Despite short-term headwinds, strong macroeconomic fundamentals warrant long-term earnings growth potential for this fund

The spread of coronavirus disease 2019 (COVID-19) has had major ramifications in the stock market. Not only have the stock prices been down, but the Philippine Stock Exchange (PSE) has taken necessary actions to address further stock market fluctuations.

Among the different sectors, consumer discretionary saw one of the biggest declines amid COVID-19 and the enforcement of the enhanced community quarantine. Meanwhile, consumer staples performed better, which often is the case in situations like this.

In today’s Philippine Markets Daily (PMD), we take a look at the BPI Invest Philippine Consumer Equity Index Fund.

In addition, we’re including fundamental analysis of one of the fund’s largest holdings, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Philippine Markets Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

Over the past weeks, the stock market has taken a beating from a broad-based panic selling driven by coronavirus-induced fears.

The Philippine Stock Exchange Index (PSEi) plummeted 31% from 7,742.53 on January 2, 2020 to 5,335.37 on March 16, 2020. This prompted the PSE to reduce the lower limit of the trading threshold from 50% to 30%, in an effort to address the volatility in the stock market.

This is in the midst of the global COVID-19 pandemic, whereby the entire Luzon was placed in an enhanced community quarantine on March 17, 2020 to prevent the ongoing spread of COVID-19.

In line with this, mass public transport has been suspended while travel by land, sea, and air has been restricted. Malls were closed as well and only those private establishments that provide basic needs are open.

The spread of coronavirus has indeed disturbed the day-to-day trade and has instantaneously become a massive threat to the global economy. It has shaken up business operations and consumer behavior on a large scale.

While the full economic impact of this event remains unclear, the drastic effect of COVID-19—and the extreme measures the government is implementing to contain it—has already begun materializing across different sectors and industries, particularly the consumer sector.

We take a look at one Philippine fund in particular that focuses on the consumer sector.

BPI’s consumer equity index fund invests in Philippine companies who derive their sales from consumer-related business activities.

The fund was launched on January 16, 2017, giving investors an opportunity to invest in the top consumer names in the country.

After enjoying around 30% investment returns in 2017, the fund suffered from a lackluster 2018 and a volatile 2019. Since inception, BPI Consumer Equity Index Fund saw a total cumulative performance of -6.8%, slightly lower than PSEi’s -6.2% performance over the same period.

Year-to-date, the fund suffered with 29% investment losses. Meanwhile, the PSEi saw a 31% decline year-to-date.

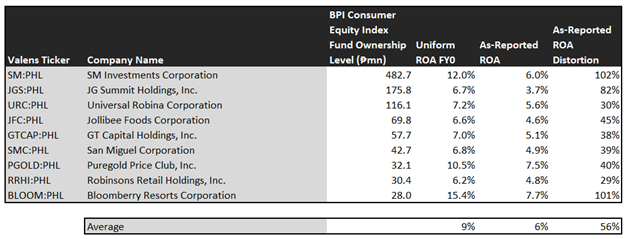

The table below lists the top consumer holdings of the BPI Invest Philippine Consumer Equity Index Fund. These consumer companies have taken a hit from this black swan event in one way or another. Most of these companies, if not all, experienced interruptions in their business operations and have temporarily closed their stores and malls.

The table also shows the Uniform return on assets (ROA) and as-reported ROA of these companies, as well as the ROA distortion—the difference between Uniform and as-reported ROA.

In 2019, this investment fund generated an average as-reported ROA of 6%, in line with corporate average returns.

However, on a Uniform Accounting basis, this fund has actually delivered stronger earnings with an average Uniform ROA of 9%, which is above cost-of-capital levels. Uniform Accounting adjusts for the distortions in companies’ financial statements brought about by the inconsistencies in the Philippine Financial Reporting Standards (PFRS) to reveal the true underlying performance of companies.

As such, it should not be surprising that when analyzing the non-financial holdings of the BPI Invest Philippine Consumer Equity Index Fund, the figures that easily stand out are the double-digit discrepancies between Uniform ROA and as-reported ROA for these companies.

While the difference in raw figures may not seem too distant, the distortion in percentage ranges from 29% to 102%, with SM Investments Corporation (SM:PHL) and Bloomberry Resorts Corporation (BLOOM:PHL) both having distortions above a hundred percent.

As-reported ROA understates the earning power of SM, treating it as an average company, when in reality, it is actually a high-quality firm with Uniform ROA of 12%—twice global corporate averages. The country’s largest conglomerate has been consistently generating economic profit for the past decade.

Similarly, Bloomberry is far more robust than what as-reported numbers suggest, with a 15% Uniform ROA compared to 8% as-reported ROA.

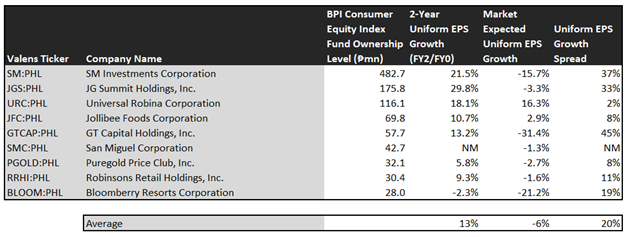

This table shows the earnings growth potential of the top holdings of the BPI Invest Philippine Consumer Equity Index Fund. It features three key data points:

- The 2-year Uniform EPS growth represents the Uniform earnings growth the company is likely to have for the next two years. The earnings number used is the value of when we convert consensus sell-side analyst estimates to the Uniform Accounting framework.

- The market expected Uniform EPS growth represents what the market thinks Uniform earnings growth is going to be for the next two years. Here, we show by how much the company needs to grow Uniform earnings in the next two years to justify the current stock price of the company. This is the market’s embedded expectations for Uniform earnings growth.

- The Uniform EPS growth spread is the difference between the 2-year Uniform EPS growth and market expected Uniform EPS growth.

On average, Philippine companies are expected to have 6% annual Uniform earnings growth over the next two years. Meanwhile, BPI’s consumer equity fund’s top holdings are forecast to surpass that with 13% projected Uniform earnings growth in the next two years.

The market, on the other hand, sees a decline for these companies with market-expected Uniform EPS shrinkage of 6% over the next two years.

Among these companies, GT Capital Holdings, Inc. (GTCAP:PHL) and SM Investments have the highest Uniform earnings growth dislocation.

The market is pricing GTCAP’s Uniform Earnings to plummet by 31% in the next two years. However, sell-side analysts are seeing sustained earnings growth for the firm, forecasting it to accelerate by 13%.

Similarly, the market is seeing SM’s uniform earnings to plunge by 16%, but analysts are projecting a robust 22% earnings growth for the firm in the next two years.

Overall, one might think that this portfolio is average with an ROA of 6% and projected earnings decline. However, through the lens of Uniform Accounting, investors can see clearly that the BPI Invest Philippine Consumer Equity Index Fund comprises mostly high-quality companies with healthy profitability levels and double-digit earnings growth potential.

This fund may face continued short-term fluctuations from the COVID-19 outbreak, trade tensions between the U.S. and China, domestic regulatory concerns, and issues around Philippine Offshore Gaming Operators (POGO). However, long-term fundamentals surrounding the Philippines remain intact, providing solid support that warrant long-term equity upside.

Jollibee Foods Corporation Tearsheet

Today, we’re highlighting one of the largest individual stock holdings in BPI Investment Philippine Consumer Equity Index Fund—Jollibee Foods Corporation.

As our Uniform Accounting tearsheet for Jollibee Foods Corporation (JFC:PHL) highlights, Uniform P/E trades in line with global corporate averages at 23.0x, but well below its historical average valuations.

High P/Es require high EPS growth to sustain them. In the case of Jollibee Foods Corporation, the company has recently shown a 6% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that poorly track reality. However, sell-side analysts have a strong grasp on near-term financial forecasts like revenue and earnings.

We take sell-side forecasts for PFRS earnings as a starting point for our Uniform earnings forecasts. When we do this, Jollibee Foods Corporation’s sell-side analyst-driven forecast shows that Uniform earnings will grow by 2% in 2019 and 20% in 2020.

Based on the current stock market valuations, we can back into the required earnings growth rate that would justify PHP 170 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels of Jollibee Foods Corporation, the company would have to see Uniform earnings grow by 3% each year over the next three years. Sell-side analysts’ expected 20% earnings growth for Jollibee Food Corporation is well above what the current stock market valuation requires.

The company has an earning power around long-run corporate averages—based on its Uniform ROA calculation. Moreover, with cash flows and cash on hand consistently exceeding obligations in the next five years, Jollibee Foods Corporation has a low dividend risk.

To conclude, Jollibee Foods Corporation’s Uniform earnings growth is well above peer averages in 2019. Moreover, the company is trading around peer average valuations.

About the Philippine Market Daily

“Friday Uniform Portfolio Analytics”

Investors who don’t engage in the buying or selling of securities for a living oftentimes rely on professionals to manage their own investments within the scope of their investment policies.

With so many funds and managers out there, it can get confusing and difficult to decide which one best suits your needs as an investor.

Every Friday, we focus on one fund in the Philippines and take a deeper look into their current holdings. Using Uniform Accounting, we identify the high-quality stocks in their portfolio which may not be obvious using the as-reported numbers.

We also identify which holdings may be problematic for the fund’s returns that they would need to reconsider from a UAFRS perspective.

To wrap up the fund analysis, we highlight one of their largest holdings and focus on key metrics to watch out for, accessible in our tearsheets.

Hope you’ve found this week’s focus on the BPI Invest Philippine Consumer Equity Index Fund interesting and insightful.

Stay tuned for next week’s Friday Uniform Portfolio Analytics!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com