Below cost-of-capital returns suggests this company needs to study the best method to gain economic value

Between 2005-2014, both public and private universities in the Philippines recorded a steady rise of local and international enrollees. However, K-12, along with rising competition and inflation, and increasing online learning offerings halted some of the schools’ success.

This company deals with these challenges by increasing its marketing efforts while also expanding its network in different locations.

Although the company has seen declining profitability in recent years, it’s not as weak as what as-reported metrics suggest.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Education in the Philippines has been largely influenced by the systems of Spain and the United States.

In the Spanish era, the aim of the colonizers was to put up parochial schools and teach Christianity. Besides religion, they also taught Filipinos how to read, write, and make art.

The Americans’ goal, on the other hand, was focused on training the Filipinos on self-government. They also made it a point to teach them their core language—English.

Since then, so many changes have been made to the system. Today, the formal education system in the country spans at least 14 years, consisting of a primary, secondary, and tertiary education. It is also divided into two types: public and private.

As of 2018, about 12% of the higher education institutions (HEIs) in the Philippines are public, while the rest of the 88% are private HEIs, with more enrollments coming from the private sector.

In addition to that, the Philippines has the most number of HEIs in the Southeast Asian region. Due to this, there is stiff competition among educational services companies to get more enrollments.

One company trying to dominate this field is STI Education Systems Holdings, Inc. (STI:PHL).

As the owner of one of the largest networks of private schools in the Philippines, STI competes with other schools by offering a wide selection of degree programs through its subsidiary, STI Education Services Group (STI ESG).

STI ESG programs include information and communications technology, business and management, hospitality management, and many more. It also offers vocational programs, post-graduate, and associate programs.

Besides focusing on its different programs, STI has been boosting its marketing efforts by spending on advertisements and promoting its educational institutions, resulting in its general and administrative costs ranging from 50%-60% of total revenue in 2008-2012.

Over the years, STI has been expanding its academic centers in different cities, funded through the issuance of fixed-rate bonds. The company now has a total of 77 campuses nationwide.

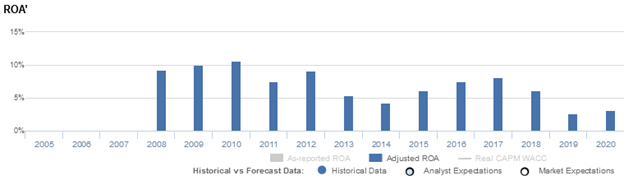

With the company’s focus on its expansion efforts to drive enrollment, STI was able to enjoy above cost-of-capital returns, ranging from 8%-11% in 2008-2012.

However, with the implementation of the K-12 program in 2013, wherein two years were added into secondary education, the company saw fewer student enrollments for the next two years.

STI ESG was able to turn that around by offering senior high school (SHS) in its program.

Additionally, STI acquired West Negros University Corporation in 2013, which is now known as STI WNU. This transaction provided a way for STI to widen its course offerings and access to basic education in preparation for the K-12 program, eventually delivering a 29% increase in STI WNU student population by 2015.

STI further expanded its operations by acquiring iAcademy in 2016, which specializes in animation, multimedia arts and design, and software engineering. The company invested in equipping iAcademy’s buildings with computer suites and high-speed internet. As a result, iAcademy became the first college in the ASEAN region to be appointed as an IBM Center of Excellence.

Although these acquisitions helped the company partially recover its profitability from 2015-2017, factors such as higher advertising and promotion expenses for tertiary programs, inflation, and the growth of online learning offerings during 2018-2019 continue to pose problems for STI.

Moreover, because of the coronavirus pandemic, STI had to close 12 schools to lessen its rental costs amid the low enrollment since the beginning of the academic year 2020.

Despite being able to reduce its costs in 2020, the impact of the pandemic has kept improvements in Uniform ROA to only 3% levels.

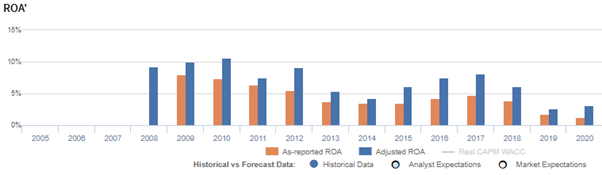

However, as-reported metrics suggest that the company’s collapse is much more severe, with as-reported ROA falling from 5% in 2017 to just 1% in 2020.

The growing deviation of as-reported metrics from the company’s true performance stems from the treatment of how Philippine Financial Reporting Standards (PFRS) classifies interest expense.

According to PFRS, interest expense is an operating cash flow. In reality, interest expense represents the cost of debt and is rightfully a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

For example, in 2020, STI Education recorded an interest expense of PHP 340 million. When we add the PHP 340 million back to earnings, net income increases because it is not an operating expense.

By making this adjustment, along with the many other necessary adjustments Valens makes, we can see that STI actually earned PHP 440.6 million net income during the year, and not incurred a loss of PHP 136 million. This adjustment drives a Uniform ROA of 3% in 2020, higher than as-reported ROA of just 1%.

Cross-comparison against peers also becomes possible since the performance, expectations, and valuations of companies are now evaluated irrespective of the amount of leverage.

STI’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think STI’s profitability has been weaker than real economic metrics have highlighted in the past twelve years.

In reality, STI’s true profitability has generally been higher than its as-reported ROA since 2009. Specifically, Uniform ROA was at 3% in 2020, while as-reported ROA was only 1% that year.

As-reported ROA compressed from 8% in 2009 to 4% in 2014, before recovering to 5% in 2017 and declining to a low of 1% in 2020.

Meanwhile, after expanding from 9% in 2008 to a peak of 11% in 2010, Uniform ROA declined to 4% in 2014. Then, Uniform ROA improved to 8% in 2017 before declining to 3% levels in 2019-2020.

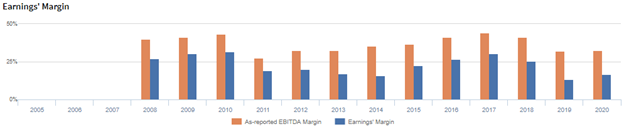

STI’s earnings margin is weaker than you think

Trends in Uniform ROA have been primarily driven by trends in Uniform earnings margin.

After improving from 40% in 2008 to 43% in 2010, as-reported margins decreased to 28% in 2011. Then, as-reported margins increased to a peak of 44% in 2017 before fading to 33% in 2020.

Meanwhile, Uniform margins expanded from 27% in 2008 to 32% in 2010, before compressing to 16% in 2014 and rebounding to 31% in 2017. Since then, Uniform margins decreased to 17% in 2020.

Looking at the firm’s margins alone, as-reported data makes the firm appear to be a more cost efficient business than real economic metrics highlight.

SUMMARY and STI Education Systems Holdings, Inc. Tearsheet

As the Uniform Accounting tearsheet for STI Education Systems Holdings, Inc. (STI:PHL) highlights, it trades at a Uniform P/E of 80.5x, well above the global corporate average of 23.7x and its historical average of -34.3x.

High P/Es require high EPS growth to sustain them. In the case of STI, the company has recently shown a 19% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, STI’s sell-side analyst-driven forecast calls for a 270% EPS decline in 2021 followed by a 24% EPS growth in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify STI’s PHP 0.37 stock price. These are often referred to as market embedded expectations.

STI is currently being valued as if Uniform earnings were to shrink by 2% annually over the next three years. What sell-side analysts expect for the company’s earnings growth is below what the current stock market valuation requires in 2021, but above its requirement in 2022.

STI’s earning power is below the long-run corporate average. Furthermore, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Also, intrinsic credit risk is 1,575bps above the risk free rate. Together, this signals a high dividend and credit risk.

To conclude, STI’s Uniform earnings growth is below peer averages in 2020. However, the company is trading above its average peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com