Building the foundation for the future of wireless technology has rewarded this infrastructure company with above cost-of-capital Uniform returns

Cellular network providers are enabling the connectivity to 5G, but equally as important are the ones constructing the cell towers themselves, like this infrastructure construction company. 5G tailwinds have pushed this company higher, but even before then, it has been benefitting from the rollout of previous wireless technology upgrades such as 3G and 4G.

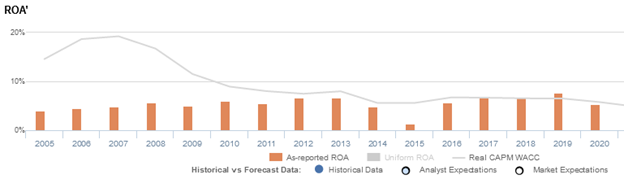

Even so, as-reported metrics only see this company as a below cost-of-capital business. Uniform Accounting, however, paints a different picture. Thanks to breakthroughs in wireless technology, this company was able to provide shareholders with excess value, with above cost-of-capital Uniform ROAs ranging from 6%-13%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

It’s truly remarkable just how far technology has evolved over the past century.

In the 1950s, disk drives that could only store a couple megabytes of data used to be the size of a closet. Now, we have hard drives that can store up to 100 terabytes of data—that’s about 100 million times more data than in the 50s—and it all fits in the palm of our hand.

That’s just the growth of physical storage—the cloud can store even more than that. Currently, the cloud is storing millions of terabytes worth of data, and it will continue to expand indefinitely thanks to another tech megatrend: 5G.

As the name suggests, 5G is the fifth generation of wireless technology. Earlier versions focused on voice and messaging capabilities, while more recent versions focused on internet connectivity and data transfer speeds.

5G is akin to its more recent predecessors, but a lot faster and robust—it’s essentially the technology that’s powering the biggest tech megatrends we currently have.

This includes, as mentioned, the cloud, as well as virtual reality and augmented reality, autonomous (self-driving) vehicles, and the Internet of Things (IoT).

The creation of Smart Cities powered by artificial intelligence and the digitalization of industries such as healthcare, agriculture, and manufacturing, among others, will markedly progress faster thanks to 5G connectivity.

At the forefront of this breakthrough technology are telecommunication companies who are providing 5G connectivity through its cellular towers. But equally as important are the ones building the towers, the very foundation for 5G itself.

This is where MasTec, Inc. (MTZ:USA) comes in.

MasTec is an industrial construction company other companies hire to build their infrastructure. It has existing relationships with some of the country’s top telecommunication providers, including AT&T and Verizon.

The deployment of 5G requires a large capital expenditure investment from these telecom companies, which provides an opportunity for MasTec to generate stable revenues over the buildout period.

Even before the rollout of 5G, however, as a reputable infrastructure construction company, MasTec has been one of the go-to operators for services ranging from engineering to installation to maintenance.

So, while 5G tailwinds are fueling the company’s current cash flows, as well as cash flows over the next few years, the rollout of previous wireless, high-speed connections such as 3G and 4G have contributed largely to MasTec’s revenues over the last decade.

On an as-reported basis, it seems as though MasTec is barely a cost-of-capital firm, with return on assets (ROAs) ranging only from 1%-8%.

In reality, Uniform Accounting reveals that the company has been able to provide excess shareholder value above its cost of capital, with Uniform ROAs ranging from 6%-13%. This is partly thanks to the tailwinds from the breakthroughs in wireless technology.

The distortion comes from as-reported metrics failing to consider the number of operating leases MasTec has arising from the numerous equipment and supplies it uses for its telecom projects, as well as other projects in its other segments.

The decision management makes between investing in capex and investing in a lease is based on how management wants to finance their investments. Choosing to lease an asset, however, would not be treated as an investment, but as an expense that would impact the income statement.

Specifically, operating leases on MasTec’s income statement are understating the company’s true earnings. Adjusting for the rent expense distortion, which historically has been about half of total operating expenses, returns are actually stronger.

As a result, as-reported ROAs are not capturing the strength of MasTec’s earning power. Adjusting for operating leases, we can see that the company isn’t actually performing poorly, with Uniform ROAs above cost-of-capital levels.

MasTec’s earning power is actually more robust than you think it is

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

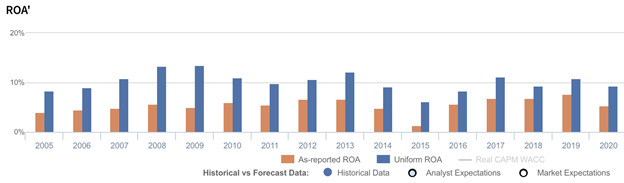

MasTec’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, Uniform ROA was at 9% in 2020, while as-reported ROA was only at 5%, which is below cost-of-capital levels.

Specifically, MasTec’s Uniform ROA has ranged from 6%-13% in the past sixteen years, while as-reported ROA ranged from only 1%-8% in the same timeframe.

Uniform ROA expanded from 8% in 2005 to peak 13% levels in 2008-2009, before compressing to 10% in 2011 and rebounding to 12% in 2013. Subsequently, Uniform ROA dropped to 6% in 2015, as the firm faced headwinds in its Oil and Gas segment, and recovered to 11% in 2019, driven by a recovery in this market and growth in its communication business. Uniform ROA has since faded to 9% in 2020 owing to pandemic headwinds.

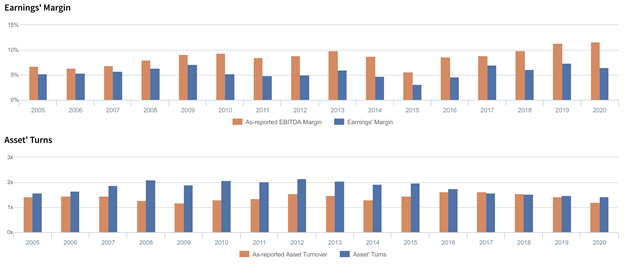

MasTec’s Uniform earnings margin is weaker than you think, but its Uniform asset turns make up for it

Trends in Uniform ROA have been driven by trends in Uniform earnings margin, and to a lesser extent, Uniform asset turns.

Uniform margins improved from 5% in 2005 to a peak of 7% in 2009, before compressing to 5% in 2011 and recovering to 6% in 2013. Then, Uniform margins compressed to 3% in 2015 and expanded to 7% in 2017. It has since remained at 6%-7% levels through 2020.

Meanwhile, Uniform turns expanded from 1.6x in 2005 to a peak of 2.2x in 2012. However, since then, Uniform turns have gradually declined to a low of 1.4x in 2020.

At current valuations, the market is pricing in expectations for slight improvements in Uniform margins and Uniform turns.

SUMMARY and MasTec, Inc. Tearsheet

As the Uniform Accounting tearsheet for MasTec, Inc (MTZ:USA) highlights, the Uniform P/E trades at 26.3x, which is above the global corporate average of 23.7x and its historical Uniform P/E of 19.7x.

High P/Es require high EPS growth to sustain them. In the case of MasTec, the company has recently shown a 19% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, MasTec’s Wall Street analyst-driven forecast is a 10% and 15% EPS growth in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify MasTec’s $116 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 1% annually over the next three years. What Wall Street analysts expect for MasTec’s earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is 2x the corporate average. Also, cash flows and cash on hand are 1.7x higher than its total obligations—including debt maturities and capex maintenance. However, intrinsic credit risk is 260bps above the risk-free rate. Together, this signals a moderate credit risk.

To conclude, MasTec’s Uniform earnings growth is in line with its peer averages, and the company is trading above its average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com