You might think this Guinness world record holder for the largest noodles packet is serving a 13% return when it’s actually double that!

As quarantines remain in effect in many parts of the world, consumers continue to stock up on canned goods and other instant food.

This company’s instant noodles are distributed worldwide, specifically in Australia, Asia, Africa, New Zealand, United States, Canada, Europe, and in the Middle East. In the Philippines, this particular instant noodles have been served in 7-Eleven stores nationwide since 2018.

Today, we take a look at how as-reported metrics are distorting this company’s TRUE earning power.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

We’ve briefly discussed in our article on Nissin how instant noodles came to be over 60 years ago. We also talked about how Samyang instant noodles were South Korea’s answer to the food shortage problem post-WWII.

Though demand for instant noodles has spread throughout the world, the top consumers of this product remain in Asia. In fact, the world’s top five consumers are China, Indonesia, India, Japan, and Vietnam.

Given how rich and diverse Asia’s culinary scene is, manufacturers of instant noodles have created different flavors to suit the unique tastes of each country.

In Indonesia, one of the biggest players in the instant noodles market is Indomie, by PT Indofood CBP Sukses Makmur Tbk, the Consumer Branded Products (CBP) group under PT Indofood Sukses Makmur Tbk. Since the introduction of instant noodles in Indonesia during the late 1960s, it has remained a staple in the country until today.

Although Indomie launched its instant noodles brand in 1971, what put the brand on the map was its first dry noodles variant called the Indomie Mi Goreng. This instant noodles packet won the hearts of many, as it was inspired by the traditional Indonesian fried noodles dish.

Indomie became a household name for instant noodles to the point where the two have become interchangeable in the country. Aside from being just a snack, Indonesians have incorporated these instant noodles into their regular diet by consuming them for breakfast, lunch, or dinner.

Indofood CBP, the manufacturer of Indomie noodles, even holds the Guinness World Records title of largest packet of instant noodles, proving that one packet is already enough as a substantial meal.

Today, Indofood CBP is one of the world’s largest instant noodles manufacturers, with Indomie accounting for 72% of Indonesia’s instant noodles market share.

With 12.62 billion servings of noodles consumed in Indonesia in 2017 alone, this makes the country the second highest consumer in the world. Indomie instant noodles are available in over 80 countries around the world, with over 20 billion packs sold annually.

In 2016, Indomie ranked top 8 in The Brand Footprint Global Ranking Top 50 by Kantar Worldpanel and has consistently remained among the top 10 since then. Indomie is recognized alongside global powerhouses such as Coca Cola, Dove, Nescafe, and Pepsi.

Indomie continues to be a favorable brand because both its types of instant noodles, dry-based and soup based, have a variety of flavors to choose from. In order to stay ahead of its competitors, Indomie continuously innovates to meet the needs of its consumers.

After replicating the authentic Indonesian flavor, Indofood CBP launched a line called “Taste of Asia.” This includes flavors such as Thai Tom Yum, Korean Bulgogi, and Singaporean Laksa.

Considering the company’s offerings and its brand’s worldwide popularity, as-reported returns of 13% in 2019 is weaker than what it should really be.

Indofood CBP’s real economic profitability can be better reflected with Uniform Accounting adjustments, to show its TRUE earning power.

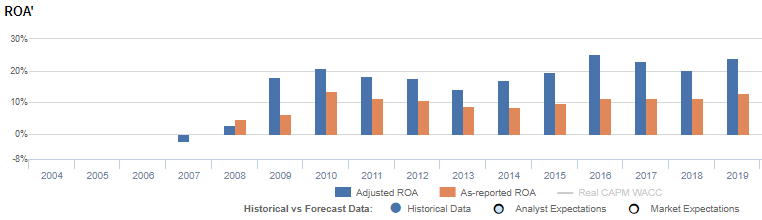

Looking at the company’s performance in 2016, Indofood CBP’s Uniform ROA peaked at 25%, which is more than double its as-reported ROA of 11%. This shows that the company’s earning power has been distorted by the inconsistencies in accounting standards.

What as-reported metrics fail to do is to consider excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

If excess cash remains included in the company’s asset base in computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is.

Over the past 10 years, Indofood CBP has had a significant amount of excess cash sitting idly in its balance sheet, ranging from 10% to 25% of its unadjusted total assets.

After excess cash and other significant adjustments are made, the company reported a 24% Uniform ROA in 2019, almost 2x stronger than their as-reported ROA of 13%.

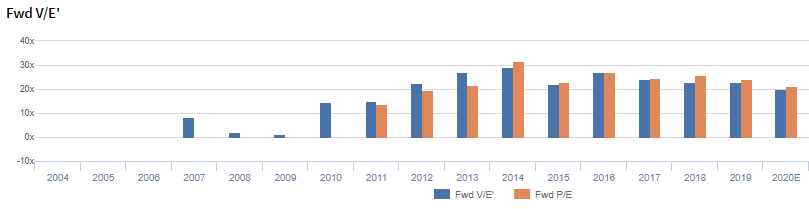

Indofood CBP’s valuations is in line with the market

PT Indofood CBP Sukses Makmur Tbk (ICBP:IDN) currently trades in line with corporate averages at a 19.9x Uniform P/E (blue bars), which is also in line with the as-reported P/E of 21.2x (orange bars).

At these levels, the market is pricing in expectations for Uniform ROA to fall to 20% in 2024, accompanied by 5% Uniform asset growth going forward.

However, analysts have more bullish expectations, projecting Uniform ROA to slightly increase to 25% in 2021, accompanied by 3% Uniform asset growth.

Indofood CBP’s profitability is much better than you think it is

As-reported metrics are distorting the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Indofood CBP’s Uniform ROA has actually been higher than its as-reported ROA in the past eleven years. For example, as-reported ROA was 13% in 2019, significantly lower than its Uniform ROA of 24%. When Uniform ROA peaked at 25% in 2016, as-reported ROA was just at 11%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been higher. Indofood CBP’s Uniform ROA for the past eleven years has ranged from 14% to 25%, while as-reported ROA ranged only from 6% to 14% in the same timeframe.

After rising from an all-time low of -2% in 2007 to 21% in 2010, Uniform ROA fell back to 14% in 2013. Afterwards, Uniform ROA recovered to reach a 25% peak in 2016 before sliding to 20% in 2018. Uniform ROA then increased to 24% in 2019.

Indofood CBP’s margins are weaker than you think, but it’s consistently stronger asset turnover makes up for it

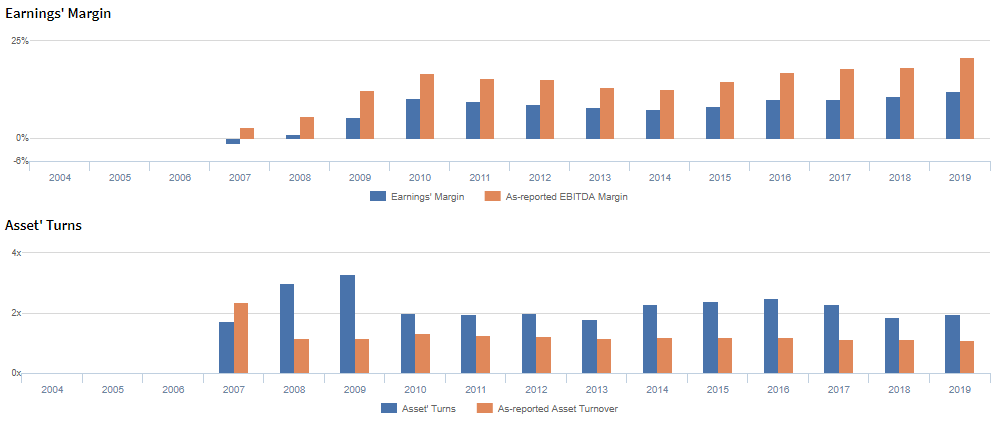

Cyclicality in Uniform ROA has been primarily driven mainly by both trends in Uniform asset turns and Uniform earnings margins, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform earnings margins increased from -1% in 2007 to 10% levels in 2010, before trending at 7%-8% levels in 2013 to 2015. It then gradually recovered to 12% in 2019.

Meanwhile, Uniform asset turns increased from 1.7x in 2007 to 3.3x in 2009 before trending at 1.8x to 2.0x levels in 2010 to 2013. It then recovered to 2.5x in 2016 but gradually fell to 1.9x in 2018, before expanding again to 2.0x in 2019.

Summary and Indofood CBP Tearsheet

As the Uniform Accounting tearsheet for Indofood CBP highlights, they are trading at a 19.9x Uniform P/E, which is around average market valuations but below its historical P/E of 22.4x.

Low P/Es require low EPS growth to sustain them. In the case of Indofood CBP, the company has recently shown a 20% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Indonesian Financial Accounting Standards (IFAS) earnings and convert them to Uniform earnings forecasts. When we do this, Indofood CBP’s sell-side analyst-driven forecast is for Uniform earnings to increase by 5% in 2020 and by 12% in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify IDR 9,875 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels of Indofood CBP, the company would have to have Uniform earnings shrink by 1% each year over the next three years. What sell-side analysts expect for Indofood CBP’s earnings growth is above what the current stock market valuation requires.

The company’s earning power, based on its Uniform return on assets calculation, is 4x corporate average returns. Furthermore, with cash flows and cash on hand consistently exceeding obligations, Indofood CBP has low credit and dividend risk.

To conclude, Indofood CBP’s Uniform earnings growth is in line with its peer averages in 2019 and it is also trading in line with peer average valuations.

About the Philippine Markets Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com