Betting most of its chips on its casino business allowed this company to cash in Uniform ROAs of 15%+ pre-pandemic

While the gambling industry has been around for centuries, integrated resorts (IRs) were only first introduced through the development of Resorts World Manila in 2009.

Like Belle Corporation (BEL:PHL), today’s company also focused on its casino and gaming business by developing one of the leading integrated casino resorts in the bay area. Despite this advantage, as-reported metrics suggest weak returns.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

In 2019, casino gaming in the Philippines grew much faster than in any of the well-known gambling markets like Las Vegas and Macau.

A slower growth rate was expected for the USD 2.7 billion Las Vegas market at the time, but Macau’s gambling market actually experienced a 0.5% decline in gross gaming revenue for the first quarter of 2019.

The recent growth opportunities in this space led to the development of integrated resorts (IRs), which helped further bring tourism and increased revenues in the Philippines.

As we’ve discussed previously, Manila’s “Entertainment City,” a vast stretch of land in the city’s bay area, houses four of the biggest integrated resorts in the country—namely Resorts World, Okada, City of Dreams, and Solaire.

Having these resorts at close proximity to each other meant they did not have to worry about how to get clients from different cities to visit their casinos. With all the resorts in one place, it was easier to drive foot traffic from one casino to another.

Last time, we talked about Belle Corporation, the owner and developer of City of Dreams. Today, we are going to talk about one of its competitors, Bloomberry Resorts Corporation (BLOOM:PHL).

Bloomberry’s business primarily revolves around casino and gaming through the development of its flagship business—Solaire Resorts and Casino—in 2010.

In March 2013, Bloomberry opened Solaire’s services to the public and garnered around PHP 11.5 billion in gaming revenues that year.

Then, in 2014, the firm spent PHP 14 billion for its Sky Tower project and added 66 gaming tables and 312 suites to accommodate its VIP customers.

With these expansions, Bloomberry proceeded to double its gaming revenues to PHP 22.8 billion in 2014, which eventually improved to PHP 38.5 billion in 2019 and garnered a CAGR of 18.8% since its opening year.

On top of that, strategically putting its resort in the blooming Entertainment City, along with the continued expansion of its gaming facilities, has also helped the company attract its massive clientele.

However, due to the pandemic, travel restrictions caused suspensions of all non-essential services, including gaming operations.

As a result, Bloomberry’s gaming revenues plunged to PHP 14 billion while net income dropped to PHP 8.3 billion for the year 2020.

In addition, the target completion date of the second Solaire casino in Quezon City, a 40-story integrated resort, has been pushed back to 2023 from the initial target of 2022.

As such, investors are still skittish to pour their money into the casino and gaming industry. While the recent challenges would make it seem that the company had fallen off a cliff, looking at its past performance, Bloomberry has been successful in handling its business.

Taking its outlier 2020 performance off the picture, one would think that Bloomberry’s focus on developing its business by opening Solaire Resorts and Casino has historically helped the company become one of the largest casino operators in the country.

However, as-reported metrics make it seem like the company had struggled to achieve returns above 8%, with returns on assets (ROAs) only ranging from 0%-8% in 2014-2019.

In reality, Bloomberry’s focus on improving and expanding its casino business has actually produced better returns for the company.

One of the said distortions stems from how Philippine Financial Reporting Standards (PFRS) classifies interest expense.

According to PFRS, interest expense can be classified as an operating cash flow. In reality, interest expense represents the cost of debt and is rightfully only a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

Specifically, in 2019, the company recorded a PHP 5.6 billion interest cost. Adding back this expense because it is not an operating expense, along with many other necessary adjustments made by Valens, leads to a PHP 13.4 billion net income and 15% Uniform ROA, higher than PHP 9.6 billion as-reported net income and 8% as-reported ROA.

Bloomberry’s earning power is stronger than you think in most years

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that Bloomberry’s profitability is weaker than what real economic metrics highlight in most years.

In reality, Bloomberry’s true profitability has generally been higher than its as-reported ROA except in 2020.

As-reported ROA expanded from negative levels in 2011-2013 to 8% in 2014, before fading to immaterial levels in 2015. Thereafter, as-reported ROA recovered to 7%-8% levels in 2017-2019, before falling back to negative levels in 2020.

Meanwhile, after improving from negative levels in 2011-2013 to 10% in 2014, Uniform ROA compressed to 3% in 2015 before rising to a peak of 16% in 2017. Then, Uniform ROA contracted to 11% in 2018 before rebounding to 15% in 2019. Since then, Uniform ROA declined to negative levels in 2020.

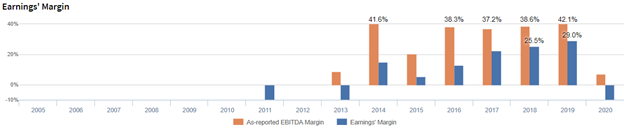

Bloomberry’s earnings margin is trending differently than you think

Volatility in Uniform ROA has been driven by trends in Uniform earnings margin, where Bloomberry is substantially improving as they continue to attract high-margin VIP customers.

Ignoring outlier shrinkage in 2011, Uniform margins inflected positively from negative levels in 2013 to 15% in 2014. Then, Uniform margins contracted to 5% in 2015 before rebounding to historical highs of 29% in 2019. Thereafter, Uniform margins fell again to negative levels in 2020.

Looking at the firm’s margins alone, as-reported metrics make the firm appear to be a more cost-efficient business than is accurate.

SUMMARY and Bloomberry Resorts Corporation Tearsheet

As the Uniform Accounting tearsheet for Bloomberry Resorts Corporation (BLOOM:PHL) highlights, it trades at a Uniform P/E of 17.7x, below the global corporate average of 23.7x but around its historical average of 19.3x.

Low P/Es require low EPS growth to sustain them. In the case of Bloomberry, the company has recently shown a 206% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Bloomberry’s sell-side analyst-driven forecast calls for a 105% EPS decline for 2021 and a 1,077% EPS growth for 2022.

Furthermore, the company’s earning power is below the long-run corporate average, and cash flows and cash on hand are slightly above total obligations—including debt maturities, capex maintenance, and dividends. Also, intrinsic credit risk is 450bps above the risk free rate. Together, this signals a low dividend and moderate credit risk.

To conclude, Bloomberry’s Uniform earnings growth is in line with peers, but currently trades below average peer valuations.

About the Philippine Markets Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com