With their strategic acquisitions, this tobacco company from Japan generated 19% Uniform returns that blew away as-reported returns of only 6%!

Republic Act 10351, or the Sin Tax Reform Law, was implemented in 2012 to restructure the excise tax on alcohol and tobacco products in the Philippines. Its purpose was to aid in financing the Universal Health Care program of the Philippine government.

Its implementation spurred a tobacco trade war locally, with Philip Morris International and PMFTC Inc. accusing Mighty Corporation of a number of issues, but none of which were formally resolved in court.

Mighty Corporation, the second largest cigarette manufacturer in the Philippines from 2010 to 2017, faced an even larger problem. They had allegedly been using counterfeit tax stamps on cigarette packs to avoid paying nearly PHP 40 billion in taxes.

Fortunately for Mighty, one of the largest cigarette manufacturers in the world was looking to expand its market share across Asia. Since Mighty already had a 23% market share in the Philippines, it looked like a perfect strategic acquisition.

In September 2017, this company acquired Mighty for PHP 46.8 billion, settling the PHP 30 billion in tax liabilities.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Tearsheet & Embedded Expectations

Powered by Valens Research

Tobacco is the common term for plants in the Nicotiana genus and the Solanaceae family. This term is also used for any product made from cured leaves of the tobacco plant.

Tobacco is one of the most widely used addictive substances worldwide. Tobacco smoking can be traced back to as early as 5000-3000 BC, when it was cultivated in Mesoamerica and South America.

It’s said that the practice of burning tobacco evolved from snuffing powdered tobacco. Burning tobacco was used in shamanistic rituals, and then later used for pleasure. Smoking tobacco was also used to establish contact with the spirit world.

Today, tobacco is its own global industry. One of the biggest industry players in the world is Japanese cigarette manufacturer Japan Tobacco Inc.

In 1898, the Japanese government established the nationalized tobacco monopoly run by a business that operated within their Ministry of Finance. The government’s total control meant it could easily collect taxes from tobacco leaf sales, which proved valuable when they needed to fund the Russo-Japanese War in 1904.

In 1949, the business became known as the Japan Tobacco and Salt Public Corporation (JTS) under the Allied Forces’ Occupation of Japan. It remained a state monopoly.

However, in 1985, the monopoly was abolished and Japan Tobacco Inc. (JT) was formed. Although technically it was a publicly traded stock company, the Japanese government only started selling its shares in October 1994. By March 2013, the Japanese government’s holdings finally reached the legal required ownership of at least a third of JT’s stock by March 2013.

In 1999, driven by the ambition to be a global company, JT expanded its brand portfolio and widened its reach to international markets through global acquisitions.

JT’s first acquisition was R.J. Reynolds’ tobacco holdings, which became known as JT International (JTI), an operating division of JT that handles the international production, marketing, and sales of their brands.

In 2007, they acquired Gallaher Group Inc. for about JPY 1.4 trillion. This integration, along with their other acquisitions in Asia, Africa, and Latin America, brought their workforce to over 40,000.

With their expansion, JT now had nine brands in their portfolio–Winston, Camel, LD, Mevius, Benson & Hedges, Glamour, Sobranie, Silk Cut, and Natural American Spirit. Each of them possessed a unique character and heritage.

Apart from their tobacco business, JT ventured into the pharmaceutical business. In 1986, they formed JT Pharmaceutical Co. Ltd., initially focusing on over-the-counter (OTC) cough remedies and nutritional supplement drinks.

JT operates in an industry heavily regulated by governments around the world. The push towards more explicit health warnings of the risk of cigarette smoking has long been one of JT’s challenges.

However, they acknowledge the necessity and importance of these regulations as it concerns health. The company supports regulations that comply with the Organization for Economic Co-operation and Development’s (OECD) principles.

They also have posters all around Japan, especially near train stations, designed to inform and educate people about smoking etiquette.

The company is also working on the development of new products. They aim to make tobacco products that do not use fire and do not emit smoke, hopefully reducing health risks created by smoking.

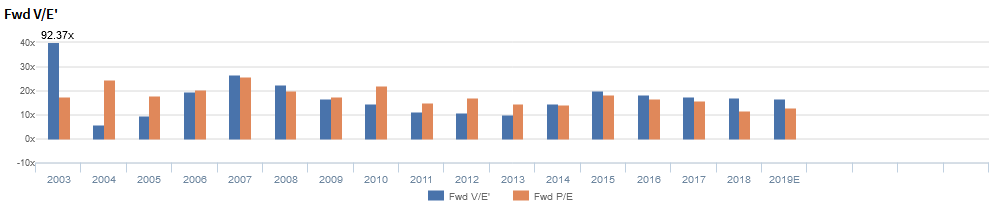

Japan Tobacco is more expensive than you think

Japan Tobacco Inc. (2914:JPN) currently trades around historical averages with a 16.5x Uniform P/E (blue bars), and is more expensive than as-reported P/E of 13.1x (orange bars).

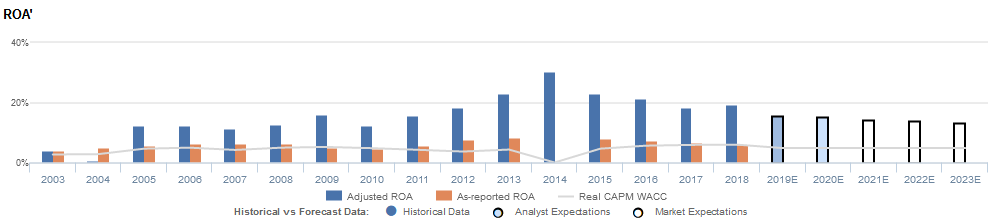

At these levels, the market is pricing in expectations for Uniform ROA to fall from 19% in 2018 to 14% in 2023, accompanied by immaterial asset shrinkage going forward.

However, analysts project Uniform ROA to remain at 15% in 2020, accompanied by a 2% Uniform asset shrinkage.

Japan Tobacco’s profitability is actually better than you think it is

Japan Tobacco’s profitability is cyclical, with Uniform ROA ranging from 1% to 31% over the past 16 years.

After falling to historical lows of 1% in 2004, Uniform ROA stabilized at 12% to 16% from 2005 to 2011, before rising to a peak of 31% in 2014. Afterward, it dropped to 23% in 2015, before slowly decreasing to 19% in 2018.

Meanwhile, Uniform asset growth was positive in nine of the past 16 years, while ranging from -13% to 20%.

As-reported metrics are understating Japan Tobacco’s profitability.

For example, as-reported ROA was 6% in 2018, a far cry from the Uniform ROA of 19%, making the company look like a weaker business than real economic metrics highlight.

Moreover, as-reported ROA has been below Uniform ROA for 15 of the past 16 years, significantly distorting the market’s perception of the firm’s historical profitability trends.

Japan Tobacco’s margins are lower than you think

Cyclicality in Uniform ROA has been driven primarily by trends in Uniform earnings margin, with peaks and troughs lining up historically with that of Uniform ROA.

After falling to 1% in 2004, Uniform earnings margin rose to 7% to 11% levels from 2005 to 2010, before rising to a peak of 23% in 2014. Thereafter, Uniform earnings margin fell to 20% in 2015, before stabilizing at 19% levels from 2016 to 2018.

Summary and Japan Tobacco Tearsheet

As the Uniform Accounting tearsheet for Japan Tobacco Inc. (2914:JPN) highlights, they are trading at 16.5x Uniform P/E, which is below market average valuations and around its historical average levels.

Low P/Es require low EPS growth to sustain them. In the case of Japan Tobacco, the company has recently shown a 1% growth in Uniform EPS.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Japan’s Modified International Standards (JMIS) earnings and convert them to Uniform earnings forecasts. When we do this, Japan Tobacco’s sell-side analyst-driven forecast is for Uniform earnings to shrink by 19% and 2% in 2019 and 2020, respectively.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify JPY 2,499 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels of Japan Tobacco, the company would have to have Uniform earnings shrink by 10% each year over the next three years.

What sell-side analysts expect for Japan Tobacco’s earnings growth falls well above what the current stock market valuation requires.

To conclude, Japan Tobacco’s Uniform earnings growth is below peer averages in 2020. Moreover, the company is trading below average peer valuations.

The company’s earning power, based on its Uniform return on assets calculation, is well corporate averages. Furthermore, with cash flows and cash on hand consistently exceeding obligations, Japan Tobacco has low credit and dividend risk.

About the Philippine Markets Daily

“Wednesday Uniform Earning Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com