Even with additional exposure from its global expansion, this pharmaceutical company’s earnings margin is only at 7%, not 20%

For decades, the blow-fill-seal (BFS) technology has been beneficial to many pharmaceutical companies around the globe because of its convenient and contamination-free process.

This company pioneered this technology in the Philippines and further drove its growth by expanding its distribution network. However, as-reported metrics seem to be exaggerating the further potential of the company’s strategies.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

For as long as we can remember, diseases of all kinds—such as Tetanus, Influenza, and Polio—have become long-standing issues in the medical community, uniting scientists and doctors alike from all over the globe in search for the right treatments.

Thanks to technological innovation and scientific discovery, some of these illnesses have been eradicated by vaccines in most, if not all, countries around the world. However, developing vaccines is just one part of the equation; handling and administering them is the other part.

One of the techniques pharmaceutical companies use to efficiently handle and administer vaccines is the blow-fill seal (BFS) technology. This invention originally came from Europe in the 1930s and was envisioned by Gerhard Hansen while he was working on his first company, Thermo-Pack.

The process is simple: in one automatic process, bottelpack machines will produce containers from thermoplastic granules (blow), insert the liquid product inside (fill), and immediately seal the container (seal). This ensures low chances of product contamination.

In the Philippines, Euro-Med Laboratories (EURO:PHL) was the one who pioneered the utilization of this technology. Through this method, the company was able to produce sterile and pyrogen-free intravenous (IV) solutions in plastic containers, eventually making it the largest manufacturer of such high-quality fluids in Asia.

Besides this, Euro-Med also specializes in making sterile water for injection, as well as other specialty solutions—like ophthalmic, inhalation, irrigation, and dialysis—to name a few.

Through the years, the company has maintained its position in the industry by using the BFS technology. While that boosted the company’s business, having an extensive marketing and distribution network also played an important role in Euro-Med’s success.

By strategically placing provincial depots across the country, Euro-Med successfully expanded its market reach to key cities such as Cavite, Bulacan, and Manila.

After expanding domestically, the company set its sights on the opportunity of globally exporting its products.

Currently, the company has already reached more than 20 other countries in Asia, with plans to continue expanding outside of the continent. To date, export sales contribute 8% of the company’s overall sales.

Furthermore, the company also engaged with acquisition activities as part of its expansion initiatives. In 2016, Euro-Med acquired Antech’s Dr. Edwards brand, giving the company the rights to Dr. Edwards’ trade name and access to its entire product inventory, such as bottled water, purified water, and sterilized water.

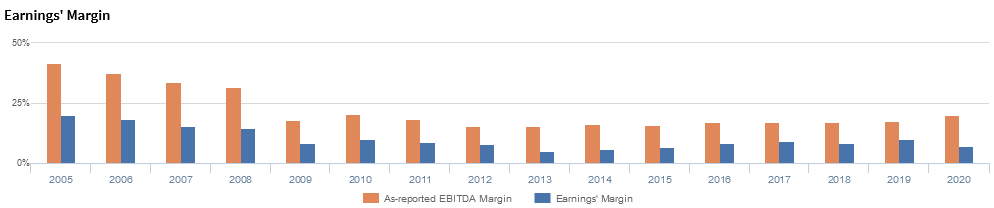

Looking at the company’s as-reported metrics, it seems that Euro-Med was able to produce generally improving returns after the global financial crisis, with margins reaching 20% in 2020.

In reality, these strategies actually resulted in margins of only 7% in recent years.

What as-reported financials have gotten wrong is the depreciation of the company’s fixed assets.

Depreciation expense is a non-cash expense, meaning it does not represent an actual outlay of cash. As such, depreciation expense should be added back to earnings. Also, it can be easily manipulated by changing the asset’s life.

However, companies do spend cash on maintenance capital expenditures to ready the same assets for use in the following years. That said, this expense barely shows up in its entirety on the balance sheet.

To arrive at an estimate of the firm’s maintenance capex, what is done instead is smoothing as-reported depreciation expense over a few years, adjusting for inflation and asset impairments.

In Euro-Med’s case, PHP 222.1 million of depreciation expense was charged in 2020, but its substantial growth in assets that year warranted PHP 115.4 million in maintenance capex.

Along with the many other needed adjustments made, adding back depreciation expense and subtracting maintenance capex leads to just PHP 688.0 million in Uniform earnings and a 7% Uniform margins in 2020, lower than as-reported EBITDA of PHP 763.0 million and 20% EBITDA margin.

Euro-Med’s earning power is weaker than you think

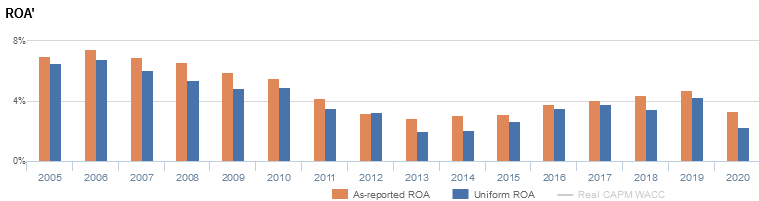

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that Euro-Med is a much stronger business than real economic metrics highlight.

Euro-Med’s Uniform ROA has actually been lower than its as-reported ROA for the past sixteen years. For example, as-reported ROA was 7% in 2008, but Uniform ROA is displaying weaker profitability at 5%.

Historically, as-reported ROA declined from a peak of 8% in 2006 to a low of 3% in 2013, before improving to 5% in 2019 and subsequently contracting to 3% in 2020.

Uniform ROAs followed a similar trend. After fading from a peak of 7% in 2006 to 2% lows in 2013-2014, Uniform ROA expanded to 4% in 2019, before compressing to 2% in 2020.

Euro-Med’s earnings margin is weaker than you think

Euro-Med’s historical performance has been driven primarily by trends in Uniform earnings margin, a key driver of profitability.

As-reported margins fell from a peak of 42% in 2005 to a low of 15% in 2013, before subsequently expanding to 20% in 2020.

Meanwhile, after falling from 20% in 2005 to 8% in 2009, Uniform margins improved to 10% in 2010 before declining to a low of 5% in 2013. Thereafter, Uniform turns gradually expanded to 10% in 2019, before contracting to 7% in 2020.

As-reported metrics are making the firm appear to be more profitable than real economic metrics highlight.

SUMMARY and Euro-Med Laboratories Phil., Inc. Tearsheet

As the Uniform Accounting tearsheet for Euro-Med Laboratories Phil., Inc. (EURO:PHL) highlights, it trades at a Uniform P/E of 40.4x, above the global corporate average of 23.7x, but around its historical average of 38.8x.

High P/Es require high EPS growth to sustain them. In the case of Euro-Med, the company has recently shown an 82% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Euro-Med’s sell-side analyst-driven forecast calls for a 52% and an immaterial Uniform EPS growth in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Euro-Med’s PHP 1.90 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 13% annually over the next three years. What sell-side analysts expect for Euro-Med’s earnings growth is above what the current stock market valuation requires in 2021, but below the requirement in 2022.

Furthermore, the company’s earning power is below the long-run corporate average, and cash flows and cash on hand are also below total obligations—including debt maturities, capex maintenance, and dividends. Moreover, intrinsic credit risk is 710bps above the risk free rate. All in all, this signals a high dividend risk.

To conclude, Euro-Med’s Uniform earnings growth is way above its peer averages, and the company is also trading way above its average peer valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com