscribers than its major competitor PLDT, having a total of 94 million subscribers compared to PLDT’s 73 million subscribers as of 2019.

Furthermore, such a large asset base and subscriber base makes it more difficult for any entrant of the telecom industry to disrupt the current duopoly.

Regardless, Dito Telecommunity, having recently granted a permit to operate by President Duterte, plans to launch as the country’s third telecommunications provider in 2021.

With Dito’s entry, the competition may become more intense.

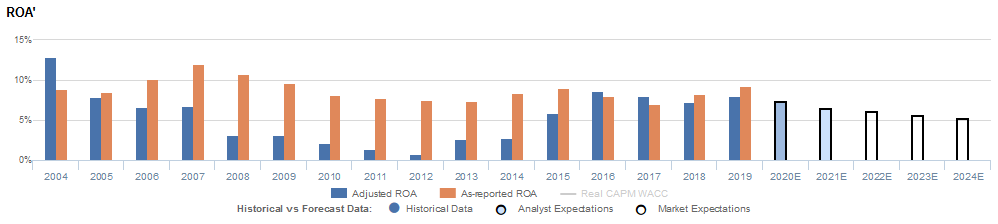

Though recent Uniform metrics show slightly less profitability than what as-reported financials state, trends in Uniform earning power have better reflected the firm’s true economic profitability.

Only in 2015 did Globe’s Uniform earning power surpass cost-of-capital levels again since 2007. Meanwhile, as-reported ROA claims that Globe has always been above cost-of-capital levels since 2004.

The overstatement of as-reported ROA lies in the failure to adjust Globe’s property, plant, and equipment (PPE) for inflation. While their cash flows are reported in current PHP, their PPE is recorded at historical costs.

Failure to adjust PPE to the current purchasing power each year results in a mismatch of ROA calculation, except for the highly unlikely case of a 0% inflation environment.

Market expectations are for Globe’s earning power to decline

Globe currently trades below recent averages relative to Uniform assets, with a 1.1x Uniform P/B (V/A’). At these levels, the market has bearish expectations for the firm, projecting Uniform ROA to decline to 5% levels through 2024, accompanied by 2% Uniform asset growth.

Analysts have similar expectations, projecting Uniform ROA to decline to 7% levels by 2021, accompanied by 5% Uniform asset growth.

Historically, Globe has seen cyclical profitability. Uniform ROA fell from 13% in 2004 to a 1% trough in 2012 as Typhoon Haiyan damaged their cell sites.

Since then, Uniform ROA has been improving, reaching new highs of 9% levels in 2016, before stabilizing at 7%-8% levels in 2017-2019.

Globe’s earnings margin is expected to decline

Trends in Uniform ROA have largely been driven by similar trends in Uniform earnings margin.

From 2004 to 2012, Uniform earnings margin continuously declined from peak 26% to a low of 2%. Then Uniform margins started to recover, reaching 17% levels in 2016-2017, before fading slightly to 16% in 2019.

Every year, as-reported earnings margins have been overstated, making the company appear to be a much stronger business than real economic metrics highlight.

At current valuations, markets are pricing in expectations for declines in both Uniform earnings margin and Uniform asset turns.

SUMMARY and Globe Telecom, Inc. Corporation Tearsheet

As our Uniform Accounting tearsheet for Globe highlights, Uniform P/E trades at 15.0x, which is below the market average but around its historical average levels.

Low P/Es require low EPS growth to sustain them. In the case of Globe, the company has recently shown a strong 20% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Globe’s sell-side analyst-driven forecast is to see Uniform earnings growth of 1% in 2020, before a 10% shrinkage in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify PHP 1,949.00 per share. These are often referred to as market embedded expectations.

To meet the current market valuation levels of Globe, the company would need to shrink its Uniform earnings by 7% each year over the next three years.

What sell-side analysts expect for Globe’s earnings growth is slightly above what the current stock market valuation requires in 2020.

The company’s earning power is above the corporate average, while the company has average dividend risk, with cash flows and cash on hand below total obligations.

To conclude, Globe’s Uniform earnings growth is above peer averages in 2019, and the company is trading below peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com