This toy maker isn’t kidding around with its profitability. Its 14% Uniform earning power is higher than as-reported ROA might have you think.

Struck by the COVID-19 global pandemic, President Rodrigo Duterte has declared a nationwide enhanced community quarantine a week ago, forcing Filipino citizens to stay in their homes.

Having been used to going out to entertain themselves, Pinoys who aren’t working from home are constantly looking for things to engage in. With kids especially, who are already normally restless, parents are trying to find better ways to entertain them other than by lending their phones or iPads.

This company manufactures electronic learning products for infants, toddlers, and kids. With their award-winning products, children can have fun learning while staying at home during the community quarantine.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

What was once a staff of 40 employees is now a 26,000-strong multinational company for children’s toys.

Video Technology Limited was founded in Hong Kong by Allan Wong and Stephen Leung in 1976. By 1978, the company was called VTech and had launched its first product, a home TV game console. The company then focused on manufacturing video games during the rest of the 70s.

VTech then revolutionized the tech space in 1980 by introducing its first electronic learning product called Lesson One, which had the ability to teach children basic spelling and math.

Along with this product, their first personal computer (PC) was introduced, and throughout the 80s, this became their main product.

Although VTech’s PCs gained traction in Japan and North America, the company became caught up in a brutal price war and in a battle for shelf space at the beginning of the 90s.

Although this forced the company to sell off its computer division, leaving room for it to be sold only in Hong Kong, this allowed the company to seize a new opportunity.

In 1991, VTech launched its first cordless telephone. The company was among the very few Hong Kong-based companies to generate rising sales and profits amid the Asian financial crisis.

Furthermore, even with the production of these telephones accounting for over 60% of their sales, the company never forgot about its electronic learning aid division which brought its name to the market.

With the changing times, VTech responded to the emergence of video game consoles by releasing a TV Learning System called V.Smile.

Their very own game console garnered huge success and featured licensing agreements with big brands such as Disney, Marvel, Hit Entertainment, Warner Brothers, and more.

Today, VTech is a world-leading manufacturer of the two core product categories: cordless and corded telephones, and electronic learning products.

In addition, it is a major original equipment manufacturer (OEM) for brands such as Sony and Philips.

VTech has established its brand by sticking to its strategy of product innovation through the continuous integration of technology and creative new ideas.

With the purpose of cultivating a fun learning experience for children during their developmental phase, the company continues to pave the way in the learning toy industry by consistently producing high-quality and innovative products.

As a result, VTech continues to receive several prestigious awards, with Myla the Magical Unicorn™ and Mix & Match-a-Saurus™ selected as finalists for the 2020 Toy of the Year (TOTY) Awards.

In this digital age, where social media platforms such as YouTube and TikTok are this generation’s main source of entertainment, the company is set to release a new product at the 2020 North American International Toy Fair.

KidiZoom® Creator Cam was added as an expansion to their Kidi line of kid-friendly electronics, which allows kids to create their own video content with several fun editing features.

Thanks to their continuous product development and innovation, VTech’s Uniform ROA has been robust and stronger than as-reported ROA.

Uniform ROA has been consistently higher than as-reported ROA for the past fourteen years. Currently, VTech reported a 14% Uniform ROA in 2019, greater than as-reported ROA of 11%.

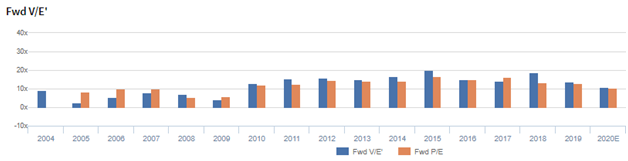

VTech’s Uniform valuation is in line with market valuations

VTech Holdings Limited (303:HKG) currently trades well below corporate averages with a 10.8x Uniform P/E (blue bars), but in line with the as-reported P/E of 10.5x (orange bars).

At these levels, the market is pricing in expectations for Uniform ROA to decline to 8% in 2024, accompanied by a 2% Uniform asset growth going forward.

However, analysts have more bullish expectations, projecting Uniform ROA to increase to 15% levels in 2021, accompanied by a 1% Uniform asset growth.

VTech’s profitability is actually better than you think it is

As-reported metrics are understating VTech’s profitability.

For example, as-reported ROA was 11% in 2019, lower than Uniform ROA of 14%. Uniform ROA has been higher than as-reported ROA in fourteen of the past sixteen years. As-reported ROA is making the company look like a weaker business than real economic metrics highlight, distorting the market’s perception of the firm’s historical profitability trends.

VTech’s Uniform ROA ranged from 5% to 31% over the past sixteen years. From a historical low of 5% in 2007, Uniform ROA peaked at 31% in 2008 before fading back to 21% in 2009. It recovered to 28% in 2010, and declined gradually to 14% in 2019.

Summary and VTech Holdings Limited Tearsheet

As the Uniform Accounting tearsheet for VTech highlights, they are trading at 10.8x Uniform P/E, which is below global corporate average valuations and its historical average levels.

Low P/Es require low EPS growth to sustain them. In the case of VTech, the company has recently shown a 19% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Hong Kong Accounting Standards (HKAS) earnings and convert them to Uniform earnings forecasts. When we do this, VTech’s sell-side analyst-driven forecast is for Uniform earnings to grow by 11% in 2020 and 5% in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify HKD 68.15 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels of VTech, the company would have to have Uniform earnings shrink by 10% each year over the next three years. What sell-side analysts expect for VTech’s earnings growth is well below what the current stock market valuation requires.

To conclude, VTech’s Uniform earnings growth is below peer averages in 2020 and the company is trading higher than peer average valuations.

The company’s earning power, based on its Uniform return on assets calculation, is 2x greater than corporate average returns. Furthermore, with cash flows and cash on hand consistently exceeding obligations, VTech has low credit and dividend risk.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com