Bringing businesses online has always been this company’s domain, earning it returns as high as 390%

Thanks to advancements in technology, it has become much easier to set up a business in the largest marketplace there is: the Internet. To do that, entrepreneurs have to establish an online presence with a website, and this company helps them do exactly that.

This company’s main revenue source is in domain names registration. But to set up an online business properly, security, marketing, and other business applications are necessary. Most entrepreneurs avail of these services on top of the domains, and is where the company sources its revenues as well.

Looking at as-reported metrics, it seems that this company’s business has been less than stellar, with as-reported return on assets (ROAs) peaking at 3%. In reality, Uniform ROAs have gone up to 390%, showing just how profitable its one-stop solution is.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

From 1990 to 2014, the number of entrepreneurship courses offered have increased from 180 to more than 2,000 in the U.S. alone. Another study conducted by OnePoll also showed increasing interest in entrepreneurship among American millennials, with 30% already with a side business and 72% showing interest in starting one.

Whether it be in the number of startups, venture capital investors, or new businesses opened in the past few years, the rise of entrepreneurship is something undeniable—this is partly thanks to advancements in technology.

There are now several resources available online for people to learn more about entrepreneurship. One can also easily set up an online business in a few days through online marketplaces such as Amazon or eBay.

Some people even choose to create their own websites themselves, which is exactly the market GoDaddy (GDDY:USA) provides solutions for.

GoDaddy’s core business is in domain names registration, which is an integral starting point when setting up a website. The company also has additional services such as domain privacy, backorder handling, and even brokerage services through auctions or direct offers for domains that have already been taken.

The domains business generates about half of GoDaddy’s revenues. Demand for it is high, especially since domains are relatively cheap, costing as low as $2. However, the average customer spends much more than that because they purchase additional features and services that they need—this is where GoDaddy generates the other half of its revenues.

These additional services include web hosting, marketing, and business applications.

For web hosting services, this is categorized into three tiers: shared, virtual private server, and dedicated.

Shared servers are a great entry point for users who want to set a presence online but aren’t expecting web traffic by the millions. It’s also affordable given that the server costs are split among the users sharing the space.

Virtual private servers and dedicated servers, on the other hand, are for users who are expecting heavy web traffic, such as corporations, and who want additional features such as higher server bandwidth and business applications compatibility.

GoDaddy also offers a suite of marketing tools to help its users expand their presence online. This includes Search Engine Optimization features, scheduling tools, integration with major payment apps, and social media management services.

Finally, the company’s business application products enable users to make use of third-party applications for their operations, as well as other in-house developed services that offer targeted email campaigns and messaging capabilities through text messages and social media sites.

GoDaddy has been able to offer an expansive suite of products and services thanks to its in-house capabilities, as well as through its many strategic acquisitions. Some of these include Mad Mimi (email marketing service), Canary (smart calendar app), Sucuri (security services), and Poynt (point-of-sale systems and online payment features).

All in all, GoDaddy’s core domains business and its other offerings enabled it to pull in over 20 million customers, with more than 80 million unique domain names being serviced across 14 offices around the world. The company also boasts a 92% retention rate for customers who stay at least three years.

Looking at as-reported metrics, it seems that GoDaddy has been a less-than-stellar business with as-reported return on assets (ROAs) that are almost immaterial, ranging only from -1% to 3%.

In reality, GoDaddy is a massively profitable business thanks to the demand for its domain products, as well as its outstanding cross-selling capabilities, with Uniform ROAs that have ranged from 60% to 70% recently and that have even gone up to highs of 390% historically.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on GoDaddy’s balance sheet. In recent years, goodwill sits close to $3 billion, about half of its total assets, stemming from the company’s acquisitions to expand its products and services.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of GoDaddy’s earning power. Adjusting for goodwill, we can see that the company isn’t actually performing poorly. In fact, it has been the complete opposite, with returns that are 30x to even nearly 400x greater.

GoDaddy is actually significantly more profitable than you think it is

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

GoDaddy’s Uniform ROA has actually been significantly higher than its as-reported ROA in five of the past six years. For example, as-reported ROA was 3% in 2020, but its Uniform ROA was actually more than 40x higher at 130%.

Specifically, GoDaddy’s Uniform ROA has ranged from -319% to 392% in the past six years, while as-reported ROA maintained -1% to 3% levels in the same timeframe.

Uniform ROA rebounded from negative levels in 2015 to a peak of 392% in 2017, before falling to 66% in 2019 and climbing to 130% in 2020.

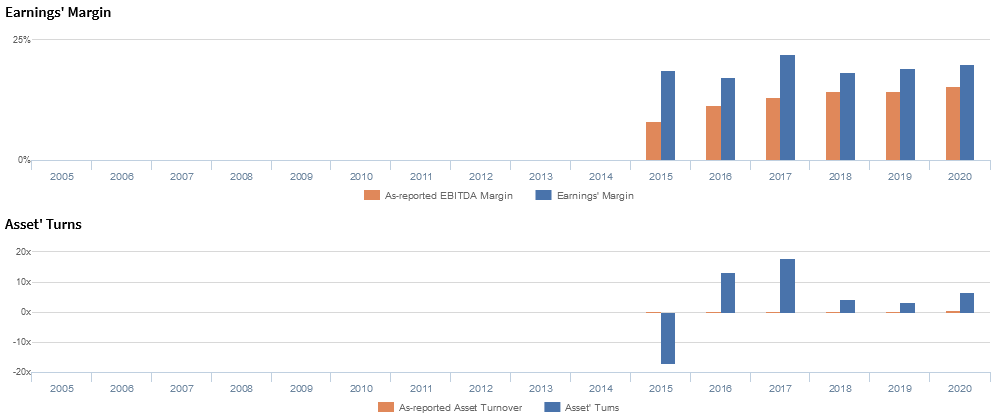

GoDaddy’s Uniform earnings margins and Uniform asset turns are more robust than you think

Volatility in Uniform ROA has been driven by volatility in Uniform asset turns, slightly offset by stable Uniform earnings margin.

After improving from negative levels in 2015 to a high of 17.8x in 2017, Uniform turns fell to 3.4x in 2019 and improved to 6.5x in 2020. Meanwhile, Uniform margins have sustained 17%-22% levels since 2015.

At current valuations, markets are pricing in expectations for Uniform margins to remain stable, coupled with a continued compression in Uniform turns.

SUMMARY and GoDaddy Inc. Tearsheet

As the Uniform Accounting tearsheet for GoDaddy Inc. (GDDY:USA) highlights, the Uniform P/E trades at 24.4x, which is around the global corporate average of 25.2x and its historical Uniform P/E of 23.5x.

Moderate P/Es require moderate EPS growth to sustain them. In the case of GoDaddy, the company has recently shown a 29% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, GoDaddy’s Wall Street analyst-driven forecast is a 12% and 13% EPS growth in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify GoDaddy’s $87 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 3% annually over the next three years. What Wall Street analysts expect for GoDaddy’s earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is 22x the corporate average. Also, cash flows and cash on hand are over 1.6x higher than its total obligations—including debt maturities and capex maintenance. Together, this signals a moderate credit risk.

To conclude, GoDaddy’s Uniform earnings growth is in line with its peer averages, and the company is trading above its average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com