Expansion initiatives and resilience have allowed this home improvement company to build up a Uniform ROA of 6%, not 4%

This home improvement retailer continues to stay resilient in the face of headwinds thanks to its continuous portfolio expansion and improving margins.

Despite the company’s efforts to grow its product reach and build its presence in the industry, as-reported metrics do not reflect the effectiveness of these strategies, with only meager returns to show for it.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

The reopening of the economy in 2022 was a big boost for most industries, helping post new highs in revenues and profits since the pandemic. However, the home improvement sector saw customer volume and demand decline in 2022.

The lower profitability is not that surprising. If you recall, the industry benefited the most from travel restrictions and lockdowns in the first half of the pandemic.

Since people were confined to their homes, they had to get creative about how they were going to spend their leisure time. Passing the time in malls or going on trips was out of the question.

As a result, a noticeable portion of consumers’ expenses shifted to fixing and improving their homes. This benefitted the home improvement industry, which adapted to digital platforms to further boost product accessibility.

AllHome Corp. (HOME:PHL), for example, was able to take advantage of this surge, posting net profits of PHP 988 million and PHP 1.44 billion in 2020 and 2021, respectively.

However, once pandemic restrictions began to ease in 2022, the home improvement industry saw a substantial decline in demand. Consumers now shifted their spending habits toward travel and entertainment, reversing the trend that was previously in the home improvement industry’s favor back in 2020 and 2021.

AllHome saw net profits fall by 35% in 2022. To make things worse, one of the company’s store outlets in Alabang was damaged by fire. This led to AllHome needing to write off more than PHP 300 million worth of equipment and inventory.

Despite the challenges that AllHome faced in 2022, the company continued to look for opportunities to expand its market reach, knowing that the low demand in the home improvement industry was only going to be temporary.

AllHome reached a total of 60 stores in 2022, a net increase of 3 stores, with the most significant recent addition located in Davao City. Chairman Manuel B. Villar, Jr. expressed his confidence that the company will reach a total of 100 stores by 2026, signaling the company’s priority to improve market reach through store expansion.

Furthermore, AllHome ventured into the pet care business in 2022, opening five PetBuddy stores. With pets being a crucial part of maintaining a home for many households, AllHome’s product expansion aims to provide its customers with a wide selection of pet products and services such as day care and grooming.

AllHome’s earning power is stronger than you think

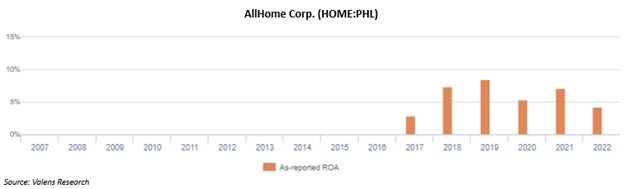

As-reported metrics still seem to understate AllHome’s expansion initiatives and distort the true reflection of the company’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

In reality, the company’s growth initiatives actually resulted in the company doing much better than expected, with Uniform ROAs reaching 6%.

One of the said distortions stems from how Philippine Financial Reporting Standards (PFRS) classify interest expense.

According to PFRS, interest expense can be classified as an operating cash flow. In reality, interest expense represents the cost of debt and is rightfully only a financing cash flow. As such, in Uniform Accounting, interest expense is added back to earnings.

As a firm that made a lot of investments through debt, AllHome recognized interest expense from its debt.

Specifically, in 2022, it recorded a PHP 404.9 million interest cost. Adding back this expense because it is not an operating expense, with many other necessary adjustments made by Valens, leads to a PHP 1.38 billion net income and 6% Uniform ROA, higher than the PHP 933.8 million as-reported net income and 4% as-reported ROA.

Through Uniform Accounting, we can see that the company’s true ROAs have been understated each year since the company was publicly listed. For example, as-reported ROA was 4% in 2022, but its Uniform ROA was actually higher at 6%.

AllHome has a more efficient business than you think

Trends in Uniform ROA have been driven by trends in Uniform asset turns. Since its IPO, as-reported metrics have been understating AllHome’s asset efficiency, a key driver of returns. For example, the company’s Uniform turns are at 0.6x in 2022, not just 0.5x.

SUMMARY and AllHome Corp. Tearsheet

As our Uniform Accounting tearsheet for AllHome Corp.(HOME:PHL) highlights, the company trades at a Uniform P/E of 11.7x, below the global corporate average of 18.4x, and its historical P/E of 19.7x.

Low P/Es require low EPS growth to sustain them. In the case of AllHome, the company has recently shown a 35% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, AllHome’s sell-side analyst-driven forecast is to see a Uniform earnings growth of 28% through 2024.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify AllHome’s PHP 1.63 stock price. These are often referred to as market-embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 11% annually over the next three years. What sell-side analysts expect for AllHome’s earnings growth is above what the current stock market valuation requires through 2024.

Moreover, the company’s earning power is in line with the long-run corporate averages. However, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals high dividend risk.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com