Going cashless might be this company’s leverage to push Uniform ROAs past 70%+ going forward

Globally, there was a time when cash was the preferred mode of payment for most people. However, as technology advanced, consumer behavior has shifted to a point where cashless payments are slowly taking over mainly for convenience reasons.

With the pandemic sparking concerns over the coronavirus being spread when cash is exchanged, the digitization of payments will likely accelerate. This company is riding that momentum by continuing to expand its portfolio of non-cash payment options.

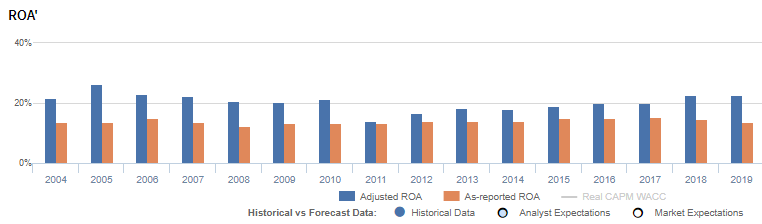

However, while as-reported metrics signal that these investments are not generating returns, TRUE UAFRS-based (Uniform) analysis shows that return on assets (ROA) have actually stayed more than 50% in recent years.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Consumer spending habits have shifted dramatically over the past few months as people continue to weather through the pandemic. Much of the spending was reallocated from physical retail stores to e-commerce.

The public has turned to online retailers to make their essential purchases—and some non-essentials like streaming or gaming subscriptions—while following social distancing rules and minimizing in-person transactions of goods and payments.

On the other hand, spending on airlines, hotels, dine-in restaurants, and other non-essential goods has plunged, with everyone having been told to stay home.

Fortunately, for digital payment companies like Mastercard (MA), Paypal (PYPL), and Visa (V), their exposure in the e-commerce space has given them some form of buffer against the decline in retail spending.

However, although e-commerce has been positively affected by the surge in demand, it was more than offset by a general decrease in consumer spending.

Visa, in particular, has felt the effects of the disruptions and announced a drop in the volume of payments and revenues for the next quarter. However, while these headwinds pull the company’s returns down in the short term, they’re actually positioned to fundamentally grow stronger in the long term.

As one of the leaders of the payments space, Visa’s vast network of merchants that accept their cards and the growing number of cashless payments provide them with an economic moat to grow their returns.

In March, the company’s contactless payments usage for the U.S. is up by 150% from the same period last year. This shows how cashless transactions have been slowly taking over the way people deal with their payments.

Furthermore, other countries across the globe have made the switch towards being a cashless society.

More than 75% of consumers in China have opted to go digital through QR code payments since 2017. In Sweden, cash transactions account for only 2% of the country’s total transactions in recent years. In the UK, the number of ATMs have declined as cash transactions are now done digitally.

Meanwhile, in the Philippines, Visa is continuing their efforts to increase digital payments usage by partnering with local banks and stores to widen merchant acceptance for cashless payments. According to the company, these efforts have yielded double-digit growth in terms of overall spending in recent years and is expected to continue going forward.

As the digitization of payments continues to accelerate, Visa is taking advantage of the momentum by acquiring fintech companies to enhance its portfolio offerings and complement existing revenue sources.

Three notable acquisitions were Earthport (May 2019), Payworks (July 2019), and Verifi (September 2019).

- Earthport strengthened the company’s international payment capabilities with its automated clearing capabilities with transaction fees that were about 90% than traditional wire transfers

- Payworks provided payment service providers with multiple additional channels to accept payments in

- Verifi enhanced the company’s risk and fraud management solutions

Visa’s product portfolio expansion through these acquisitions has had a considerable positive impact on the company’s revenues. However, as-reported metrics don’t quite reflect that.

As-reported ROAs are shown to be stable at around 12%-15% in the past eight years when in fact, the company’s profitability is much stronger with Uniform ROAs staying at more than 50% levels.

The distortion comes from as-reported metrics failing to consider the amount of goodwill on Visa’s balance sheet, which is substantial given their many acquisitions in the past.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Visa’s earning power. Once you adjust for goodwill, you will get returns that are actually 5x-6x greater. Without this adjustment, it will look like Visa’s acquisitions have not been creating value for the firm.

Visa’s plans to sustain its robust profitability levels are evident in its product expansion strategy through its recent acquisition of Plaid—a platform that allows applications to access consumers’ financial data.

Plaid’s customers include peer-to-peer payment app Venmo, mobile stock trading app Robinhood, and cryptocurrency exchanges Coinbase and Gemini. This means that Visa now has connections to a wider base of the financial system, giving the company greater leverage across new transaction types and new users of credit.

Visa can now push into new avenues of growth such as business-to-business payments while having the capability to build out their non-card offerings.

These tailwinds, combined with the acceleration of cashless payments, point to the potential for a significant positive improvement for the company going forward, likely driving long-term profitability growth.

Visa’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Uniform ROA has been higher than as-reported ROA in the past sixteen years. For example, as-reported ROA for Visa was 14% in 2019, which is materially lower than its Uniform ROA of 65%.

Visa’s Uniform ROA has ranged from 19% to 89% over the past sixteen years. From a historical high of 89% in 2004, Uniform ROA fell to 19% in 2008. It then recovered to 69% to 71% levels in 2012 to 2014, before declining to 50% in 2017. Finally, it bounced back to 65% levels in 2019.

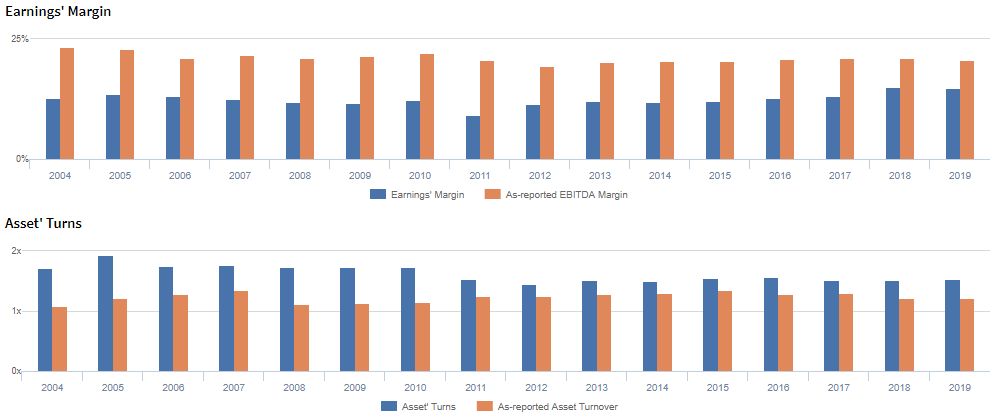

Visa’s Uniform ROA is driven by significantly more robust Uniform asset turns but is slightly offset by Uniform earnings margins

Trends in Visa’s Uniform ROA have largely been driven by trends in Uniform earnings margins and Uniform asset turns.

From 2005-2007, Uniform earnings margins sharply declined from 40% to 15%. It recovered to 38% levels in 2010, and further increased to a peak of 55% in 2019. Meanwhile, Uniform asset turns fell from a peak of 2.9x in 2006 to 0.8x in 2008. It then improved to 1.6x in 2013, before declining to 1.2x levels in 2019.

At current valuations, markets are pricing in expectations for Uniform earnings margins and Uniform asset turns to modestly improve from current levels.

SUMMARY and Visa Tearsheet

As the Uniform Accounting tearsheet for Visa Inc. (V) highlights, the Uniform P/E trades at 33.6x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Visa, the company has recently shown a 30% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Visa’s Wall Street analyst-driven forecast is an 8% shrinkage in 2020, and a 17% growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Visa’s $176 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 14% each year over the next three years. What Wall Street analysts expect for Visa’s earnings growth is below what the current stock market valuation requires in 2020 but is above that requirement in 2021.

The company’s earning power is 11x the corporate average. Also, cash flows are 5x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Visa’s Uniform earnings growth is in line with peer averages in 2020. Also, the company is trading in line with average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com