Cup noodles may be inexpensive, but the creator’s stock is just the opposite with a P/E of 36X (not 29X). Learn more about this noodle in an instant!

An average Filipino spends about 40%-60% of their budget on food. In a 2017 Kantar survey, it is estimated that Filipino households spend roughly PHP 4,900 just on snacks, which consist of biscuits, instant noodles, spreads, ice cream, cheese, pasta, and rice soup.

Among those snacks, instant noodles take the crown. With its versatility and endless flavor possibilities, it is no wonder Filipinos favor this snack over others, with Monde Nissin’s Lucky Me instant noodles enjoying a 98% penetration rate in Filipino households.

It makes sense to look at the company that started it all. And though its name is oddly similar to Monde Nissin, these two companies are in no way affiliated with each other.

Philippine Markets Daily:

Wednesday Uniform Earning Tearsheets – Asia-listed Focus

Powered by Valens Research

Instant noodles were invented by Momofuku Ando, founder of Nissin Foods Holdings Co., Ltd. (2897:JPN) in Japan, initially under the brand name Chikin Ramen.

Originally residing in Taiwan, Ando returned to his hometown Osaka after World War II. It was there where he witnessed a scene that would be so engraved in his memory that he would draw inspiration from this several years later.

In one of Ando’s walks when he relocated to Japan, he encountered a small ramen stall that was surrounded by a good number of people. They were all waiting in line just to be able to eat ramen, the Japanese’s comfort food.

At that time, he thought nothing of it.

Years later, the bank he was president of closed down.

During that time, food shortage in Japan was still a major problem. Ando wanted to address this issue for his next venture.

It was then that Ando recalled the ramen memory and got to work on creating instant noodles, which to him was the answer to hunger since it was going to be convenient and cheap.

In 1958, Chikin Ramen was born.

Instant noodles did not start out as the affordable snack that it is today.

Because of its novelty, it was more expensive than fresh noodles. In time, though, the Japanese consumers fully embraced this quick way to prepare tasty and satisfying ramen at home.

The success he enjoyed locally motivated him to set his sights on global expansion.

In 1971, Cup Noodles debuted in the US, though it was first introduced at Isetan Department Store in Shinjuku district, Tokyo that same year.

Today, 10 out of the top 15 countries with the highest demand for instant noodles in the world are in Asia, with China holding the number 1 spot, while Japan and the Philippines placed 4th and 7th, respectively.

Since their introduction, instant noodles have undergone numerous improvements to match the ever-growing market of consumers.

In July 2005, testament to Ando’s continual innovation of their products, Nissin developed Space Ram, the instant noodles that can be consumed in space. The first man who ate instant noodles in zero-G was Astronaut Soichi Noguchi.

Nissin’s philosophy, which is formed from Ando’s ideas and beliefs, is encapsulated into four tenets:

- Peace will come to the world when there is enough food

- Create foods to serve society

- Eat wisely for beauty and health

- Food-related jobs are a sacred profession

It hasn’t always been blue skies for Nissin and instant noodles. Many studies have been made that link instant noodles to illnesses because of the preservatives used to prolong their shelf life.

Being highly processed, instant noodles have high sodium content. Making this a staple in one’s diet will lead to health problems like hypertension, kidney stones, and high blood pressure leading to heart diseases.

Since promoting a healthy lifestyle is one of Nissin’s business tenets, they released the Cup Noodle Light in 2009 and Cup Noodle Nice in 2017.

In 2019, they released All-In Pasta, a nutritious kind of instant noodles that contains approximately one-third of a person’s daily nutrition needs. It has 13 different vitamins, 13 minerals, and high amounts of protein and dietary fiber.

Moreover, Nissin has been aiming to become a “Century Brand Company,” which means they are focusing on having brands that can exist for 100 years. To achieve this goal, they are focused on the promotion of the global branding of Cup Noodles.

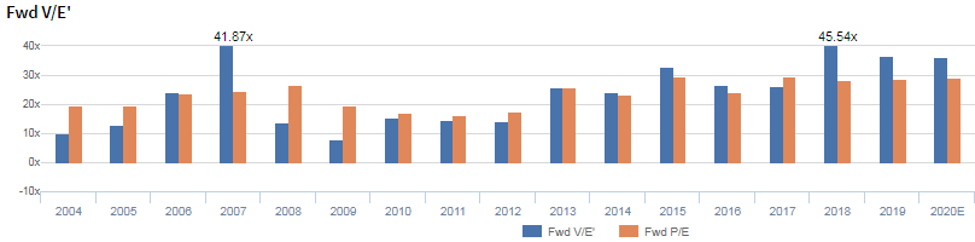

Nissin Foods is trading at a higher valuation than you think

Nissin Foods currently trades around recent averages with a 36.1x Uniform P/E (blue bars).

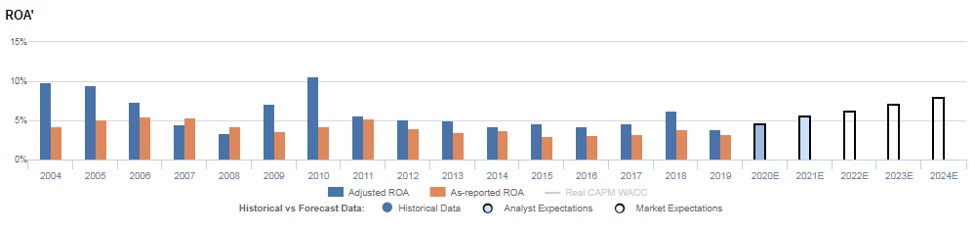

At these levels, the market is pricing in expectations for Uniform ROA to expand from 4% in 2019 to 8% in 2024, accompanied by 5% Uniform asset growth going forward.

However, analysts have muted expectations, projecting Uniform ROA to improve to 6% in 2020, accompanied by 8% Uniform asset growth.

Nissin Foods’ earning power is actually better than you think it is

Nissin Foods began with cyclical profitability that stabilized thereafter, with Uniform ROA ranging from a high of 11% to a low of 3% over the past 16 years.

Uniform ROA fell from 10% in 2004 to a historical low of 3% in 2008, before rising to a peak of 11% in 2010. Afterwards, Uniform ROA remained at 4%-6% levels, with 2019 being in the lower end of that range.

Meanwhile, Uniform asset growth was positive in 14 of the past 16 years, while ranging from -1% to 8%, except for the 32% asset growth in 2007 due to their acquisition of Myojo Foods.

As-reported metrics are understating Nissin Foods’ profitability.

For example, as-reported ROA was near 3% levels in 2019, lower than the Uniform ROA of 4%, making the company look like a weaker business than real economic metrics highlight.

Moreover, as-reported ROA has been below Uniform ROA for the past 16 years, except for 2007 and 2008, significantly distorting the market’s perception of the firm’s historical profitability trends.

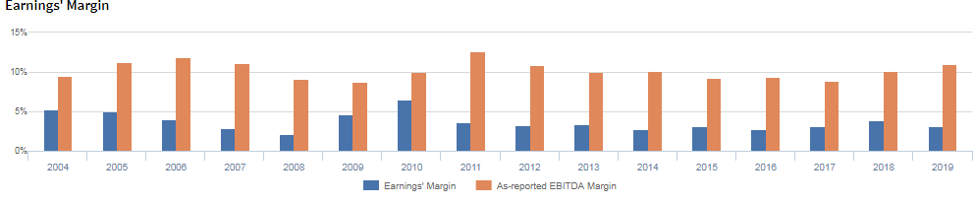

Nissin Foods’ margins are weaker than you think

Cyclicality in Uniform ROA has been driven primarily by trends in Uniform earnings margins, with peaks and troughs lining up historically with that of Uniform ROA.

After dropping from 5% in 2004 to 2% in 2008, Uniform earnings margins rose to 7% in 2010. Thereafter, Uniform earnings margins remained at 3% to 4% levels, with 2019 having a Uniform earnings margin of 3%.

Meanwhile, after staying at 1.9x from 2004 to 2006, Uniform asset turns stabilized at 1.5x-1.6x from 2007 to 2018, before compressing to 1.2x in 2019. At current valuations, markets are pricing in expectations for Uniform earnings margins and Uniform asset turns to return to improve.

SUMMARY and Nissin Foods Holdings Co., Ltd. Tearsheet

As the Uniform Accounting tearsheet for Nissin Foods Holdings Co., Ltd. highlights, Nissin trades at 36.1x Uniform P/E, which is above market average valuations, and around its recent average levels.

High P/Es require high EPS growth to sustain them. In the case of Nissin Foods, the company has recently shown a 33% decline in Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for JMIS earnings and convert them to Uniform earnings forecasts. When we do this, Nissin Foods’ sell-side analyst-driven forecast is for Uniform earnings to grow by 33% and 21% in 2020 and 2021, respectively.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify JPY 8,170 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels of Nissin Foods, the company would have to have Uniform earnings grow by 20% each year over the next three years.

What sell-side analysts expect for Nissin Foods earnings growth falls far below what the current stock market valuation requires.

To conclude, Nissin’s Uniform earnings growth is well above peer averages in 2020. Moreover, the company is trading at above average peer valuations.

The company’s earning power, based on its Uniform return on assets calculation, is in line with corporate averages. Furthermore, with cash flows and cash on hand consistently exceeding obligations, Nissin has low credit and dividend risk.

About the Philippine Market Daily

“Wednesday Uniform Earning Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing himself, Benjamin Graham

Warren Buffett and Charles Munger of Berkshire Hathaway; David Sanford Gottesman of First Manhattan Co.; Walter Schloss of WJS Partners; William Ruane of Ruane Cuniff, Sequoia Fund; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com