Credited with the “athleisure” trend, this apparel company successfully cultivated its fitness lifestyle brand and got healthy Uniform ROAs of 20%+

Athleisure, or casual and comfortable everyday athletic wear, has become a popular trend mainly among millennials becoming more conscious about fitness and health.

Credited for the popularization of this trend, this company was able to take advantage of secular trends in both the fitness and fashion industry by cultivating a successful lifestyle brand and developing innovative programs to support this marketing strategy.

Because of this, it was able to position itself as a powerhouse in the apparel industry. But while as-reported metrics make it seem like the business has had weak returns, Uniform Accounting reveals that it has had returns consistently above 20%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Athleisure has taken the fashion world by storm and has become the signature trend of the 21st century. A portmanteau of ‘athletic’ and ‘leisure,’ athleisure is any form of casual, comfortable exercise wear that can also be worn for other daily activities.

The past decade has seen a massive cultural shift, with millennials placing a heavier emphasis on fitness and health. Incorporating this shift into street style fashion contributed significantly to the popularization of athleisure.

In fact, according to Morgan Stanley, the athleisure trend has grown 40% over the last seven years, and is expected to grow another 30% this year.

Lululemon Athletica (LULU), regarded as the creator of athleisure, took advantage of the secular trends in both the health and fashion industry and positioned itself well, becoming the retail behemoth that it is today.

Much of Lululemon’s success can be attributed to the way it cultivates its brand—the company focused on being a lifestyle brand, and not just a business selling a product. This is similar to how one of its competitors, Nike, executes its marketing strategy.

Nike sells the athletic lifestyle. It’s based on the idea that athletes and non-athletes alike should be empowered to work towards their fitness goals, with this marketing objective encapsulated perfectly in their iconic slogan, “Just Do It.”

Lululemon sells the healthy mind, body, and soul lifestyle. To further reinforce its brand image, the company sells its products to wholesale customers such as gyms, yoga studios, and other health and fitness clubs.

However, Lululemon sets itself apart from its competitors by adding an experiential element to customer shopping. A few of their largest stores offered amenities such as fitness studios, meditation rooms, and a “fuel bar” serving healthy food and drink options.

A “gear trial program” is also offered, allowing its consumers to test drive their apparel during an in-store studio workout. Leveling up the customer experience by introducing initiatives that tied in with the Lululemon lifestyle allowed the company to command a premium price on its products.

More importantly, this experience fosters a feeling of community by enabling customers to interact with each other as well as with the business. Building customer relationships and driving community growth has helped the company amass a loyal customer base.

Lululemon plans to invest more in these experiential stores to drive foot traffic and revenue, increasing to about 10% of its entire store fleet over the next few years, as part of their retail store expansion.

In line with the expansion, the company will be continuing with its pop-up store concept, which allows it to test new markets before setting up shop permanently. The ones that perform well will stay, while the others will close down.

Historically, this particular strategy has enabled the company to scale up the business efficiently. Coupled with its lifestyle brand strategy to market its products, Lululemon has become a powerhouse in the athleisure apparel industry.

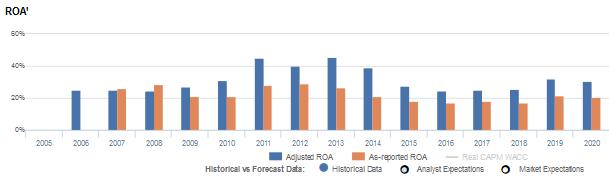

Uniform Accounting portrays this accurately, with Uniform ROAs ranging from 25%-46% over a fourteen-year period. This is in contrast to lower as-reported ROAs, making it seem like Lululemon is a weaker business than it actually is.

The distortion comes from as-reported metrics failing to consider the number of operating leases Lululemon has from their numerous existing retail stores.

The decision management makes between investing in capex and investing in a lease is based on how management wants to finance their investments. Choosing to lease an asset, however, would not be treated as an investment, but as an expense that would impact the income statement.

Specifically, operating leases on Lululemon’s income statement are understating the company’s true earnings. Adjusting for the rent expense distortion, which historically has been about a third of its income, returns are actually stronger.

However, even with robust returns, current valuations for the company are astronomically high, standing at a Uniform P/E of 62x. This means that the market is pricing in significant optimism for the company, with expectations for ROA to ramp from 30% in 2020 to almost double to 50% in 2025.

With Lululemon’s returns coming under pressure, having lost out on in-store sales due to the pandemic, and seeing rising competition in the space from brands such as Nike and Aerie, the company will have difficulties meeting market expectations.

So while secular trends and tailwinds might justify the company’s complementary retail expansion plans, it does not justify its valuations.

Lululemon’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Lululemon’s Uniform ROA has actually been higher than its as-reported ROA in thirteen of the past fifteen years. For example, as-reported ROA was 21% in 2020, but its Uniform ROA was actually higher at 30%.

Furthermore, Lululemon’s Uniform ROA has ranged from 25% to 36% in the past fifteen years while as-reported ROA ranged only from 17% to 29% in the same timeframe.

From 2006-2013, Uniform ROA gradually rose to a peak of 46%, excluding the 45% outperformance in 2011. Thereafter, it compressed to 30% in 2020.

Lululemon’s Uniform earnings margins are weaker than you think, but its robust Uniform asset turns make up for it

Lululemon’s trends in profitability have been driven by trends in Uniform earnings margins and to a lesser extent, Uniform asset turns.

From 2006-2013, Uniform earnings margins improved from 11% to 22%, before gradually falling to 14% levels in 2015-2018 and expanding to 17% in 2020.

Meanwhile, Uniform turns declined from a peak of 2.4x in 2007 to 1.7x in 2008-2009, before expanding back to 2.4x in 2011. It then compressed to 1.7x-1.8x levels in 2016-2018, before recovering to 2.1x in 2019. Thereafter, Uniform turns fell back to 1.7x in 2020.

At current valuations, markets are pricing in an expectation for Uniform margins to continue expanding and for Uniform turns to reverse its recent deterioration.

SUMMARY and Lululemon Tearsheet

As the Uniform Accounting tearsheet for Lululemon Athletica Inc. (LULU) highlights, its Uniform P/E trades at 70.4x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Lululemon, the company has recently shown a 40% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Lululemon’s Wall Street analyst-driven forecast is a 16% EPS shrinkage in 2021 and a 46% EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Lululemon’s $349 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 34% each year over the next three years to justify current prices. What Wall Street analysts expect for Lululemon’s earnings growth is below what the current stock market valuation requires in 2020, but above its requirement in 2021.

Furthermore, the company’s earning power is 5x the corporate average. Also, cash flows are 5x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Lululemon’s Uniform earnings growth is above its peer averages in 2020. Therefore, as is warranted, the company is also trading above average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com