Growth and survival have been this retail company’s motto since the beginning, reaching a Uniform ROA of 18%, not 6%

This hypermarket company was able to withstand the severe effects of the pandemic through its growth initiatives. However, as reported data doesn’t believe that this is the case.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

The Philippine economy is beginning its recovery, albeit slow, two years after the pandemic began. A big contributor to this is the easing of restrictions and the opening up of the country once again.

One industry that benefited from this improvement is the retail hypermarket industry. In the Philippines, the second leading hypermarket is Puregold Price Club, Inc. (PGOLD:PHL), with SM Investments Co. being its biggest rival in the industry.

Puregold’s strategic method of retailing involves offering a variety of high-quality items at a cheaper cost. It targets the growing middle class and the young population through its one-stop shopping philosophy to consumers.

Despite the challenges brought by the pandemic, the company was able to improve its sales from PHP 38.5 billion in 2021 to PHP 43.7 billion in 2022.

This was mainly due to Puregold’s strategic growth initiatives, specifically store expansion, shopper count increases, demand creation, and robust end-to-end supply chain. Currently, Puregold has 513 stores nationwide and has opened 15 additional new stores in Metro Manila, North Luzon, South Luzon, and Visayas.

The company continues to focus on investing in various marketing vehicles to leverage its social media and business capabilities. Specifically, Puregold is doing this by strengthening its digital impact through shopping ally “Sally,” Aling Puring App, and Aggregators.

The company even pioneered “retailtainment,” as it aimed to maximize social media users to connect and interact with consumers wherever they are. This is made through the Puregold Channel, where several contents regarding branded messaging, sales offers, and frictionless transactions are offered.

With all these continuous efforts and growth, Puregold remains competitive and relevant in the Philippine retail industry.

However, looking at as-reported metrics, it appears that the company’s returns continue to decline and produce barely cost-of-capital levels, with return on assets (ROAs) reaching only 6% in 2021.

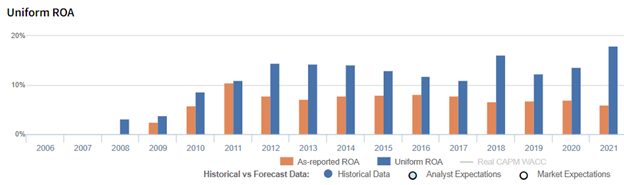

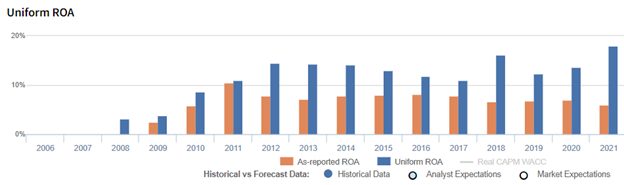

In reality, Uniform Accounting tells us that this is a misrepresentation of Puregold’s profitability. In fact, the company’s Uniform ROA is far more robust than what the as-reported figures show.

What as-reported metrics fail to do is consider the company’s excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

When excess cash remains included in the company’s asset base in computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

For 2021, Puregold had a significant amount of excess cash sitting idly in its balance sheet for up to 24% of its as-reported total assets.

Puregold’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that Puregold’s profitability has been recently weaker than real economic metrics highlight.

Through Uniform Accounting, we can see that the company’s true ROAs have been understated over the past decade. For example, as-reported ROA was 6% in 2021, but its Uniform ROA was 3x higher at 18%.

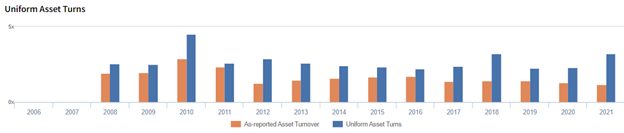

Puregold’s asset turns are more efficient than you think

For nearly two decades, as-reported metrics have understated Puregold’s asset turns, a key driver of profitability.

Moreover, Uniform turns have already reached 4.5x. In comparison, as-reported turns have yet to eclipse beyond 2.9x. over the same time period, making the company appear to be a less efficient business than real economic metrics highlight.

SUMMARY and Puregold Price Club, Inc. Tearsheet

As our Uniform Accounting tearsheet for Puregold Price Club, Inc. (PGOLD:PHL) highlights, the company trades at a Uniform P/E of 8.7x, below the global corporate average of 18.4x and its historical P/E of 12.3x.

Low P/Es require low EPS growth to sustain them. In the case of Puregold, the company has recently shown an 18% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Puregold’s sell-side analyst-driven forecast is to see Uniform earnings shrinkage of 17% and 8% growth through 2023.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Puregold’s PHP 33.25 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 23% annually over the next three years. What sell-side analysts expect for Puregolds earnings growth is above what the current stock market valuation requires through 2023.

Moreover, the company’s earning power is 3x the long-run corporate average. Also, cash flows and cash on hand are 5x total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Puregold’s Uniform earnings growth is below its peer averages, and also below its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com