An air mattress in a living room gave birth to this multi-billion lodging company, with Uniform ROAs consistently at positive levels

Successful market disruptors don’t just offer a better product than their competitors—they completely change the landscape of the market and shift consumer behavior to their advantage.

This digital lodging marketplace has done exactly that, moving tourists and travelers across the globe away from traditional hotels and resorts and into more homey, private accommodations.

As-reported metrics signal that the disruption of the vacation properties market hasn’t translated to any profits for this company. Uniform Accounting, on the other hand, reveals the opposite.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

The world would have been a much different place if Ford hadn’t introduced the Model T car—the world’s first car that was made accessible to the masses.

The same can be said for Apple. If it hadn’t introduced the iPhone almost two decades ago, the landscape of technology would be very different now.

The iPhone was basically a mini computer in a pocket, combining the features of a phone, walkman, and of course, a computer. More importantly, it gave rise to the popularity of the smartphone.

All things considered, you can say that these companies are among the few of the greatest market disruptors of our time.

Being a market disruptor is no easy feat. However, across these industry standard-setters, there are two distinct characteristics that they always possess.

First, their products are deceptively simple—enough to make people go “why didn’t I think of that.” This makes it easier for the market to understand the value of a product, which leads to faster adoption rates.

Second, and arguably the most important characteristic, is that disruptive innovators change the way people behave. Netflix, for example, has completely changed the way we watch television, and has even led to the widespread cord-cutting trend.

Keeping these characteristics in mind, it’s clear that Airbnb (ABNB) is also one of these market disruptors.

The idea for Airbnb came when its founders, Brian Chesky and Joe Gebbia, started renting out an air mattress in their living room as a way to offset their rent. The company has since grown to become a $90 billion online marketplace offering peer-to-peer lodging services.

Airbnb’s business is simple: it provides a platform that connects renters to lodgers. The company then collects service and booking fees from both parties, which is how it makes its revenues.

Because the company doesn’t own the physical real estate itself, this makes the business extremely asset-light. What this means is that Airbnb doesn’t have to shell out massive amounts of capex to grow its assets.

Additionally, the company is also operating a fully digital channel. Unlike traditional hotels or travel agencies, Airbnb doesn’t have receptionists or booking agents—all reservations and bookings are made through the app or website, and guests do business with the hosts and not the company itself.

These features play into Airbnb’s greatest strength: scalability. The company has been able to globalize and penetrate new markets at a much lower cost and quicker pace relative to traditional hotels.

With over 2.9 million hosts worldwide (four times as much as the total number of hotels and resorts) across 100,000 cities, Airbnb has completely changed the vacation scene and how people approach their lodging needs.

A lot of tourists and travelers now prefer the homey feel and privacy of an Airbnb, especially among the younger generations.

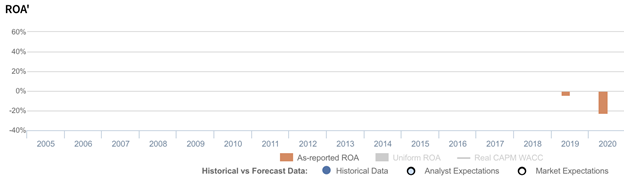

Looking at as-reported metrics, however, it seems that disrupting the vacation property market was not enough to generate profits for the firm, with as-reported return on assets that have fallen from -4% in 2019 to -23% in 2020.

In reality, Uniform Accounting shows that the simple idea of connecting travelers with property hosts translated not only to positive profits, but to improving ones as well. Over the same timeframe, Uniform ROAs are actually positive and have even doubled from 9% to 21%.

What as-reported metrics fail to do is to consider excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

The purpose of removing excess cash is to see what the true operating ROA of the firm is. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

In the case of Airbnb, the company had a substantial cash balance amounting to $3 billion, a little over one-third of its total assets. Having too much cash on the books inflates the asset base and causes profitability to look weaker than it really is.

Adjusting for excess cash, we can see that Airbnb is a positive-return business, with as-reported ROAs directionally misleading investors.

Airbnb’s earning power is significantly more robust than you think it is

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

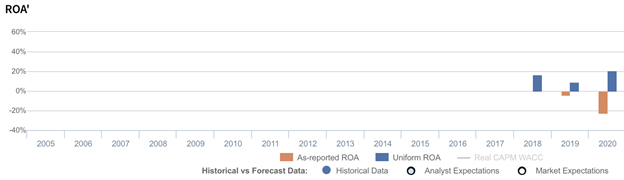

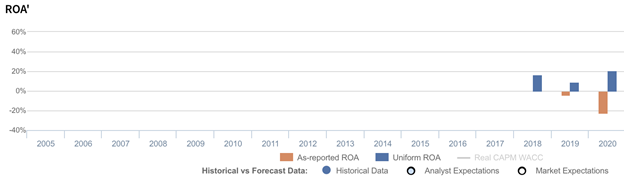

Airbnb’s Uniform ROA has actually been significantly higher than its as-reported ROA in the past three years. For example, Uniform ROA was at 21% in 2020 while as-reported ROA was at -23%.

Historically, Airbnb’s as-reported ROA has ranged from -23% to 0% in the past three years while Uniform ROA has ranged from 9% to 21% in the same timeframe.

After declining from 17% in 2018 to 9% in 2019, Uniform ROA rebounded to a high of 21% in 2020.

Airbnb’s Uniform earnings margin and Uniform asset turns are much stronger than as-reported

Overall improvements in profitability have been driven by trends in both Uniform earnings margin and Uniform asset turns.

Uniform margins fell from 14% in 2018 to 6% in 2019, before jumping to a peak of 19% in 2020. Meanwhile, after rising from 1.2x in 2018 to 1.6x in 2019, Uniform turns declined to 1.1x in 2020.

At current valuations, markets are pricing in expectations for both Uniform margins and Uniform turns to reach new peaks.

SUMMARY and Airbnb, Inc. Tearsheet

As the Uniform Accounting tearsheet for Airbnb, Inc. (ABNB:USA) highlights, the Uniform P/E trades at 32.4x, which is above the global corporate average of 23.7x and its own historical P/E of 19.0x.

High P/Es require high EPS growth to sustain them. In the case of Airbnb, the company has recently shown a 61% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Airbnb’s Wall Street analyst-driven forecast is a 468% and 28% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Airbnb’s $179 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 32% annually over the next three years. What Wall Street analysts expect for Airbnb’s earnings growth is well above what the current stock market valuation requires in 2021, but below that requirement in 2022.

Furthermore, the company’s earning power is 3x the long-run corporate average. Also, cash flows and cash on hand are over 4x its total obligations—including debt maturities and capex maintenance. Together, this signals a low credit risk.

To conclude, Airbnb’s Uniform earnings growth is in line with its peer averages. Therefore, as is warranted, the company is also trading around average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com