Improving the innovation process by fusing creativity with efficiency helped this multi-billion company maintain robust Uniform ROAs of 20%+

Brand acquisition is a common strategy for firms looking to expand their product portfolio. When this company became global, it used this acquisition strategy to create a portfolio of diverse, profitable brands.

Eventually, when profitability plateaued, the company decided to divest its underperforming businesses and focus more on the innovation of its core products as an avenue for growth.

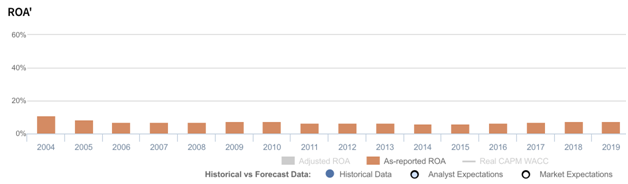

As-reported metrics suggest that the company’s innovation efforts were a waste, with ROAs declining consistently since 2004. However, Uniform Accounting shows that its product innovations have enabled the company to tap into new markets and reinforce the strength of its brands, helping maintain robust Uniform ROAs of 20%+.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

In 1837, a candlemaker and a soap maker, with the advice from their father-in-law, created a joint venture that is now known as Procter & Gamble (PG).

The venture initially supplied candles and soap to the army before entering the consumer market with their first product, Ivory soap. Demand grew fast, and eventually, the business partners took the firm global.

To increase scale, P&G diversified its portfolio with products ranging from toothpastes, laundry detergents, and toilet paper, among other things. Over time, these products became highly-profitable household names.

The company had grown so much to the point that its growth rate began to plateau. Its revenues and margins had also begun to soften. To address this concern, P&G decided to move away from a brand portfolio expansion strategy to focus more on their core brands.

In 2014, the company announced a plan to divest about 100 of its underperforming businesses. This included the divestiture of Duracell to Berkshire Hathaway, two of its soap brands to Unilever, and 43 of its beauty brands to Coty.

This left P&G with a smaller portfolio of well-known consumer brands such as Tide, Pampers, Safeguard, and Gillette.

While the portfolio’s brand identities were strong, what really sustained the company’s growth was its commitment to innovation, as inspired by the assembly line concept of Thomas Edison and Henry Ford. This was the idea of mass production that combined speed, efficiency, and reliability—or what was called a “new-growth factory.”

P&G used the tenets of creativity and efficiency of the new-growth factory concept to create assembly lines, not for physical products, but for innovations. In that sense, the company was systematizing the innovation process, moving from generating raw ideas to creating innovative and profitable products.

To do this, P&G targeted several innovation points. First, improving on existing products through innovation, which the company applied to Gillette.

Shaving is supposed to be a simple task—you pick up a razor, any razor, and you start shaving. This was true for much of Gillette’s early years. But now, the brand has over 20 types of razors each serving a different purpose and targeting a specific market.

There are ones for men and women, and people with sensitive skin. There are disposable ones, ones with two blades and ones with three blades, and ones that can pivot for a shave that’s easier to navigate.

Gillette has been able to dominate the razor market by bringing innovation to its products. So, although any razor would get the shaving job done, the brand is able to increase market share by marketing quality over simplicity.

The next target point centered around transformative innovation through performance breakthroughs, as is the case with Olay.

Olay had already established itself as a trusted skincare brand for women. This comes as no surprise because the products go through multiple rigorous clinical trials and are tested with thousands of women annually.

Olay took it up a notch with their ProX series, which are essentially the same products, but marketed as being dermatologically-designed, not just dermatologically-tested. This performance-enhancing innovation allowed P&G to target more of the affluent consumers with their higher-quality products.

The last point, disruptive innovation, enabled the company to drive growth through the adoption and creation of trends. Several of P&G’s brands followed a disruptive path, two of which, Tide and Crest, were notable.

Crest used to dominate the toothpaste market in the 1990s before Colgate took the lead. To recapture market share, Crest disrupted the market by introducing Crest Whitestrips, making teeth whitening easier and more affordable. It then followed up with other advanced teeth whitening products that appealed to previous consumers as well as new ones.

Tide followed a similar path with Tide To Go, a portable detergent stick that easily removes small stains without the need for actual laundry. This targeted the company’s general consumer base and opened up a new market for on-the-go dry cleaning.

With these extensive innovation efforts strengthening P&G’s brands further while capturing new markets as avenues for growth, it is expected that ROAs would at least sustain its strength.

However, as-reported data make it appear that their innovation strategies have been unsuccessful, and even detrimental to returns, with as-reported ROAs falling from 11% in 2004 to 8% in 2019.

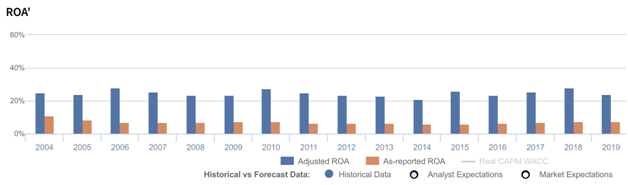

In reality, Uniform Accounting paints a significantly different picture. Uniform ROAs over the past sixteen years have actually maintained robust 20%+ levels.

The distortion comes from as-reported metrics failing to consider the amount of accumulated goodwill on P&G’s balance sheet, which is about $40 billion in recent years, from their acquisitions in recent years as well as during the early years of their expansion strategy.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of P&G’s earning power. Adjusting for goodwill, which historically has been about a third of its assets, returns are actually 3x-4x greater.

P&G’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

P&G’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA was 8% in 2019, but its Uniform ROA was actually over 3x higher at 24%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been much higher. P&G’s Uniform ROA has ranged from 21% to 28% in the past sixteen years while as-reported ROA ranged only from 6% to 11% in the same time frame.

After rising to 28% in 2006, Uniform ROA declined to 23% in 2009 before expanding back to 28% in 2010. Then, it gradually compressed to 21% in 2014 and subsequently rose to 24% in 2019.

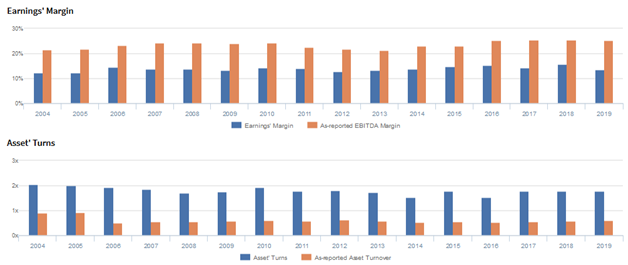

P&G’s Uniform earnings margins are weaker than you think, but its robust Uniform asset turns make up for it

P&G’s stable profitability has been driven by offsetting trends in Uniform earnings margins and Uniform asset turns.

From 2004-2006, Uniform earnings margins improved from 12% to 15%, before stabilizing to 13%-14% levels through 2014 and expanding to 15% levels in 2015-2016. It then compressed back to 14% in 2019.

Meanwhile, Uniform turns gradually declined from 2.1x in 2004 to 1.7x in 2008, before expanding to 1.9x in 2010. It then compressed to 1.5x in 2014, before recovering to 1.8x in 2019.

At current valuations, markets are pricing in an expectation for Uniform margins and Uniform turns to expand to new highs.

SUMMARY and P&G Tearsheet

As the Uniform Accounting tearsheet for the Procter & Gamble Company (PG) highlights, the Uniform P/E trades at 26.4x, which is above corporate average valuation levels, but around its own recent history.

High P/Es require high EPS growth to sustain them. In the case of P&G, the company has recently shown a 9% Uniform EPS contraction.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, P&G’s Wall Street analyst-driven forecast is a 41% and 2% EPS growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify P&G’s $126 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow by 13% each year over the next three years to justify current prices. What Wall Street analysts expect for P&G’s earnings growth is above what the current stock market valuation requires in 2020, but below its requirement in 2021.

Furthermore, the company’s earning power is 4x the corporate average. Also, cash flows are 2x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, P&G’s Uniform earnings growth is the highest among peer averages, but the company is trading in line with average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com