Its strong brand recognition helped this food and beverage company secure its spotlight, producing a Uniform ROA of 12%, not 8%

With so many companies today, only a handful of them provide brands and products that become commonplace in our lives.

Specifically, in the local food and beverages scene, this particular subsidiary has succeeded in making itself a household name through ordinary products that later prove nearly irreplaceable to the Filipino lifestyle.

However, as-reported metrics give the company less credit than it deserves, understating its return on assets at 8%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

There are only a handful of companies that are titleholders of impressive brand recognition. In the local setting, just as brandy is Emperador, beer is San Miguel.

The local alcoholic beverages market is dominated primarily by these two conglomerates, with San Miguel being the largest beer producer in terms of both domestic sales and volumes.

However, the popularity of these products alone is not enough to ensure the company’s profitability amid market downtrends.

In fact, much of the success of San Miguel Food and Beverage Inc. (SMFB) is not solely attributed to its beverage business, San Miguel Brewery Inc. (SMB).

SMFB owes much of its success to its food subsidiary, San Miguel Foods (SMF), which has garnered various strategic brand acquisitions throughout the years—such as Pure Foods, Spam, Magnolia, and Monterey among others.

Amidst the global pandemic, these packaged food brands managed to further increase SMF’s sales due to stable pricing, doubling its net income during the first quarter of 2021.

On the other hand, SMB was not as lucky. Alcohol bans during the government-imposed community quarantines resulted in weaker beer sales. Not only that, SMB’s volumes have been relatively lower than in previous years due to major distribution channels being closed, resulting in revenues only improving by a mere 2%.

Despite SMB’s slower growth, SMFB was able to increase its consolidated net income by 137% from PHP 7.34 billion in H1 2020 to a whopping PHP 17.36 billion in H1 2021.

This comes after the company launched relevant initiatives to combat the adverse effects of the pandemic, which includes the improvement of the SMC Hub, allowing customers to purchase favored items through a seamless online transaction process.

On top of that, SMFB plans to allot PHP 30 billion for capital expenditures to pursue capacity expansion.

This expansion is aimed at building more processed meat canneries, butter and cheese plants, feed mills, poultry processing plants, and warehouses to store additional products.

The strength of its brands along with various strategic initiatives synergizes the performance of this business. However, as-reported metrics had been giving the company less credit than it deserves, understating its profitability at 8%.

In reality, SMFB’s business strategies delivered better results for the company, with its Uniform ROA still reaching 12% despite the negative effects of the pandemic.

For this company, the largest accounting distortion has been the treatment of minority interest expenses. With the firm also having its own set of subsidiaries, each subsidiary has investors that possess non-controlling stakes.

According to the Philippine Financial Reporting Standards (PFRS), the profits attributable to minority shareholders can be recognized under operating cash flow, leading people to think that it is essential to the firm’s core operations.

In reality, it should always be classified as a financing cash flow. Minority shareholders have provided capital to the subsidiaries in exchange for a piece of the company’s earnings. As a result, minority interest expense should not be subtracted from SMFB’s revenues when calculating its real core earnings.

In 2020, SMFB recognized PHP 10.0 billion in minority interest expense, resulting in a PHP 12.5 billion net profit and an 8% as-reported ROA. By adding the expense back alongside the other adjustments Valens makes, the company should actually be recognizing PHP 22.4 billion in earnings and a 12% Uniform earning power.

San Miguel Food and Beverage’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

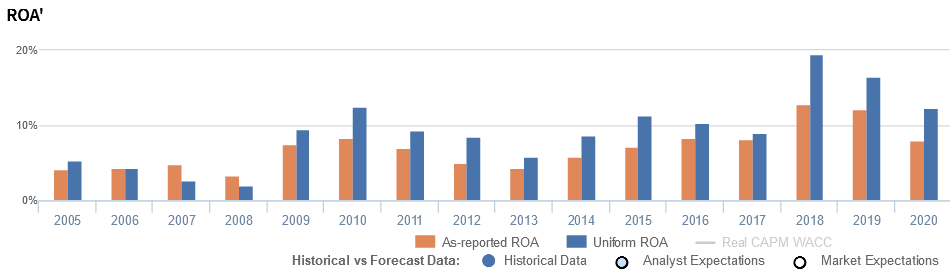

SMFB’s Uniform ROA has actually been significantly higher than its as-reported ROA since consolidating its food and beverage businesses in 2018. For example, as-reported ROA was 12% in 2019, but its Uniform ROA was stronger at 17%.

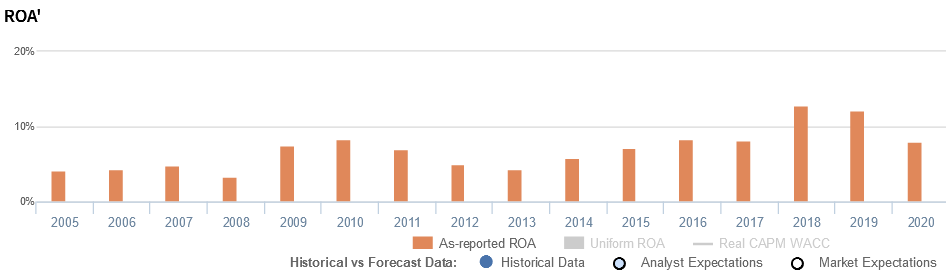

Historically, as-reported ROA has improved from 3%-4% levels in 2005-2008 to 13% in 2010, before compressing to 4% in 2013 and jumping to a high of 13% in 2018. Since then, as-reported ROA declined to 8% in 2020.

Meanwhile, after fading from 5% in 2005 to a low of 2% in 2008, Uniform ROA soared to 13% in 2010 and fell back to 6% in 2013. Thereafter, Uniform ROA recovered to 11% in 2015, before compressing to 9% in 2017 and subsequently rebounding to a peak of 20% in 2018. Since then, Uniform ROA declined to 12% in 2020.

San Miguel Food and Beverage is more efficient with its assets than you think

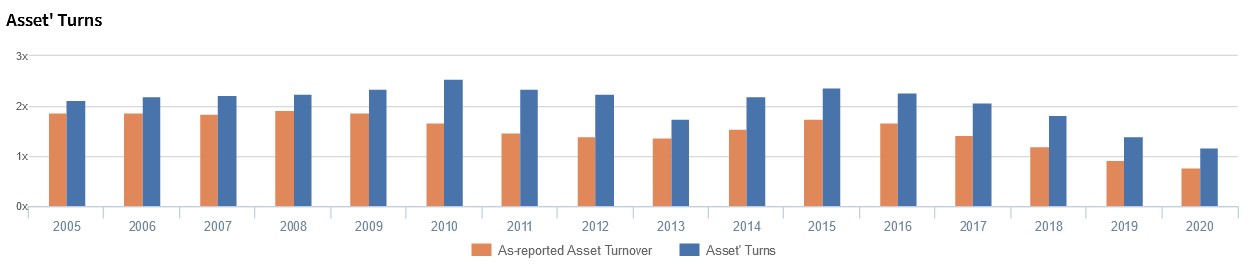

Overall strength in Uniform ROA has been driven by strength in Uniform asset turns. Since 2005, as-reported metrics have understated SMFB’s asset utilization, a key driver of profitability.

Uniform turns improved from 2.1x in 2005 to a high of 2.6x in 2010, before contracting to 1.7x in 2013. Then, Uniform turns improved to 2.4x in 2015, before receding to 1.2x in 2020.

Meanwhile, from 2005-2009, as-reported asset turnover sustained 1.9x levels, before compressing to 1.4x levels in 2012-2013. Subsequently, as-reported asset turnover recovered back to 1.8x in 2015, before declining again to 0.8x in 2020.

As-reported metrics have been making SFMB appear to be a far less asset-efficient business than real economic metrics highlight.

SUMMARY and San Miguel Food and Beverage, Inc. Tearsheet

As our Uniform Accounting tearsheet for San Miguel Food and Beverage, Inc. (FB:PHL) highlights, the company trades at a Uniform P/E of 15.3x, below global corporate average of 24.0x and its historical P/E of 19.5x.

Low P/Es require low EPS growth to sustain them. In the case of SFMB, the company has recently shown a 26% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, SFMB’s sell-side analyst-driven forecast is to see Uniform earnings grow by 96% and 13% by 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify SFMB’s PHP 75.80 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 3% annually over the next three years. What sell-side analysts expect for SFMB’s earnings growth is well above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 2x the long-run corporate average. Furthermore, cash flows and cash on hand are also 2x total obligations—including debt maturities, capex maintenance, and dividends. Also, intrinsic credit risk is 140bps above the risk-free rate. Together, this signals a low dividend but moderate credit risk.

Lastly, SFMB’s Uniform earnings growth is above its peer averages, but currently trades below its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com