Built differently: this developer managed to sustain its strong profitability even amid the pandemic, recording a Uniform ROA of 27%

While Philippine real estate companies took a hit during the pandemic, this company was an exemption to the rule thanks to a completely different market it serves and its cost-effective strategy.

However, its as-reported data show its profitability did not improve even as the economy started reopening.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

The Philippine Tobacco Flue-Curing and Redrying Corporation was incorporated in 1951 as a tobacco business.

Through the years, the company would diversify its operations and eventually form a new subsidiary called the Baesa Redevelopment Corporation (BRC). This subsidiary redeveloped and leased its parent company’s old warehouses.

Because of the success of BRC’s operations as well as the declining export volumes and domestic prices of tobacco products, the parent company eventually phased out its tobacco business and focused more on its leasing business.

In 2014, the company renamed itself as the PTFC Redevelopment Corporation (TFC:PHL) with the primary business repositioning as a real estate corporation.

Today, PTFC Redevelopment Corporation deals and engages in acquiring an interest in land or real estate development in the Philippines.

Majority of the company’s clients are walk-in clients who were referred in from other tenants and brokers. Its main competition comes from complexes and warehouses within a rough radius of three to five kilometers from Balintawak, Quezon City.

However, PTFC Redevelopment Corporation’s competitive edge is said to be from its ample parking, technologically advanced gate access, and securely monitored compounds via CCTV.

During the height of strict quarantine restrictions in 2020, occupancy rates declined, but so did its cost of services. The lower consumption of power from its facilities helped gross income increase by 30% in 2020.

Then, the company implemented early retirement packages for its employees in order to mitigate the risks associated with the pandemic. Because of this, PTFC Redevelopment Corporation would have lower general and administrative expenses in 2021, which helped with the declining occupancy rates.

Although its gross income would decrease by 5% in 2021, the rental business continued to provide a sustainable source of income and cash flow for the company.

Going forward, management has expressed that no external event or trend will materially affect its operations, excluding the impact of strict quarantine restrictions in 2020.

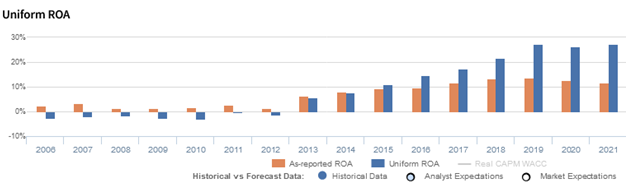

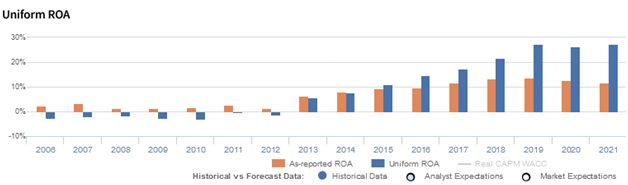

Looking at its as-reported metrics, it seems that lower occupancy rates have affected profitability, with ROAs fading to 12% in 2021.

In reality, the company’s strategy to focus on its warehouse rental business continues to drive profitability, with Uniform ROAs achieving a high of 27%.

What as-reported metrics fail to do is to consider the company’s excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

When excess cash remains included in the company’s asset base in computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

For 2021, PTFC Redevelopment Corporation had a significant amount of excess cash sitting idly in its balance sheet for up to 54% of its as-reported total assets.

PTFC Redevelopment Corporation’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that PTFC Redevelopment Corporation’s profitability has been weaker than real economic metrics highlight.

Through Uniform Accounting, we can see that the company’s true ROAs have been mostly understated over the past seven years. For example, as-reported ROA was 12% in 2021, but its Uniform ROA was actually higher at 27%.

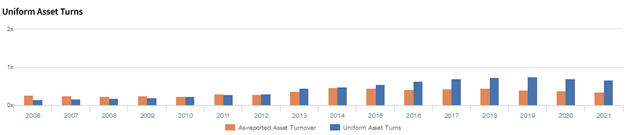

PTFC Redevelopment Corporation’s asset turns are more efficient than you think

Trends in Uniform ROA have been driven by trends in Uniform asset turns. Since 2016, as-reported metrics have understated PTFC Redevelopment Corporation’s asset efficiency, a key driver of profitability.

Moreover, as-reported asset turnover has maintained 0.7x peaks since 2017. In comparison, Uniform turns have yet to exceed 0.5x over the same time period, making PTFC Redevelopment Corporation appear to be a less efficient business than real economic metrics highlight.

SUMMARY and PTFC Redevelopment Corporation Tearsheet

As our Uniform Accounting tearsheet for PTFC Redevelopment Corporation (TFC:PHL) highlights, the company trades at a Uniform P/E of 9.8x, below the global corporate average of 19.3x and its historical P/E of 14.7x.

Low P/Es require low EPS growth to sustain them. In the case of PTFC Redevelopment Corporation, the company has recently shown a 5% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, PTFC Redevelopment Corporation’s sell-side analyst-driven forecast is to see a Uniform earnings decline of 2% in 2022 and immaterial growth in 2023.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify PTFC Redevelopment Corporation’s PHP 43.20 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 14% annually over the next three years. What sell-side analysts expect for PTFC Redevelopment Corporation’s earnings growth is above what the current stock market valuation requires through 2023.

Furthermore, the company’s earning power is 5x the long-run corporate average. Also, cash flows and cash on hand are nearly 7x above total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

Lastly, PTFC Redevelopment Corporation’s Uniform earnings growth is in line with its peer averages, and is also trading in line with its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com