Can this remote communications giant zoom past the pandemic bubble and sustain an 84% earnings growth going forward?

Staying at home will be the new normal routine as flattening the curve continues to be the country’s top priority. As a result, many employees and students have to carry on their workflow from home.

Despite a massive surge in the demand for this company’s product as a response to quarantine measures set in place, Uniform Accounting shows that growth has already been priced in—towering Uniform valuations and market expectations suggest that the stock may be overvalued.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Zoom’s major break seemingly happened overnight.

Daily average users hit a record 200 million in March, with active users up by 151% from the previous month. Now, amidst the pandemic, Zoom has become one of the most important apps in the world.

Before the company rose through the ranks, its founder Eric Yuan was actually just looking for a more efficient solution to keep his long-distance relationship afloat.

Instead of having to take 10-hour trains to visit his girlfriend, he decided to join WebEx in 1997 to design and build a web-conferencing product along with a team of engineers.

By the time WebEx was acquired by Cisco in 2007, the product they built had over 2 million users—but almost all of them were dissatisfied with the service.

WebEx was supposed to make it easier for conference-call attendees to communicate and share files. But the product had multiple problems—connectivity issues, outdated codebases, and limited functionalities, among other things.

When Cisco said that they wouldn’t be investing in modernizing WebEx or building a new web-conferencing product, Yuan decided that it was time to go.

He took the problems WebEx had and created his own web-conferencing product: Zoom.

Zoom launched its product in 2013, and initially had a user base of about a million.

However, through increased functionalities such as participant capacity expansion, and through strategic integration initiatives with Slack, Microsoft, Skype and Facebook, daily average users rose to 10 million by the end of 2018.

Three months later, that number has now multiplied by twenty.

With transportation services and at-office operations on halt, businesses are left with no choice but to let their employees work from home.

Web-conferencing has become one of the top options to ensure communication between employees, and Zoom, given its popularity, is the top tool of choice.

The company prides itself with their product’s functionality and ease of use:

- Users only need the link to launch the meeting

- It works on any device

- Installation is uncomplicated and takes only a few minutes

- Meetings can be recorded

- The audio and video are both high quality

As an added bonus, Zoom allows for the use of filters and background customization. People have been known to set their meetings with places like Paris or Tokyo, or some fictional place like Hogwarts, as their background.

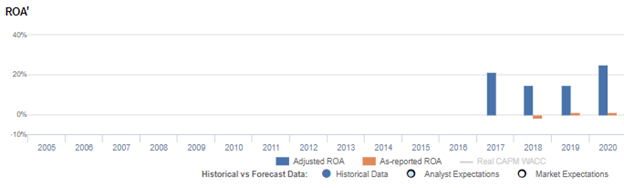

Because of the product’s differentiated user experience, the company has been able to maintain robust Uniform return on assets (ROA) of 16%-25% over the past four years, 16 times higher than as-reported ROAs.

What as-reported metrics fail to do is to consider excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

As in the case of Zoom, a substantial amount of cash received in 2019 from its IPO is sitting idly on the company’s balance sheet, inflating the asset base. As a result, as-reported ROA was at 1% in FY2020, significantly lower than the TRUE Uniform ROA of 25%.

But while the company is able to produce strong Uniform ROAs, the unprecedented product user growth that led to that strength revealed security and privacy flaws that the management should have foreseen beforehand.

Over the past few months, people have complained about “Zoombombers.” Uninvited attendees have interrupted Zoom meetings and remote classes while displaying highly suggestive images and images with racist undertones.

Since a link to the meeting is all that is needed, hackers have found ways to generate active meeting ID numbers and hijack shared screens. In some cases, cameras were forcibly activated without the user’s consent.

Although workarounds for these issues are relatively simple, such as password-protecting the meeting, the company’s less-than-stellar fundamental outlook proves to be a much bigger problem.

With the stock rallying about 45% to new highs, Zoom’s Uniform P/E currently stands at 324x. The company has a strong 25% ROA, but at current P/E levels, the market forecasts returns to rise to 60% in 2025. This implies that growth is already priced in.

Basically, the company is forecast to have an annual growth of 16%, but the market is pricing Zoom to have 84% earnings growth a year going forward.

It is highly unlikely that the company would be able to sustain the growth that the market is expecting, post-quarantine. This is partly because most of the management’s current efforts are focused towards fixing its privacy issues and are not about any specific growth initiatives.

With sky high valuations and market expectations, Zoom may well be overvalued.

Zoom’s earning power is still actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Uniform ROA has been higher than as-reported ROA in the past four years. For example, as-reported ROA for Zoom Video Communications, Inc. (ZM:USA) was 1% in FY2020, which is materially lower than its Uniform ROA of 25%.

Zoom’s Uniform ROA ranged from 15% to 25% over the past four years. From 22% in 2017, Uniform earning power fell to 15% in 2019. It then increased to a peak of 25% in FY2020.

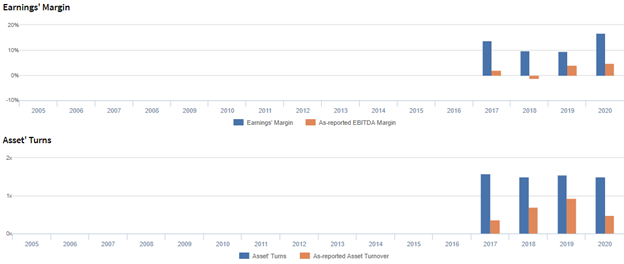

Zoom’s Uniform ROA is driven by robust Uniform earnings margins

Trends in Zoom’s Uniform ROA have largely been driven by trends in Uniform earnings margin, coupled with stable Uniform asset turns.

From 2017-2019, Uniform earnings margins declined from 14% to 9%, before recovering to 17% levels in FY2020. Meanwhile, Uniform asset turns have ranged from 1.5x-1.6x levels since 2017.

At current valuations, markets are pricing in expectations for both Uniform earnings margin and Uniform asset turns to reach new peaks.

SUMMARY and Zoom Video Communications Tearsheet

As the Uniform Accounting tearsheet for Zoom Video Communications, Inc. (ZM) highlights, Uniform P/E trades at 324.4x, which is far above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Zoom, the company has recently shown a 54% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Zoom’s Wall Street analyst-driven forecast is a shrinkage of 13% and a growth of 16% in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Zoom’s $150 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 84% each year over the next three years. What Wall Street analysts expect for Zoom’s earnings growth is far below what the current stock market valuation requires.

The company’s earning power is 4x the corporate average. Also, cash flows are about 6x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit risk and dividend risk.

To conclude, Zoom’s Uniform earnings growth is below peer averages. The company is also trading above average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com