Uniform Accounting shows how this food packaging company can preserve its robust ROA

Canned goods are pretty much a staple on the grocery list, even more so these days while the Philippines is generally still on quarantine.

With this company’s diverse set of brands, its products can be easily found anywhere, from the neighborhood sari-sari store to the nearest supermarket. This is why it has been able to generate robust UAFRS-based (Uniform) profitability.

However, as-reported metrics aren’t reflecting a similar performance, falsely claiming the company’s profitability to be much weaker.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

At the beginning, canned meat used to only be eaten when their fresh alternative was hard to come by. In fact, canning was specifically invented during wartime so that food did not spoil en route to the front lines, while outlasting the winter season.

With modernization, the perception of canned food changed. In the Philippines, many see canned food as an essential breakfast item and an easy to make packed lunch for students and workers.

Aside from its convenience and long shelf life, further innovations made canned food cheaper, making it a preferred choice over its fresh counterpart, for many people.

Canned food has even become such a popular food choice that supermarkets often dedicate more than one aisle for canned goods, filled with corned beef, sardines, and many others. Over time, food manufacturers even developed different kinds of flavors for canned meats, creating demand for new products within the category.

Century Pacific Food, Inc. (CNPF:PHL) is one of the largest players in this space, beginning as a manufacturer of canned tuna and then venturing into other packaged food and beverages.

The company started as a family business in 1978, focusing on canning, processing, manufacturing, and exporting tuna products to leading international brands.

After five years in the tuna business, Century Pacific entered the growing Philippine sardine market by launching 555 Sardines, its first branded product.

Century Pacific proceeded to expand its tuna business in 1986 by creating Century Tuna, its flagship product. A decade later, the company branched out to other meat-based products, entering the corned beef market with Argentina Corned Beef in 1995.

The company also made a number of key acquisitions over the next several years, notably premium corned beef brand Swift and milk powder brand Birch Tree Full Cream Milk Powder.

Together with its other brands, Century Pacific has been able to create an extensive portfolio, becoming one of the largest food manufacturers in the country.

By May 2014, the company conducted an IPO, allowing the firm to raise funds for further expansion and creating a platform to broaden its food business.

Century Pacific made three notable acquisitions in 2016: the North American license for the leading Filipino shrimp paste brand-Kamayan, full control of Century International (China) Group, and an integrated coconut producer to diversify its private label export business.

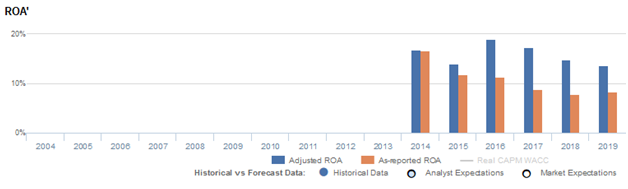

These 2016 acquisitions helped increase the firm’s earnings by nearly 40%, driving their 3x cost-of-capital Uniform ROA of 19% for the year. However, Century Pacific’s Uniform ROA has gradually declined since then due to higher prices for raw materials, reaching 14% in 2019.

Although the company’s profitability has been trending downwards since its peak in 2016, it is still at least 2x cost-of-capital levels.

Additionally, the company has actually benefited from the current COVID-19 pandemic. In Q1 2020, Century Pacific posted a 31% increase to PHP 1.03 billion net income from PHP 793 million in Q1 2019.

Still, as-reported metrics fail to reflect how important this company’s products are to everyone. As-reported financials show much less profitability than what Uniform metrics reveal, understating the company’s TRUE earning power.

In 2019, as-reported metrics posted only an 8% ROA, but when removing the accounting distortions, Century Pacific’s Uniform earning power is significantly higher at 14%.

One of the main contributing factors is how Philippine Financial Reporting Standards (PFRS) accounts for interest expense.

In PFRS, interest expense is treated as an operating cash flow. In reality, interest expense represents the cost of debt and should be categorized as part of cash flow from financing. As such, in Uniform Accounting, interest expense is added back to earnings.

In Century Pacific’s case, it recognized an interest expense of PHP 369 million in 2019. When we add this expense back to earnings since it is not an operating expense, net income increases.

Performing this adjustment along with the many other adjustments Valens makes, we arrive at a TRUE earning power of 14%.

Century Pacific’s earning power is stronger than you think

Through Uniform Accounting, we see that as-reported metrics significantly distort the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than what real economic metrics reveal.

Uniform ROA has actually been higher than as-reported ROA for the past five years. In 2019, Uniform ROA was 14%, significantly higher than as-reported ROA of 8%.

After its IPO in 2014, Century Pacific’s profitability declined from 17% to 14% in 2015. A year later, the company’s earning power reached peak levels of 19% due to synergies created by its acquisitions that year. However, Uniform ROA gradually declined starting 2017 until its current lowest level of 14% in 2019.

On the other hand, as-reported metrics only show a steady decline in ROA since 2014, from 17% to 8% levels in 2018-2019, nearly half of what Uniform Accounting shows.

Century Pacific is a more efficient business than you think

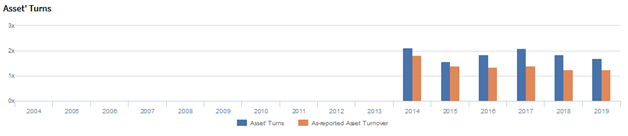

Similarly, as-reported metrics significantly distort the firm’s asset efficiency, a key driver of profitability.

In 2019, as-reported asset turnover was 1.2x compared to Uniform asset turns of 1.7x, making the company appear to be a less efficient business than real economic metrics highlight.

Moreover, as-reported asset turnover has been lower than Uniform turns each year for the past six years, distorting the market’s perception of the firm’s historical asset efficiency level.

SUMMARY and Century Pacific Food, Inc. Corporation Tearsheet

As our Uniform Accounting tearsheet for Century Pacific highlights, Uniform P/E currently trades at 16.9x, which is below the market average and the company’s historical average.

Low P/Es require low EPS growth to sustain them. In the case of Century Pacific, the company has recently shown a 2% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Century Pacific’s sell-side analyst-driven forecast calls for 27% Uniform earnings growth in 2020, followed by 8% Uniform earnings growth in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify PHP 15.28 per share. These are often referred to as market embedded expectations.

To meet the current market valuation levels of Century Pacific, the company would only need to immaterially grow its Uniform earnings over the next three years.

What sell-side analysts expect for the company’s earnings growth is far above what the current stock market valuation requires.

In addition, the company’s earning power is 2x the corporate average, and the company has moderate dividend risk, with cash flow and cash on hand materially above their debt obligations beginning 2021.

To conclude, Century Pacific’s Uniform earnings growth is above peer averages in 2020, and the company is trading below peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com