As-reported metrics aren’t seeing this company with a sober look. TRUE earning power is twice its 5% as-reported ROA.

While Filipinos are a beer-loving people, their consumption of liquor has equally grown.

According to Euromonitor International, the Philippines spent $3 billion on distilled spirits in 2018, enough to rank in the top 25 globally. In 2023, the country is expected to become the 22nd largest consumer of liquor.

This Philippine company is capitalizing on its local success as a springboard to the global stage.

Today, most Philippine cities have implemented liquor ban sales as part of the government’s community quarantine policies.

While as-reported metrics imply that the company is struggling to succeed, TRUE UAFRS-based (Uniform) analysis shows healthy earnings.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Out of all the industries that exist today, the alcoholic beverage industry is probably one of the most interesting.

Many Filipinos would attest to this, though probably for a different reason.

For investors and entrepreneurs, it’s a huge and fragmented industry. One company has yet to dominate the $1.7 trillion global market.

The industry is often classified into four groups: Beer, Spirits, Wine, and Others.

However, within each of these mentioned groups, there are countless types of drinks with an almost infinite number of variations. The source of the ingredients and the process of making a beverage brings a unique taste and texture to each one.

This is why there hasn’t been a drink considered as a universal favorite, because there’s always another drink that can match one’s taste better.

We’ve seen this happen in the Philippines. Before the late 20th century, everyone thought that the market was set and that there were only two major liquors that Filipinos wanted: gin (distilled sugarcane) and rum (distilled molasses).

As such, a duopoly occurred. Ginebra San Miguel Inc. (GSMI:PHL) provided the gin while Tanduay Distillers, Inc. supplied the rum.

Yet in 1990, a new competitor arrived on the scene.

After sharpening his business acumen from running the McDonald’s franchise in the Philippines, Andrew Tan created Emperador Inc. (EMP:PHL) to break into the liquor business and offer another type of distilled beverage: brandy.

Made from wine, Emperador brandy distinctly differed in taste from its sugarcane counterparts and offered a more premium variant of liquor.

Emperador distinguished itself from the competition by advertising their brandy as a gentleman’s drink. Their endorsers dressed up in suits, in contrast to the burly and macho men seen in Ginebra and Tanduay commercials.

Disrupting the near 100-year old duopoly, Emperador quickly saw success in the Philippines, becoming the market leader in the liquor business by the early 2010s.

However, Emperador’s reign was short-lived. Early on, Ginebra and Tanduay learned that to survive, they had to expand production to other types of liquor.

Since 2001, Tanduay had been trying to tap into the brandy market and in 2013, they finally launched Compañero brandy. They also have been producing their own line of vodka and whisky.

Meanwhile, Ginebra launched their own brandy product in 2015 called Primera Light. Since then, they have also expanded to the vodka and rum market.

Today, market share is more or less divided equally among the three, still, Emperador generates almost as much revenue as the other two combined.

While Ginebra and Tanduay were too focused on regaining lost market share, the people at Emperador were asking themselves this question: “Why fight over the $3 billion Philippine liquor market when it is just dimes and pennies compared to the $1.7 trillion global market?”

As such in 2014, Emperador ventured into the whisky business and acquired one of the largest scotch markers in the world, Whyte & Mackay, for PHP 31 billion.

In 2016, Emperador acquired Beam Suntory’s brandy and sherry business in Spain for PHP 13.8 billion. As part of the deal, the company would own the production of “Fundador” brandy, which would soon become the company’s best selling premium product and the best brandy in the world.

In the same year, the company sought access to the Latin American market, taking over the Domecq brandies and wines from Pernod Ricard (RI:FRA).

With these deals, Emperador became the world’s largest brandy company, controlling a significant niche in the global market.

Although the market is seeing a negative impact from COVID-19 due to weak demand amid store closures and liquor bans, the company is still one of the few stocks that continue to appreciate. Year-to-date, Emperador stock price has appreciated by 11%.

Part of this stock improvement comes from their operations not halting. Unlike other food and drink products, Emperador’s products do not undergo spoilage if not sold today. In fact, their alcoholic beverages can even become more valuable if kept in the barrel longer.

So while they’re delaying the production of their liquors, they’ve temporarily switched to a different type of alcohol. During the early days of the enhanced community quarantine, Emperador announced mass production of one million liters of 70% disinfecting alcohol to be donated to the front-liners.

Still, the market may not be wholly convinced with the firm’s resiliency during this period. One reason why Emperador stock price continues to increase is due to the speculation that the firm would be taken private as its free float is now down to 13%.

However, recent as-reported financials show less profitability than what Uniform metrics reveal, understating the company’s TRUE earning power by more than half, providing negative value for shareholders since.

In 2018, as-reported metrics showed only a 5% ROA, but when we remove the accounting distortions, Emperador’s Uniform earning power is actually higher at 11%.

One of the main contributing factors is how Philippine Financial Reporting Standards (PFRS) accounts for intangible assets.

Based on PFRS, intangible assets made of trademarks are fixed assets. While this asset is important to the company’s operations, in reality these assets do not represent the company’s actual operational performance. Hence, in Uniform Accounting, intangible assets are removed from total assets.

As an example, in 2018, Emperador recognized an intangible asset of PHP 20.51 billion or 18% of the company’s total assets of PHP 117.82 billion. When we remove PHP 20.51 billion from total assets since it’s not an operating asset, total assets decrease and, along with the many other adjustments Valens makes, we arrive at a TRUE earning power of 11%.

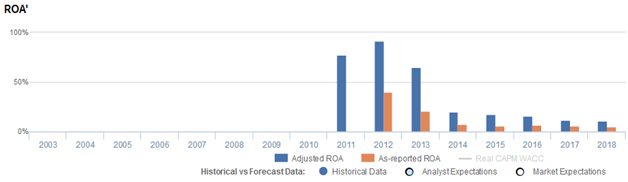

Emperador’s earning power is stronger than you think

As-reported metrics are significantly understating Emperador’s (EMP:PHL) profitability.

Historically, Emperador’s profitability has been declining since their IPO, following a series of aforementioned acquisitions. Although the trend in Uniform return on assets (ROA) (blue bars) is similar to as-reported ROA (orange bars), it is nowhere near the lows that traditional metrics report.

As an example, from a peak of 65% in 2013, Uniform ROA has fallen every year until it reached 11% levels. Meanwhile, as-reported ROA fell from 21% to current 5% levels in the same timeframe.

Using as-reported numbers, the company appears to be much weaker than real economic metrics highlight.

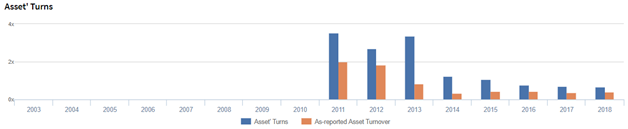

Emperador’s asset turns are stronger than you think

Trends in Uniform earning power have been driven by declines in Uniform asset turns and, until more recently, Uniform earnings margins.

Emperador’s Uniform asset turns have trended downwards, but not to the degree that as-reported metrics state. The company is generating better sales per peso spent in assets than what traditional metrics imply.

After ranging from 2.7x-3.5x in 2011-2013, Uniform turns have fallen to current 0.7x levels. Similarly, as-reported asset turns peaked at 2.0x in 2011, before dropping to 0.4x levels in 2017-2018.

Every year, Uniform asset turns have been understated, significantly distorting the market’s perception of the firm’s asset efficiency level.

SUMMARY and Emperador Inc. Tearsheet

As our Uniform Accounting tearsheet for Emperador highlights, Uniform P/E trades at 22.4x, which is around market average but above the company’s historical average levels.

Average P/Es require average EPS growth to sustain them. In the case of Emperador, the company has recently shown 6% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Emperador’s sell-side analyst-driven forecast is for Uniform earnings to grow 10% in 2019, before shrinking 12% in 2020.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify PHP 8.00 per share. These are often referred to as market embedded expectations.

To meet the current market valuation levels of Emperador, the company would need to grow its Uniform earnings by 1% each year over the next three years.

What sell-side analysts expect for Emperador’s earnings growth is near what the current stock market valuation requires.

The company’s earning power is 2x the corporate average and the company has low dividend risk, signaling that their cash flow risk to the company’s operations and credit profile in the future is low.

To conclude, Emperador’s Uniform earnings growth is below peer averages, while the company is trading slightly above peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com