As-reported metrics claim this company generated profits in the global financial crisis, but its TRUE earning power was actually negative, not 8%.

While pessimism over the entire market may be unwarranted, it is worthwhile to review how companies individually perform during economic downturns.

On an as-reported basis, this mining company seems to have been doing well during the global financial crisis in 2007-2009 but Uniform (UAFRS-based) metrics reveal that the firm actually hit rock bottom.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

People often mention the oil crises when they talk about the 1970s. Oil prices tripling in 1974 and doubling again in 1979 caused such a shock to the world economy that each event sparked a global recession.

In an effort to mitigate the volatility during that period, the Philippine government enacted policies to reduce the economy’s dependence on oil.

One of these policies was the nationwide excavation of coal, including the exploration of Semirara island, located near the Philippines’ geographic center.

Semirara island is too small to be noticed but actually contains one of the largest known coal reserves in the country.

In 1980, the government gave exclusive mining rights of Semirara island to a company named after the island itself, Semirara Coal Corporation (SCC:PHL).

The company struggled in its early years, due to high start-up costs associated with opening a mine. It went public in 1983, in order to amass the needed capital and scale faster.

Semirara eventually overcame its scaling troubles and is now responsible for over 90% of the country’s coal production. From 1.5 million metric tons (MMT) of coal per year in 2001, the company is now producing at a rate of 15 MMT per year in 2019.

However, for investors, a mining company’s value as a stock largely depends on the amount of deposits it can still mine. Despite a company’s high production rate, the market can have a negative perception of the business if reserves are near depletion.

Fortunately, this is not yet an issue for Semirara. There is a site on the island called the Himalian mine, which the company has yet to excavate and is said to possess 120 MMT of coal.

The island also contains large deposits of silica, limestone, and clay that the company can tap into for additional revenue.

The company has since expanded into the power generation business, acquiring a coal power plant in 2009 to ensure constant demand for its coal. To reflect this change, the company modified its name to Semirara Mining and Power Corporation.

All in all, its strong performance, a stable future, and a secondary line of business point to strong fundamentals for Semirara.

True enough, in 2019, as-reported return on assets (ROA) was 10%, close to Uniform earning power of 12%.

While Uniform Accounting has been showing higher profitability for Semirara, that has not always been the case.

When the 2007-2009 global financial crisis occurred, as-reported ROA was displaying 8%-11%, near current levels. On the other hand, Uniform earning power was already at a meager 2% in 2007, before fading to 1% in 2008 and falling further to negative levels in 2009.

Looking at 2009 specifically, what as-reported financials got wrong in this instance was the depreciation of the company’s fixed assets.

Since depreciation doesn’t represent an actual outlay of cash, Semirara’s PHP 1.1 billion depreciation expense should be added back to its earnings.

The company does spend cash on maintenance capital expenditures though, to ready the same assets for use in the following years. However, this expense barely shows up in the balance sheet.

To arrive at an estimate of the firm’s maintenance capex, what is done instead is smoothing as-reported depreciation expense over a few years, adjusting for inflation and “asset impairments”, and factoring in the 2009 power plant acquisition.

In this manner, the firm should actually be recognizing PHP 3.7 billion of maintenance capex, more than thrice as much according to Uniform Accounting.

As a result, along with the many other adjustments made, we arrive at a PHP 738 million loss in Adjusted earnings and a -3% Uniform earning power for Semirara in 2009.

Semirara’s earning power is stronger than you think

Despite trending similarly in the recent years, as-reported metrics continue to distort the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Coming out of the global financial crisis, Uniform ROA has actually been higher than as-reported ROA for over nine of the past ten years. For example, in 2017, Uniform ROA reached a peak of 28%, almost 2x higher than as-reported ROA of 15%.

Through Uniform Accounting, we see that the firm’s true ROAs have actually been more volatile as well. Since 2004, Uniform ROA had gradually fallen from 17% in 2004 to negative levels in 2009.

Thereafter, Uniform ROA recovered to 15%-20% levels in 2010-2013, before compressing to 2% levels in 2014 due to low oil prices. Then, Uniform ROA expanded to a peak of 28% in 2017 and subsequently faded to 12% in 2019.

Meanwhile, as-reported ROA declined from a 35% high in 2004 to 8% in 2006. Since then, as-reported ROA has stabilized at 8%-13% levels through 2019, excluding 15% in 2017.

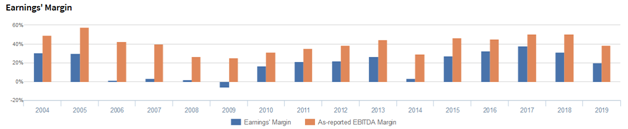

Semirara’s earnings margin is more volatile than you think

Volatility in Uniform ROA has largely been driven by volatility in Uniform earnings margin. Uniform margins ranged from 30%-31% in 2004-2005, before regressing to negative territory in 2009.

Then, Uniform margins recovered to a high of 27% in 2013, before fading to 4% in 2014. After jumping to a peak of 38% in 2017, Uniform margins have since faded to 20% in 2019.

Every year, as-reported earnings margin has been overstated, making the company’s earnings appear stronger than real economic metrics highlight. This suggests that strength in Uniform ROA has been driven by the firm’s asset efficiency.

SUMMARY and Semirara Mining and Power Corporation Tearsheet

As the Uniform Accounting tearsheet for Semirara highlights, Uniform P/E trades at 7.4x, which is far below market average levels and the company’s historical average levels.

Low P/Es require low EPS growth to sustain them. In the case of Semirara, the company has recently shown a 37% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Semirara’s sell-side analyst-driven forecast is to see 1% Uniform earnings shrinkage in 2020, followed by 17% Uniform earnings growth in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify PHP 11.82 per share. These are often referred to as market embedded expectations.

To meet the current market valuation levels of Semirara, the company would need to shrink Uniform earnings by 19% per year over the next three years.

What sell-side analysts expect for Semirara’s earnings growth is above the current stock market valuation required in 2020.

The company’s earning power is 2x the corporate average, and the company has low dividend risk, with cash flows and cash on hand consistently exceeding debt obligations.

To conclude, Semirara’s Uniform earnings growth is above peer averages in 2020, and the company is trading below peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com