Consulting Uniform Accounting will make it clear that this AI company has a 36% Uniform ROA, more robust than the as-reported 20%!

From only being able to compute 500-kilo flops of mathematical operations to almost replicating the computing power of the human brain, technology has seen exponential growth over the years.

This Indian company integrates its tech expertise and business intelligence to catalyze change and deliver results by providing quality and best-in-class consulting and IT solutions and services.

However, this is not reflected in the company’s as-reported returns. Uniform Accounting shows that the company’s innovative efforts resulted in a more robust Uniform return on assets (ROA).

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Some of us might be familiar with the term artificial intelligence (AI) because of the popularity of science fiction. For decades in pop culture, AI has been equated with robots and the recurring theme of the rise of robots. After all, its early beginnings could be traced back to the time scientists were curious enough about creating thinking machines.

Over 70 years have passed since the beginning of AI, and AI continues to evolve. It is no longer limited to scientific research or robots—it has become a part of our everyday lives. With the pervasiveness of AI, mankind is now considered to be in the Fourth Industrial Revolution.

According to the 2019 CIO Survey conducted by Gartner at the beginning of 2019, over 37% of organizations use AI in some form. IDC, a market intelligence and advisory services firm, is projecting global AI spending to double in the next four years to $110 billion. That’s a 20% compounded annual growth rate from 2019 to 2024.

AI has even extended to customer service, applying it to understand the trends and behaviours of consumers to better and quickly meet their needs. An example of this is how Netflix uses AI in the form of recommender systems that gives its viewers movies and TV series suggestions based on what they previously watched and what is popular in their region.

One company that benefits from the tailwind of the Fourth Industrial Revolution is Tata Consultancy Services Limited.

Through integrating AI and automation, Tata Consultancy pioneered both Machine First™️ Approach and TCS Pace™️ to bring effective business solutions to its stakeholders.

Through its Machine First™ approach (MFDM™), Tata Consultancy alleviates the challenges of various business choices in the digital era. This approach helps businesses automate processes, streamline decision-making, and improve a company’s efficiency, by giving technology the right of first refusal to do a task while focusing the human workers’ skills to more sophisticated jobs.

Tata Consultancy’s TCS Pace™️ aims to advance innovation thinking and to optimize resource expenditure that would give a competitive advantage to enterprises. Through translating TCS Pace Port Hubs from the idea of TCS Pace™️, Tata Consultancy allows you to engage with its co-innovation network partners, brainstorm with experts, collaborate with start-ups, research with academics, and work with its developers.

Today, with the help of its tech expertise and business intelligence in boosting continuous innovation, Tata Consultancy is considered as part of the top three most valuable brands in the IT services sector. Furthermore, leading branded business valuation consultancy Brand Finance named the company to be the fastest growing IT service brand worldwide in 2018.

Apart from providing business solutions to its clients, Tata Consultancy Services prioritizes research and innovation through its Innovation Labs. With its AI technology, the lab’s team of scientists were able to identify 31 molecular compounds that can help find a cure for COVID-19.

The company’s success in this area further solidifies its expertise in AI for its Life Sciences and Healthcare segment, which saw a 6.3% year-over-year revenue increase in its Q1 2021. The rest of the company’s units reported revenue declines during the pandemic.

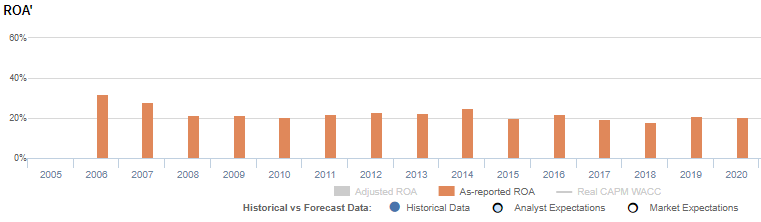

With its as-reported returns, Tata Consultancy seems to already be a fairly profitable business, thanks to its ability to innovate and maximize its operations in the AI space. Its as-reported ROA currently sits at 20%.

However, this is not an appropriate representation of Tata Consultancy’s earning power. Uniform Accounting shows that this company is actually a stronger business than what the market thinks.

What as-reported metrics fail to do is to consider the company’s excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

If excess cash remains included in the company’s asset base in computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is.

From 2014 to 2020, Tata Consultancy has had a significant amount of excess cash sitting idly in its balance sheet, ranging from 16% to 37% of its unadjusted total assets.

After excess cash and other significant adjustments are made, the company actually had a 36% Uniform ROA in 2020, which is much more robust than its as-reported ROA of 20%.

Tata Consultancy’s valuations are higher than as-reported

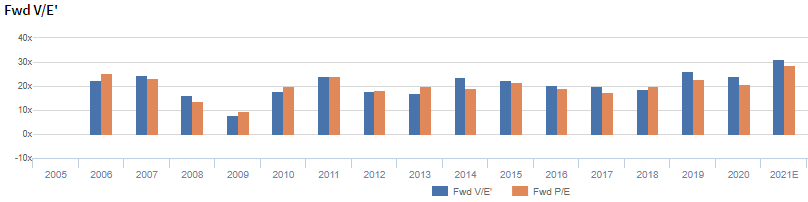

Tata Consultancy Services Limited (TCS:IND) currently trades above corporate averages at a 31.4x Uniform P/E (blue bars), above its as-reported P/E of 28.6x (orange bars).

At these levels, the market is pricing in expectations for Uniform ROA to improve to 48% in 2024, accompanied by 5% Uniform asset growth going forward.

Analysts have less bullish expectations, projecting Uniform ROA to remain at 36%-38% levels in 2022, accompanied by a 2% Uniform asset shrinkage.

Tata Consultancy’s profitability is much better than you think it is

As-reported metrics are distorting the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

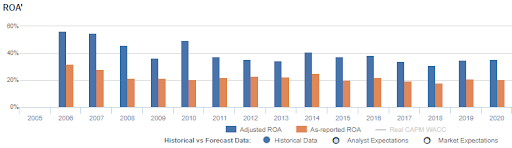

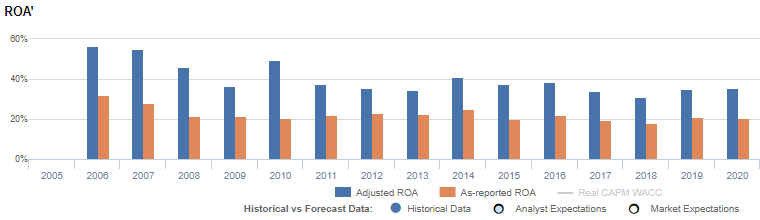

Tata Consultancy’s as-reported ROA has been significantly lower than its Uniform ROA in the past fifteen years. For example, as-reported ROA is 20% in 2020, drastically lower than its Uniform ROA of 36%. Uniform ROA reached an all-time high of 56% in 2006, when as-reported ROA was only 32%.

The company’s Uniform ROA for the past fifteen years has ranged from 31% to 56%, while as-reported ROA ranged only from 18% to 32% in the same timeframe.

From 56% in 2006, Uniform ROA gradually declined to 37% in 2009 before recovering to 49% in 2010. Afterwards, Uniform ROA gradually fell to 31% in 2018, before rebounding to 36% in 2020.

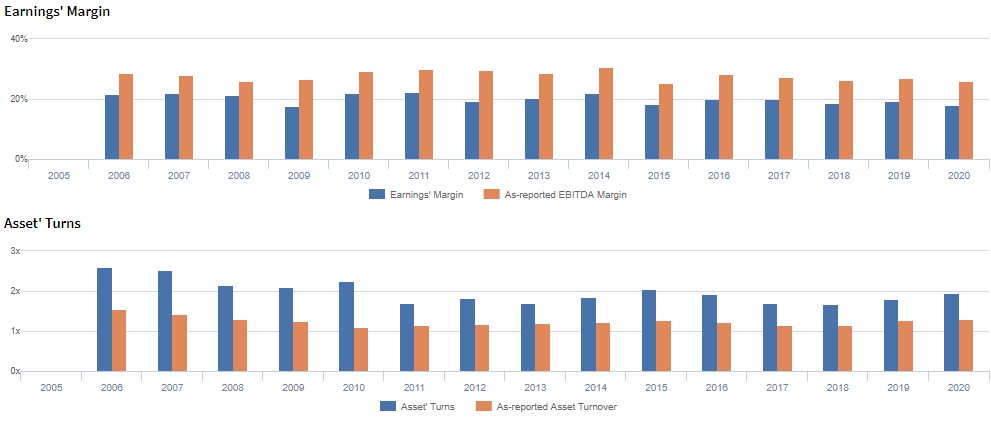

Tata Consultancy’s Uniform earnings margins are weaker than you think but its robust Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in Uniform asset turns, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform earnings margins fell from 22% levels in 2006-2008 to 18% in 2009, before recovering to 22% in 2014. It then gradually compressed back to 18% in 2020.

Meanwhile, Uniform asset turns fell from a peak of 2.6x in 2006 to an all-time low of 1.7x in 2011, before recovering to 2.0x in 2015. It then declined to 1.7x in 2018, before rebounding to 2.0x in 2020.

SUMMARY and Tata Consultancy Services Limited Tearsheet

As the Uniform Accounting tearsheet for Tata Consultancy Services Limited (TCS:IND) highlights, its Uniform P/E trades at 31.4x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Tata Consultancy, the company has recently shown a 2% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Indian Accounting Standards (Ind-AS) earnings and convert them to Uniform earnings forecasts. When we do this, Tata Consultancy’s sell-side analyst-driven forecast is a 1% earnings shrinkage in 2021 and a 12% growth in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Tata Consultancy’s INR 2,449.90 stock price. These are often referred to as market embedded expectations.

In order to justify current market expectations, Tata Consultancy would need to have Uniform earnings grow by 8% each year over the next three years. What sell-side analysts expect for Tata Consultancy’s earnings is below what the current stock market valuation requires in 2021, but above that requirement in 2022.

The company’s earning power is 6x the corporate average. Additionally, cash flows and cash on hand are above its total obligations—including debt maturities, capex maintenance, and dividends. This signals low credit and dividend risk.

To conclude, Tata Consultancy’s Uniform earnings growth is below its peer averages in 2021. However, the company is trading above its peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com