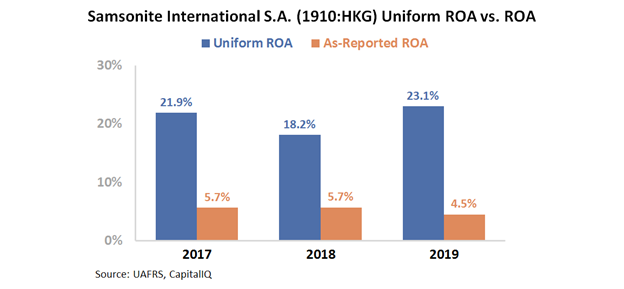

With its sustainability initiatives, the “Samson” of the luggage industry is more powerful with a 23% Uniform ROA, not 5% as-reported!

With increased temperatures, rising sea levels, and extreme weather patterns, climate change is a pressing issue that affects everyone everywhere.

For years, there has been a call for a transformation to a sustainable lifestyle, and this company headquartered in Hong Kong plays its part by putting sustainability on the forefront of its business processes.

However, as-reported metrics do not seem to show how this company’s efforts to advance its products through sustainability positively affect its returns. Uniform Accounting shows that the business has a better Uniform return on assets (ROA) than what you might think.

Also, below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

According to the National Institute of Standards and Technology (NIST) of the U.S., businesses that embrace sustainable practices benefit through lower overhead costs, increased consumer base, and higher profitability.

With the benefits outweighing the costs, one might think that more companies would adopt strategies geared toward sustainability.

However, a McKinsey survey found that while more than 50% of business executives consider sustainability initiatives, only 30% of companies proactively invest in looking for sustainable business opportunities.

This lifestyle bag and travel luggage company continues to strengthen its commitment to sustainability through a global campaign it recently launched. It aims to continue delivering high quality products while reducing its environmental impact on the planet. Some of its well-known brands are Samsonite, Tumi, American Tourister, and Gregory.

To celebrate its 110th anniversary, Samsonite International S.A. launched its “Our Responsible Journey” global strategy as a sign of its commitment to lead the industry in sustainability. This campaign focuses on four areas: Innovative Products, Carbon Action, Thriving Supply Chain, and People Focused.

In recent years, Samsonite has translated sustainability in their product line by creating higher quality products while lowering environmental impact. Moreover, Samsonite has committed to create a positive impact in the communities in which it operates.

Looking into their products, Samsonite uses Recyclex™, a hardware material composed of 100% post-consumer recycled PET plastic bottles, for a number of their product lines. The company launched over 21 collections that contained Recyclex™ in 2018, saving more than 30 million 500ml PET bottles.

Furthermore, Samsonite upcycles its byproducts through transforming their plastic wastes into post-industrial regrind material. With this, Samsonite launched Samsonite’s S’Cure Eco range in 2018 in Europe, which enabled them to recycle more than 100 tons of high-quality plastic annually.

Through its sustainable efforts, Samsonite has been able to release over 50 sustainable collections that contain environmentally-friendly materials such as recycled PET, recycled nylon, post-industrial recycled polypropylene, wood waste, and cork.

Moreover, Samsonite introduced a new spin dyeing manufacturing process in their supply chain that eliminated water intensive processes and colored yarn during extrusion. Thanks to this, the firm was able to use 87% less water, 15% less energy, and 83% less chemicals.

Samsonite continues to put importance in investing in research and development for its sustainable innovations by procuring lighter and/or stronger new materials and promoting efficient product packaging. In addition, Samsonite is committed to completely using 100% renewable energy and to be carbon neutral by 2025.

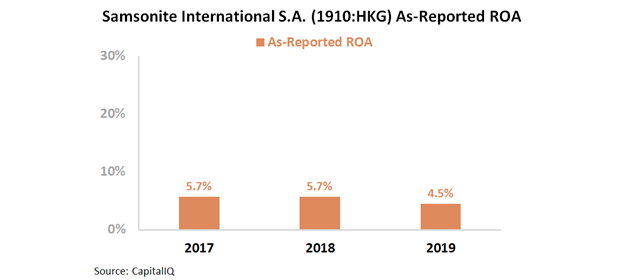

However, as-reported metrics don’t quite reflect these sustainability efforts. For the past three years, as-reported returns have been declining, from nearly 6% in 2017 to just 4.5% in 2019.

This is not an accurate representation of Samsonite’s profitability. The company’s real economic profitability is better reflected with Uniform Accounting adjustments, which shows that its TRUE earning power is actually stronger than what you think it is.

One of the things that as-reported metrics fail to consider is the amount of goodwill on Samsonite’s balance sheet, which is substantial given its many acquisitions in the past.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not showing the real strength of Samsonite’s earning power. After goodwill and other significant adjustments are made, the company actually had a 23% Uniform ROA in 2019, which is almost 5x stronger than its as-reported ROA of 5%.

Samsonite’s profitability is much better than you think it is

As-reported metrics are distorting the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

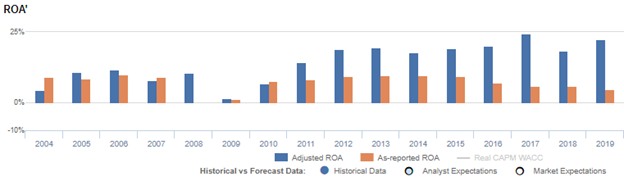

Samsonite’s Uniform ROA has actually been higher than its as-reported ROA in the past nine years. For example, as-reported ROA is 5% in 2019, significantly lower than its Uniform ROA of 23%. The company’s Uniform ROA for the past nine years has ranged from 14% to 24%, while as-reported ROA ranged only from 4% to 10% in the same time frame.

From 4% in 2004, Uniform ROA improved to 12% in 2006, before falling to its all-time low of 1% in 2009. Uniform ROA gradually recovered, peaking at 24% in 2017 before slightly declining to 23% in 2019.

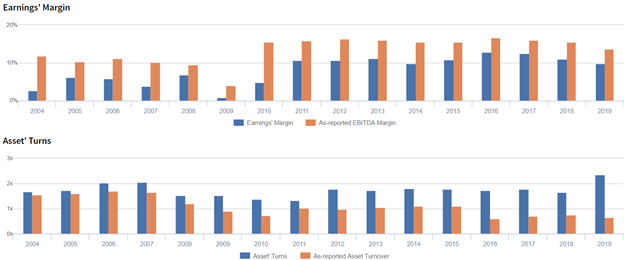

Samsonite’s Uniform earnings margins are weaker than you think but its robust Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in Uniform earnings margins and to a lesser extent, Uniform asset turns, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform earnings margins fell from 3% in 2004 to 1% in 2009, before rebounding to a peak of 14% in 2017. Uniform margins then settled to 10% in 2019.

Meanwhile, Uniform asset turns stayed in the range of 1.3x to 2.0x from 2004 to 2018, before reaching its peak of 2.3x in 2019.

SUMMARY and Samsonite International S.A. Tearsheet

As the Uniform Accounting tearsheet for Samsonite International S.A. (1910:HKG) highlights, the Uniform P/E trades at -5.3x, which is below the corporate average valuation levels and its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of Samsonite, the company has recently shown a 30% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Hong Kong Accounting Standards (HKAS) earnings and convert them to Uniform earnings forecasts. When we do this, Samsonite’s sell-side analyst-driven forecast is a 611% and 107% earnings shrinkage in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Samsonite’s HKD 8.22 stock price. These are often referred to as market embedded expectations.

Samsonite can have Uniform earnings shrink by 13% each year over the next three years and still justify current prices. What sell-side analysts expect for Samsonite’s earnings is far below what the current stock market valuation requires in 2020 and 2021.

The company’s earning power is 4x the corporate average. However, cash flows are below its total obligations—including debt maturities, capex maintenance, and dividends. This signals high credit and dividend risk.

To conclude, Samsonite’s Uniform earnings growth is below its peer averages in 2021, and the company is trading below its peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com