As-reported metrics conveniently leave out how efficient and profitable this company really is, especially as a leader in the franchising business

From lotto outlets to fast-food restaurants, the Philippine franchising market has seen an explosion over the recent years. At the forefront of this trend is the world’s largest franchise in terms of number of stores.

With its rapid store expansion in the country, as-reported metrics are showing profitability become more muted. Meanwhile, Uniform Accounting shows that this company’s earning power is ramping up as well.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

In 2018, the Philippine Franchise Association (PFA) reported that the Philippine franchising industry rose 14% from $22 billion in sales to $25 billion. On top of this solid growth, sales grew higher the following year by 20%.

The industry has experienced a massive boom. What was once 5% of Philippine GDP in 2015 now contributes 7% of GDP as of 2019. The increasing disposable incomes of Filipinos and the rise in jobs across the country have been serving as tailwinds.

Furthermore, many businesses from various fields have chosen to employ a franchising model. Gyms, milk tea stores, gas stations, and coffee shops are some of the many examples of franchises.

From the franchisor’s side, franchising is attractive because it reduces risk and costs in expanding the business, particularly the need to take on debt and operate the store. The franchisee becomes responsible for getting the business up and running.

For the franchisees, franchising is desirable because it is less risky, with the business already having a recognizable brand name. The business immediately has a core customer base it can serve, at the expense of paying the franchisor fees and a piece of the profits.

Leading this franchising trend are the convenience stores. In cities across the Philippines, convenience stores are found on almost every street, as we previously mentioned in our FamilyMart article.

This time, we’ll talk about 7-Eleven, the largest among the convenience store franchises, with 2,864 branches in the country as of 2019.

Given their relatively small size, convenience stores are cheaper to fund and easier to fit into an available commercial space. Total cash outlay for a 7-Eleven franchise usually ranges from PHP 3.5 million to PHP 5 million, while typical fast-food restaurants can vary from PHP 15 million up to PHP 35 million.

It is no wonder then that 7-Eleven, under the management of Philippine Seven Corporation (SEVN:PHL), has been expanding faster than the rest of its peers. In 2019 alone, the company was able to open 349 stores nationwide.

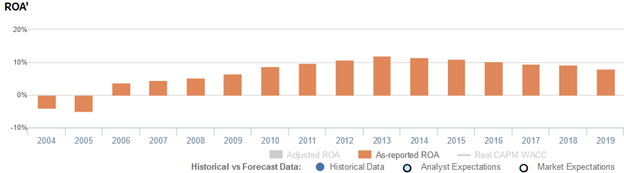

When looking at the as-reported metrics, the rapid expansion of 7-Eleven stores appears to be an unfruitful strategy for the firm. Since 2013, as-reported ROAs have eroded each year from 13% to just 8%.

The chart above implies that the company hasn’t been able to take advantage of the supposedly more efficient franchise model, with its asset base growing at a much faster pace than the earnings it is able to generate.

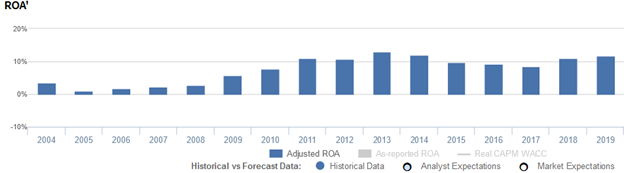

In reality, the opposite story is actually the case. The company has been seeing its true earnings ramp alongside its asset base. After fading from 13% in 2013 to 9% in 2017, Philippine Seven’s true earning power has been on a rebound, improving to 12% by 2019.

What as-reported metrics fail to consider is how current liabilities are factored into the ROA calculation. Traditional ROA calculations for measuring a firm’s earning power only include current and long-term assets as part of the cost of investment.

However, a company’s ability to receive goods and services in advance of payments – the current operating liabilities – ought to be factored in as well.

Current liabilities (excluding short-term debt) are necessary for operations. Items such as accounts payable, accrued expenses, and others are used to maintain the firm’s current capital position. On the other hand, long-term liabilities are mostly just used to finance the business.

If a company has a ton of cash to service its current liabilities and we only factor in its cash, it would make the company look inefficient. In reality, the company is just being responsible by building liquid assets to meet short-term obligations.

As such, net working capital (current assets – current liabilities) is used for the firm’s ROA calculation. This shows a company’s real cash management ability and thereby, its true earning power.

In the case of Philippine Seven, as-reported metrics’ asset base for ROA calculation is at PHP 29.7 billion in 2019, leading to an 8% as-reported ROA.

However, when subtracting current operating liabilities and applying other needed adjustments, we arrive at Philippine Seven’s PHP 18.5 billion Uniform assets, resulting in a 12% Uniform ROA.

Philippine Seven’s recent earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight in the past two years.

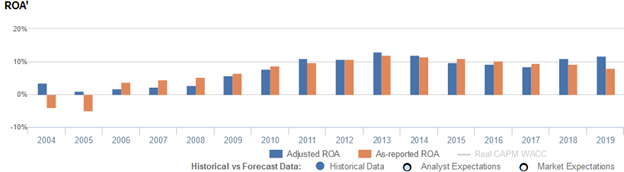

Philippine Seven’s true profitability has been understated over recent years. In 2019, as-reported ROA was 8% in 2019, but Uniform ROA was actually higher at 12%.

As-reported ROA inflected positively from negative levels in 2004-2005 to 2% in 2006-2007, before steadily expanding to 12% peaks in 2013-2014 and subsequently fading to 8% in 2019.

Meanwhile, after declining from 4% in 2004 to 1% in 2005, Uniform ROA slowly rebounded to a high of 13% in 2013. Thereafter, Uniform ROA compressed to 9% in 2016-2017, before recovering to 12% in 2019.

Philippine Seven’s recent turns are stronger than you think

Trends in Uniform ROA have been driven primarily by trends in Uniform asset turns. As-reported metrics have similarly understated the firm’s recent asset utilization.

As-reported asset turnover rose from 2.1x in 2004 to 2.7x-2.8x levels in 2005-2007, before contracting to 2.5x in 2009 and rebounding to a high of 2.9x in 2012. Then, as-reported asset turnover maintained 2.5x-2.7x levels through 2018, before dropping to a low of 1.8x in 2019.

Meanwhile, after fading from 2.1x in 2004-2005 to 1.9x in 2007, Uniform turns expanded to a peak of 2.9x in 2013. Thereafter, Uniform turns declined to 2.2x in 2017, before recovering back to 2.9x in 2019.

Looking at the firm’s asset utilization for the past year, as-reported metrics are making the firm appear to be a more asset inefficient business than is accurate.

SUMMARY and Philippine Seven Corporation Tearsheet

As the Uniform Accounting tearsheet for Philippine Seven (SEVN:PHL) highlights, the Uniform P/E trades at 52.4x, which is well above corporate average valuation but around its own history.

High P/Es requires high EPS growth to sustain them. However, in the case of Philippine Seven, the company has recently shown a 31% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Philippine Seven’s sell-side analyst-driven forecast calls for a 19% and 5% Uniform EPS decline in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Philippine Seven’s PHP 112.00 stock price. These are often referred to as market embedded expectations.

The company needs its EPS to grow by 15% each year over the next three years to justify current valuations. What sell-side analysts expect for Philippine Seven’s earnings growth is well below what the current stock market valuation requires in 2020 and 2021.

That said, the company’s earning power is 2x the long-run corporate average and intrinsic credit risk is only 70bps above the risk-free rate. Together, this signals low credit and dividend risk.

To conclude, Philippine Seven’s Uniform earnings growth is well below peer averages in 2020, but the company is trading well above its peer average valuations as well.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com