With prudent spending, this cement company has generated a concrete Uniform earning power of 22%.

Next to water, concrete has become the most used material in the world. Its sturdiness has made it an ideal material for the construction of any type of structure, from highways to skyscrapers.

This cement manufacturer has been one of the fastest growing in this space and it still has room to run, with its massive cash balance.

As-reported financials see their cash balance as a burden to the company, incorrectly dragging down the company’s TRUE profitability.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

With the rise of urbanization, particularly in developing countries, the global cement industry has enjoyed robust growth over the years. Since 2014, the industry has been expanding at 7% annually, and it is expected to grow by 10% each year until 2022.

The Philippines has also seen similarly rapid growth due to demand from both the public and private sectors.

With the current administration’s PHP 2.4 trillion “Build, Build, Build” program, local cement manufacturers had to reassure the Department of Trade and Industry (DTI) that they can match rising demand and that they will continue to expand capacity.

In the private sector, new construction was at robust levels last year. In Q4 2019, around 37,000 building permits were approved for construction.

However, the local cement industry has not been without its fair share of challenges. Its major headwinds include rising cement imports and quarantine-induced delays or suspension in construction activities.

Nevertheless, local manufacturers remain well-positioned for growth, particularly Eagle Cement Corporation (EAGLE:PHL). Eagle Cement is only the fourth largest cement manufacturer in the country, but it is one of the most profitable and fastest growing in terms of capacity.

As a response to the rise in cement imports from immaterial levels in 2014 to 14% of the Philippines’ annual cement supply by 2018, the DTI implemented cement tariffs in September 2019. The tariff was based on the conclusion of the Tariff Commission that cement imports posed an “imminent threat of serious injury” to the domestic cement industry.

The tariff limits the impact of industry headwinds and provides more room for growth for domestic producers. However, it may take a while for the local cement industry to feel its impact as construction companies will first need to reorganize their supply chain.

As for the more recent headwind, like other companies in the Materials sector, Eagle Cement’s business was hampered by the slowdown in construction activity. While the quarantine restrictions were only enacted in mid-March, it was enough to shrink Eagle Cement’s Q1 2020 revenues by 16% compared to Q1 2019.

As the restrictions are gradually lifted, Eagle Cement will likely see revenues partially recover, with construction activities slowly resuming again.

What makes Eagle Cement uniquely poised for growth is the company’s preference to build one mega factory in the center of high demand areas.

Its Bulacan Cement Plant is located between two regions with the highest construction activity, CALABARZON and NCR. Its factory is also the largest cement producing plant in the country, manufacturing 7.1 million metric tons of cement per year.

On the other hand, the rest of the competition have their plants spread out across the country. While the competition’s strategy may save on distribution costs, they do spend more on personnel costs and they face a harder time managing production efficiently.

Eagle Cement’s strategy is also why it has been very conservative in its cash. Since its IPO, the company’s cash balance has gone up from PHP 17 billion to PHP 18 billion, and their current facilities have been capable of satisfying most of their demand.

Though the company is currently building another plant in Cebu to reach the Visayas and Mindanao markets, it is only spending its average yearly cash flow.

However, as-reported metrics are incorrectly portraying the company as a less asset efficient business. In 2019, as-reported asset turnover was only 0.4x, significantly lower than Uniform asset turnover of 0.8x.

With asset turnover being a key driver of profitability, Eagle Cement’s bottom line is also understated. The company’s 2019 as-reported ROA was 9%, while Uniform ROA was actually more than double at 22%.

As-reported financials have distorted the market’s perception of the firm’s successful strategy and prudent spending.

Much of the distortion comes down to how excess cash is treated. While as-reported financials treat Eagle Cement’s entire cash balance as part of its asset base, Uniform Accounting removes the cash not necessary to operate and fulfill obligations–cash above what one might view as “operating” cash.

The purpose of removing excess cash is to see what the true operating ROA of the firm is. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

Since Eagle Cement has maintained a substantial cash balance each year, the company’s true asset base has been materially inflated each year.

In 2019 for example, Eagle Cement’s excess cash amounted to PHP 16 billion, a third of the company’s PHP 49 billion as-reported assets.

Removing excess cash, along with all the other necessary adjustments in Uniform Accounting, we arrive at a PHP 28 billion true asset base in 2019. This leads to a Uniform asset turnover of 0.8x and a Uniform ROA of 22%.

Eagle Cement’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

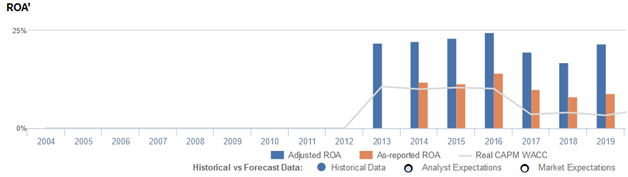

Eagle Cement’s Uniform ROA has actually been higher than its as-reported ROA in the past six years. For example, as-reported ROA was 9% in 2019, but its Uniform ROA was actually significantly higher at 22%. When Uniform ROA peaked at 25% in 2016, as-reported ROA was only at 14%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been much higher. Eagle Cement’s Uniform ROA for the past six years has ranged from 17% to 25%, while as-reported ROA ranged only from 8% to 14% in the same timeframe.

After improving from 22% in 2013 to a high of 25% in 2016, Uniform ROA declined to a low of 17% in 2018. Uniform ROA then recovered to 22% in 2019.

Eagle Cement is a more asset efficient business than you think

Eagle Cement’s profitability has been primarily driven by robust Uniform asset turns.

Since 2013, as-reported asset turnover has remained at 0.4x-0.5x levels through 2019. Meanwhile, Uniform asset turns sustained 0.6x-0.8x levels over the same time period.

As-reported metrics are making the firm appear to be a less efficient business than real economic metrics highlight.

SUMMARY and Eagle Cement Corporation Tearsheet

As the Uniform Accounting tearsheet for Eagle Cement highlights, the Uniform P/E trades at 8.3x, which is far below corporate average valuation levels and its own history.

Low P/Es require low EPS growth to sustain them. In the case of Eagle Cement, the company has recently shown a 34% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Eagle Cement’s sell-side analyst-driven forecast calls for an 8% Uniform EPS decline in 2020, followed by 11% Uniform EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Eagle Cement’s PHP 10 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 19% each year over the next three years and still justify current prices. What sell-side analysts expect for Eagle Cement’s earnings growth is above what the current stock market valuation requires.

The company’s earning power is 4x the long-run corporate average. In addition, cash flows are significantly higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Eagle Cement’s Uniform earnings growth is in line with peer averages in 2020, but the company is trading below peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com