This UITF generated returns TWICE its benchmark and Uniform Accounting shows its portfolio may see further equity gain in the long term

This bank emerged from a small commercial bank to a key capital provider in the Philippine coconut industry, to one of the country’s top 15 banks in terms of assets.

One of its notable products—its equity unit investment trust fund—has delivered investment returns better than its benchmark, the Philippine Stock Exchange Index (PSEi).

Both the UITF and the PSEi made huge runs over the past 10 years. However, during the first quarter of 2020, both declined and are expected to remain subdued in the near term due to COVID-19-related concerns. However, over the long term, Uniform Accounting gives investors a better investment perspective.

In today’s Philippine Markets Daily (PMD), we take a look at the bank’s equity trust fund and assess the profitability and growth potential of its major non-financial holdings.

In addition, we’re including fundamental analysis of one of the fund’s largest holdings, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Philippine Markets Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

United Coconut Planters Bank, commonly referred to as UCPB, was known for providing financial services primarily to coconut farmers in the country beginning in the late 1970s.

Established on May 15, 1963, UCPB started off as a small commercial bank called the First United Bank. It was founded by Jose Cojuangco, the father of the 11th President of the Philippines, Maria Corazon “Cory” Cojuangco Aquino.

In the face of increasing coconut production in 1975, the Philippine Coconut Authority (PCA) acquired First United Bank to provide readily available funds to coconut producers. First United Bank was then renamed to United Coconut Planters Bank.

Since then, UCPB has been acknowledged for uplifting the quality of life of Filipinos living in coconut communities. UCPB, together with the Coconut Industry Investment Fund (CIIF), implements community-building activities, credit programs, and scholarship grants in coconut communities across 64 provinces.

Apart from its community development initiatives, UCPB has also been known for its efforts to expand its banking capabilities and provide innovative products and services to its customers.

UCPB was the country’s first private bank to become a universal bank. It was also one of the first few banks to introduce an automated teller machine (ATM) service in the late 1980s.

In addition, UCPB was among the first banks to offer UITF products, since the shift from common trust funds (CTFs) to unit investment trust funds (UITFs) in September 2004.

With the goal of providing long-term investment growth, UCPB launched the UCPB Equity Fund (UEF) on January 15, 2007. UEF is an equity trust fund that invests in companies listed in the Philippine Stock Exchange, with the Philippine Stock Exchange Index as its benchmark.

UEF saw a rough start in the midst of the global economic downturn, falling 17% from its PHP 1.00 NAVPU in Jan 2007 to a PHP 0.83 NAVPU in January 2009. The PSEi performed worse, plunging 35% from 3,019.06 points to 1,954.97 points over the same period.

After that decline, as the global economy recovered, the fund took off and registered a record PHP 4.15 NAVPU in April 2015. This translated to a massive 402% investment return, outperforming the PSEi’s 316% growth over the same time frame.

However, Greece’s debt crisis and the economic slowdown in China stirred up concerns across the globe. This dragged UEF’s NAVPU down to PHP 3.49 by the end of 2015. Moreover, due to investment outflow driven by uncertainties around the Federal Reserve’s tightening interest rate hike cycle and the United States’ new administration, the fund NAVPU fell further by the end-2016 to PHP 3.10, a 25% investment loss from its peak in April 2015.

The PSEi saw a similar but less volatile pattern, falling from 8,127.48 points in April 2015 to 6,658.20 points in December 2016, a decline of 18%.

In the following years, the fund and the country’s equity market in general saw increased stock price fluctuation due to mixed sentiments brought about by improving domestic economic fundamentals, US-China trade tensions, and regulatory risks around concessionaires. UEF rose to PHP 3.91 NAVPU in December 2017, before dipping at PHP 3.29 NAVPU in November 2018 and stabilizing at PHP 3.62 NAVPU in December 2019. Similarly, the PSEi skidded to 6,843.83 points before rising to 7,815.26 points by the end of 2019, with both the fund and its benchmark totaling to a gain of 17%.

Recently, due to the fears brought about by the COVID-19 pandemic, the fund plunged to PHP 2.63 NAVPU on March 31, 2020, suffering an investment loss of around 27%. The PSEi performed worse, incurring an investment loss of around 31% YTD.

The uncertainties around the COVID-19 pandemic and the extreme measures the government has been implementing to contain it are expected to cause continued disruption in business operations. This will also result in further short-term stock price volatility across multiple companies and industries, including the companies that UEF invests in.

UEF picks companies with sound long-term fundamentals. This has been one of the reasons why the fund has been beating its benchmark. In fact, as of March 31, 2020, UEF has provided a cumulative investment return of 163% since its inception; this is 2x the PSEi’s 76% growth over the same horizon.

However, by looking at as-reported numbers, investors won’t be able to understand the true underlying performance of companies. Worse, it could lead one to generating skewed insights, negatively affecting the investment decision making process.

With Uniform Accounting, investors can see the real profitability and earnings expectations of companies.

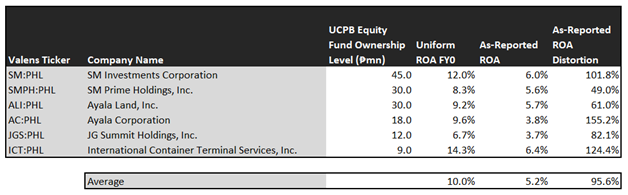

The table below lists the top non-financial holdings of UEF along with their Uniform return on assets (ROA), as-reported ROA, and ROA distortion—the difference between Uniform and as-reported ROA.

As-reported numbers show that most of UEF’s holdings are not profitable, with as-reported ROA ranging below cost of capital returns. However, Uniform Accounting reveals that in reality, these companies are generating economic profit.

Traditional metrics imply that this fund is subpar with an average as-reported ROA of 5%, below global corporate average returns of 6%. Under the Uniform Accounting framework though, this fund has actually delivered stronger earnings with an average Uniform ROA of 10%.

Uniform Accounting adjusts for the misrepresentations in companies’ financial statements brought about by the inconsistencies in the Philippine Financial Reporting Standards (PFRS), to reveal the true underlying performance of companies.

As such, it should not be surprising that when analyzing the non-financial holdings of the UEF, the figures that easily stand out are the double-digit discrepancies between Uniform ROA and as-reported ROA for these companies.

While the difference in raw figures may not seem too distant, the distortion in percentage ranges from 49% to 155%, with Ayala Corporation (AC:PHL), International Container Terminal Services, Inc. (ICT:PHL), and SM Investments Corporation (SM:PHL) having distortions greater than a hundred percent.

As-reported ROA understates the earning power of Ayala Corporation, treating it as a low-quality company with a 4% as-reported ROA. In reality, it is a high-quality firm with a 10% Uniform ROA, higher than global corporate average returns. This leading conglomerate has actually never seen its profitability dip below 10% over the past decade.

Meanwhile, as-reported numbers incorrectly suggest that ICT is an average firm with an as-reported ROA of 6% when in fact, it is an above-average firm with 14% Uniform ROA. This global port management company has consistently generated double-digit Uniform ROA over the past 10 years.

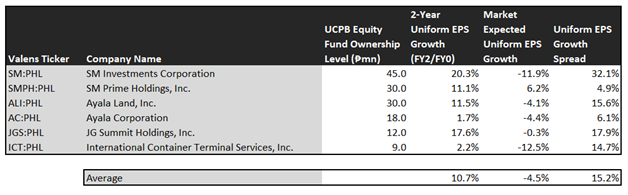

This table shows the earnings growth expectations for the major company ownerships of UEF. It features three key data points:

- The 2-year Uniform EPS growth represents the Uniform earnings growth the company is likely to have for the next two years. The earnings number used is the value of when we convert consensus sell-side analyst estimates to the Uniform Accounting framework.

- The market expected Uniform EPS growth represents what the market thinks Uniform earnings growth is going to be for the next two years. Here, we show by how much the company needs to grow Uniform earnings in the next two years to justify the current stock price of the company. This is the market’s embedded expectations for Uniform earnings growth.

- The Uniform EPS growth spread is the difference between the 2-year Uniform EPS growth and market expected Uniform EPS growth.

On average, Philippine companies are expected to have 6% annual Uniform earnings growth over the next two years. Meanwhile, the UEF’s top holdings are forecast to surpass that, with 11% projected Uniform earnings growth in the next two years.

The market, on the other hand, sees a decline in earnings for these companies with market-expected Uniform EPS shrinkage of 5% over the next two years.

Among these companies, SM Investments Corporation, JG Summit Holdings, Inc. (JGS:PHL), and Ayala Land, Inc. (ALI:PHL) have the highest Uniform earnings growth dislocation.

The market is pricing SM’s Uniform earnings to plummet by 12% in the next two years. However, sell-side analysts are seeing earnings growth expansion for the firm, forecasting it to accelerate by 20% going forward.

Similarly, the market is seeing JGS’s uniform earnings to remain flat, but analysts are projecting a robust 18% earnings growth for the firm in the next two years.

As-reported metrics are understating the fund’s overall profitability, while the market has bearish earnings growth expectations over the funds’ major holdings in the face of the COVID-19 pandemic. This could lead to investors thinking that UEF has a subpar portfolio with unexciting earnings projection.

However, in reality, this fund has healthy profitability levels with an average Uniform ROA of 10% and robust earnings growth potential with 11% Uniform EPS growth in the next two years.

With Uniform Accounting, investors can see through black swan events such as the COVID-19 pandemic, revealing the companies’ underlying fundamentals for what they truly are.

While this fund may see continued volatility in the short term, Uniform metrics reveal that this fund invests only in high quality companies with strong fundamentals, which could point to long-term equity upside.

Ayala Land, Inc. Tearsheet

Today, we’re highlighting one of the largest individual stock holdings in UEF—Ayala Land, Inc.

As the Uniform Accounting tearsheet for Ayala Land highlights, it trades at a Uniform P/E of 16.6x, below global corporate averages and its historical averages.

Low P/Es require low, and even negative, EPS growth to sustain them. In the case of Ayala Land, the company has recently shown a 1% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that poorly track reality. However, sell-side analysts have a strong grasp on near-term financial forecasts like revenue and earnings.

We take sell-side forecasts for PFRS earnings as a starting point for our Uniform earnings forecasts. When we do this, Ayala Land’s sell-side analyst-driven forecast shows that Uniform earnings will grow by 1% in 2020 and 23% in 2021.

Based on the current stock market valuations, we can back into the required earnings growth rate that would justify PHP 32.00 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels of Ayala Land, the company would have to see Uniform earnings shrink by 4% each year over the next three years. Sell-side analysts’ expected 23% earnings growth for the company is well above what the current stock market valuation requires.

The company has an earning power at least 1.5x the long-run corporate averages—based on its Uniform ROA calculation. Additionally, since the company’s combined cash flows and cash on hand are way above obligations within five years, Ayala Land has no dividend risk.

To conclude, Ayala Land’s Uniform earnings growth is above peer averages in 2020. Moreover, the company is trading below peer average valuations.

About the Philippine Market Daily

“Friday Uniform Portfolio Analytics”

Investors who don’t engage in the buying or selling of securities for a living oftentimes rely on professionals to manage their own investments within the scope of their investment policies.

With so many funds and managers out there, it can get confusing and difficult to decide which one best suits your needs as an investor.

Every Friday, we focus on one fund in the Philippines and take a deeper look into their current holdings. Using Uniform Accounting, we identify the high-quality stocks in their portfolio which may not be obvious using the as-reported numbers.

We also identify which holdings may be problematic for the fund’s returns that they would need to reconsider from a UAFRS perspective.

To wrap up the fund analysis, we highlight one of their largest holdings and focus on key metrics to watch out for, accessible in our tearsheets.

Hope you’ve found this week’s focus on UEF interesting and insightful.

Stay tuned for next week’s Friday Uniform Portfolio Analytics!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com