Expanding its asset base has actually made this logistic firm more efficient with 1.8x Uniform asset turns

The ongoing coronavirus pandemic has placed the world’s supply chain and logistics networks to the test. Some, like the automotive supply chain, have seen massive factory shutdowns, its effects reverberating across its customers.

Other networks have been more resilient, through shrewd asset management efforts. Such is the case for the Philippines’ largest courier and cargo company, although its as-reported financials are incorrectly telling a different story.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

In the Philippine Statistics Authority’s June 2020 report, it’s estimated that at any given time between April to September 2019, over 2 million Filipinos worked abroad. These Overseas Filipino Workers (OFWs) held a variety of jobs, including as technicians and associate professionals, machine operators and assemblers, and service and sales workers. Nearly 40% of OFWs worked at elementary occupations.

In the same period, OFWs brought in over PHP 211 billion in remittances, accounting for about 10% of the Philippine GDP. In addition to OFWs sending that much cash to their families back home, many of them prefer to also send items from abroad. Hence, we have the tradition of the balikbayan box.

Balikbayan boxes might be just a box of foreign goods for others, but sending gifts through parcels holds a strong emotional and cultural importance to many Filipinos. In fact, Philippine customs laws have been amended just to exclude balikbayan boxes from certain tariff restrictions.

In the past twenty years, no other company has delivered balikbayan boxes to their destinations in the Philippines more than LBC Express Holdings, Inc. (LBC:PHL). This service helped propel the firm to become the largest cargo and courier company in the Philippines.

Famous for the line ‘We like to move it,’ LBC has become a logistics giant, also dominating the markets of cash payments, money remittances, and corporate logistics services.

Starting out as an air cargo agent in 1945 under the name Luzon Brokerage Company, the company began venturing into the express delivery service business.

LBC continued to expand its logistics network until it established its first branch outside the Philippines in 1985, paving the way for OFWs to start sending their Balikbayan boxes back home.

The growing number of OFWs played a key role in LBC’s success not only in the logistics space, but also in the money transfer over the years. OFW remittances peaked at 13% of the Philippine GDP in 2005.

Thanks to the freight forwarding activity driven by overseas workers, LBC was able to add bills payment, secured mail service, and other such services to their branches from 2005-2010. Still, LBC maintained a broad focus by offering personal services as well as logistics tailored to corporations.

Today, the boom of e-commerce is bringing LBC to reach a new level. To capitalize on this industry tailwind, the firm introduced its cash-on-delivery and cash-on-pick up (COD/COP) services for its retail customers.

With its continuous expansion into different logistical fields, LBC’s asset base has ballooned to record-highs. Excluding 2019, the firm has consistently grown its real Uniform assets in each year since its backdoor listing.

However, such rapid pace of asset growth can be worrisome to investors, especially if assets are mismanaged or if they do not generate sufficient revenues. In other words, asset growth can be detrimental if it sinks LBC’s asset utilization, a key driver of profitability.

As-reported financials are claiming LBC’s as-reported asset turnover to be fading, making it look like the firm is performing less efficiently than its competitors. Since 2014, as-reported asset turnover has been slowly falling to a historical low of 1.1x in 2019.

In reality though, LBC has grown to be a more asset efficient business, even with its various expansion initiatives. The company’s Uniform asset turns show that it has reached a new peak of 1.8x in 2019, significantly higher than what as-reported metrics state.

One of the main contributors to such discrepancy is its treatment of excess cash. While as-reported financials treat LBC’s entire cash balance as part of its asset base, Uniform Accounting removes the cash not necessary to operate and fulfill obligations—cash above what one might view as “operating” cash.

The purpose of removing excess cash is to see what the true operating assets of the firm are. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

Since LBC has maintained a substantial cash balance each year, the company’s Uniform asset base has seen a substantial deflation. In 2019, LBC’s cash balance was carrying PHP 3.6 billion more than operationally required, making up a quarter of the company’s PHP 14.1 billion as-reported assets.

Removing excess cash along with the other necessary adjustments in Uniform Accounting, we arrive at LBC’s true PHP 8.5 billion Uniform asset base and a 1.8x Uniform asset turnover.

LBC’s earning power is stronger than you think

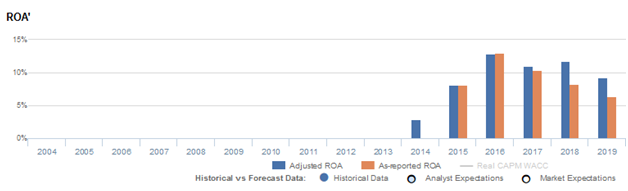

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

LBC’s Uniform ROA has actually been higher than its as-reported ROA in the past two years. For example, as-reported ROA was 6% in 2019, but Uniform ROA is showing stronger profitability at 9%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually become stronger recently.

As-reported ROA improved from 8% in 2015 to 13% in 2016, before contracting to 6% in 2019. However, after rising from a low of 3% in 2014 to a peak of 13% in 2016, Uniform ROA slowly declined to just 9% in 2019.

LBC is a more asset efficient business than you think

LBC’s performance has been driven primarily by strong Uniform asset turns, a key driver of profitability.

From 2014 to 2016, as-reported asset turnover gradually declined from 1.4x to 1.1x levels through 2019. Meanwhile, although Uniform asset turns declined from 1.3x in 2014 to 1.1x levels in 2016, Uniform asset turns steadily rebounded to a peak of 1.8x in 2019.

As-reported metrics are making the firm appear to be a less efficient business than real economic metrics highlight.

SUMMARY and LBC Express Holdings, Inc. Tearsheet

As the Uniform Accounting tearsheet for LBC highlights, the Uniform P/E trades at 34.8x, which is above corporate average valuation levels and its own history.

High P/Es require high EPS growth to sustain them. In the case of LBC, the company has recently shown a 44% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, LBC’s sell-side analyst-driven forecast calls for an 11% and 14% Uniform EPS decline in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify LBC’s PHP 14.20 stock price. These are often referred to as market embedded expectations.

The company would need to grow its EPS by 5% each year over the next three years to justify current valuations. What sell-side analysts expect for LBC’s earnings growth is below what the current stock market valuation requires.

Furthermore, the company’s earning power is above the long-run corporate average. However, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals high credit and dividend risk.

To conclude, LBC’s Uniform earnings growth is above peer averages, and the company is trading above its peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com