As-reported metrics are looking at this vintner and distiller company with an inebriated look. TRUE earnings margin is only 7%, not 12%

This gin producer is often overshadowed by its beer-making sister company. What many may not know is that the company now owns the best-selling gin brand in the world.

However, there may be good reasons for why it is overlooked. Although the company has many promising qualities, its low Uniform earnings margin makes these moot.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

According to the International Wine and Spirits Research (IWSR) group report in 2018, the Philippines is one of the fastest-growing alcoholic beverage markets in the world. Specifically, the Philippine gin market, which is the largest in the world, grew by 8% for the year.

IWSR predicts that a number of developing nations will be at the helm of the alcoholic beverage market’s growth within the next five years. When global alcoholic beverage consumption dipped by 2% in 2018, gin and whiskey actually grew in volume.

This expected growth means Ginebra San Miguel Inc. (GSMI:PHL), producer of the world’s largest selling gin, has a significant tailwind. The firm’s large brand portfolio makes it seem like it is able to capitalize on any advantages.

Ginebra San Miguel was founded in 1902 by Carlos Palanca, Sr. in Tondo Manila under the La Tondeña name, as inspired by its location. The company gained popularity when the American occupational government enacted food and beverage regulations to ensure the quality of the products. Only La Tondeña’s products were considered pure.

In the next 55 years, the company made three notable acquisitions to expand the distribution of its gin products throughout the entire country. It acquired Ayala Distillery from Ayala y Compañía in 1924, Añejo Rhum from Tabacalera in 1955, and the trademark rights to Kulafu in 1957.

In 1987, San Miguel Corporation bought the company from the Palanca family, then renamed La Tondeña to La Tondeña Distillers after the transaction. La Tondeña benefited from San Miguel Corporation’s vast domestic and international distribution network.

La Tondeña Distillers changed its name to Ginebra San Miguel only in 2003 as an homage to the gin brand and its heritage. To keep up with changing consumer behavior patterns, new gin variants were introduced like GSM Blue for entry-level drinkers and Ginebra San Miguel Premium Gin for the upscale market.

Aside from growing its gin brand, Ginebra San Miguel expanded its liquor portfolio to include Gran Matador Solera Brandy (2003); Tondeña Premium Rum (2004); Gran Matador Solera Gran Reserva (2005); Antonov Vodka, Don Enrique Mixkila, and St. George’s Whiskey (2006).

All of the acquisitions and developments Ginebra San Miguel did led to its prominence in the Philippine liquor market. In fact, by controlling the Philippine gin market—the largest in the world—so well, it became the largest gin producer in the world.

However, while industry tailwinds, a huge portfolio, and global market dominance are all attributes any firm would like to have, these are irrelevant if a company is unable to translate these to the bottom line.

As-reported metrics think that Ginebra San Miguel is capable of doing just that with its robust margins. Excluding 2011, as-reported EBITDA margin has been positive in each year since 2004 and has even reached as high as 26%.

That said, Ginebra San Miguel’s true earnings margins show that it has been weaker at generating earnings from its vast revenue base. Uniform earnings margin has actually been negative in five of the past sixteen years and has only ever peaked at 14%.

With Ginebra San Miguel’s margins lower than initially thought, its favorable position may no longer be as appealing.

One reason behind the distortion in the as-reported figures comes from the accounting treatment of depreciation expense of fixed assets.

Depreciation expense is a non-cash expense, meaning it does not represent an actual outlay of cash. Also, it can be easily manipulated by changing the asset’s life. As such, depreciation expense should be removed from earnings.

However, the company does spend cash on maintenance capital expenditures to ready the same assets for use in the following years. That said, this expense barely shows up in its entirety on the balance sheet.

To arrive at an estimate of the firm’s maintenance capex, what is done instead is smoothing as-reported depreciation expense over a few years, adjusting for inflation and asset impairments.

Removing PHP 167 million of maintenance capex from Genebra San Miguel’s 2019 earnings along with the many other adjustments made leads to just 7% Uniform earnings margin 2019, lower than as-reported earnings margin of 12%.

Ginebra San Miguel’s earning power is slightly weaker than you think

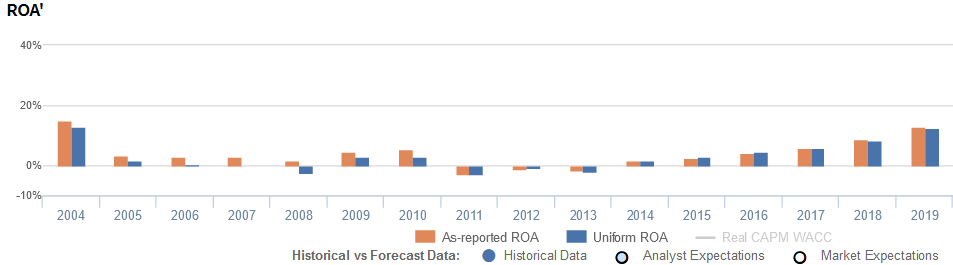

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that Ginebra San Miguel’s profitability has been stronger than real economic metrics have highlighted in each of the past sixteen years.

In reality, Ginebra San Miguel’s true profitability has been slightly lower than its as-reported ROA. Specifically, as-reported ROA was 13% in 2019, but Uniform ROA was only at 12%.

As-reported ROA dropped from 15% in 2004 to 2% in 2008, before recovering to 5% in 2010. Thereafter, as-reported ROA declined to negative levels from 2011-2013, before rising to 13% in 2019.

Meanwhile, after falling from 13% in 2004 to -2% in 2008, Uniform ROA rebounded to 3% levels in 2009-2010. Then, Uniform ROA contracted to -3% in 2011, before improving to 12% in 2019.

Ginebra San Miguel’s margins are weaker than you think

Weakness in Uniform ROA has been driven by weak Uniform earnings margins. In fact, Uniform margins have been lower than as-reported EBITDA margins in each of the past sixteen years.

As-reported EBITDA margins steadily declined from a peak of 26% in 2004 to -3% in 2008, before slowly recovering to 12% in 2019.

Meanwhile, after contracting from 14% in 2004 to -4% in 2008, Uniform margins improved to 3% levels in 2009-2010 and subsequently fell to -5% in 2011. Since then, Uniform margins have rebounded to only 7% in 2019.

Looking at the firm’s margins alone, the as-reported metrics are making the firm appear to be a more cost-efficient business than is accurate.

SUMMARY and Ginebra San Miguel Inc., Incorporated Tearsheet

As the Uniform Accounting tearsheet for Ginebra San Miguel (GSMI:PHL) highlights, the Uniform P/E trades at 9.4x, which is below corporate averages but around its own history.

Low P/Es require low EPS growth to sustain them. However, in the case of Ginebra San Miguel, the company has recently shown a 66% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Ginebra San Miguel’s sell-side analyst-driven forecast calls for a 2% Uniform EPS decline in 2020 and immaterial EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Ginebra San Miguel’s PHP 51.70 stock price. These are often referred to as market embedded expectations.

The company can have its Uniform earnings decline by 16% each year over the next three years and still justify current valuations. What sell-side analysts expect for Ginebra San Miguel’s earnings growth is above what the current stock market valuation requires in 2020 and in 2021.

Furthermore, the company’s earning power is 2x long-run corporate averages, and cash flows and cash on hand are 269% of its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Ginebra San Miguel’s Uniform earnings growth is in line with peer averages, and the company is trading below peer average valuations.

About the Philippine Markets Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com