Listen to music on the spot. This company created a platform that revolutionized digital music streaming and realized Uniform returns of 20%+

A “freemium” model works well for companies who are looking to increase their user base with the expectation that these users would get enough firsthand experience to upgrade to the premium product.

This music streaming company uses this model, but instead of relying solely on revenues from premium subscriptions, it is also able to monetize the free version of its service through ads.

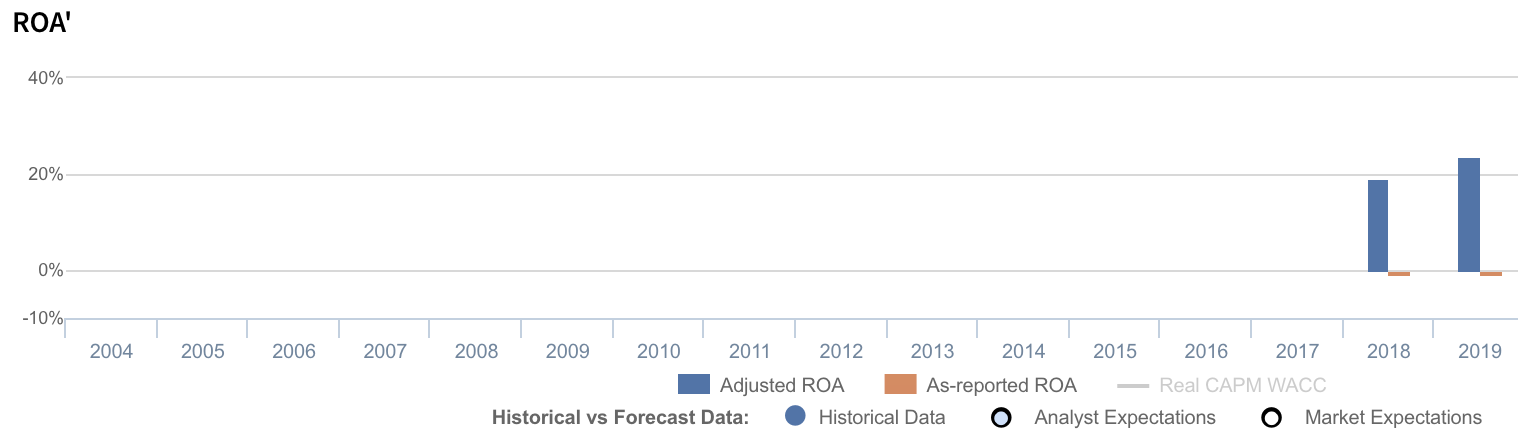

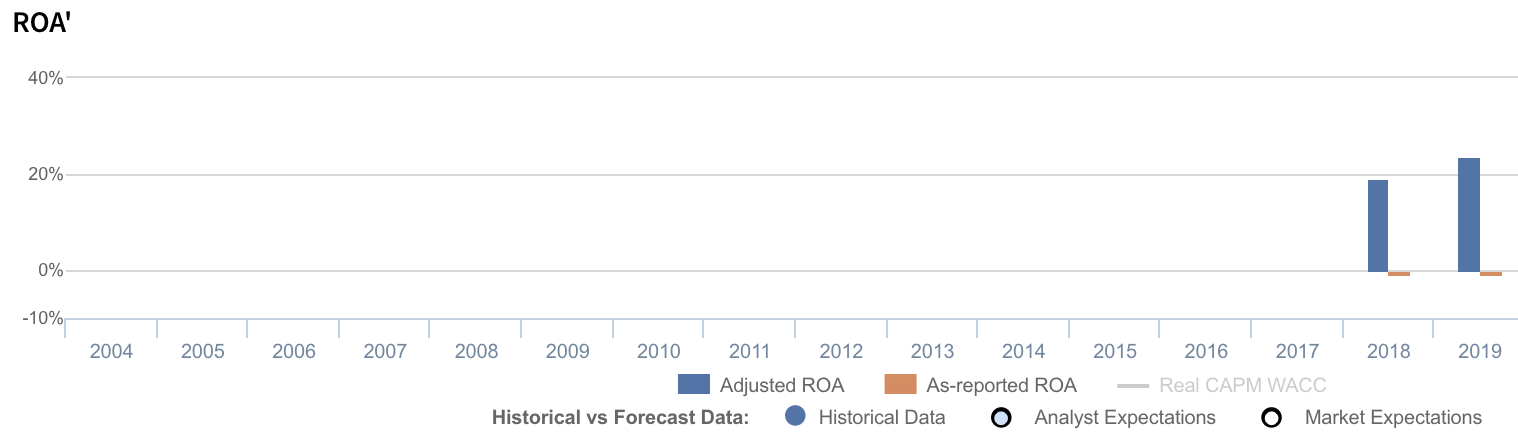

While as-reported metrics make it appear that this company’s ability to monetize both the free and premium versions of its product has not yet resulted in profits, Uniform Accounting shows that returns have actually been positive and are 5x the cost-of-capital levels, with Uniform ROAs at around 20%.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Before the era of digital streaming, listening to music on demand came in the form of cassette tapes or CDs. People would often carry around walkmans and CD players, and you’d have to manually switch from one album to another if you wanted to listen to other artists.

Now, listening to music has become a lot easier thanks to the internet. Gone are the days of limited music libraries and physically browsing through CD collections.

The digitization of music was popularized by Apple when it came out with the iPod and its online mp3 marketplace, iTunes. But while Apple’s iPod revolutionized where and how we listened to music, entrepreneurs Daniel Ek and Martin Lorentzon heavily disrupted iTunes and revolutionized where we get the music.

They developed the idea for a new music streaming platform, Spotify (SPOT), that would legally deliver music instantly to its users without the need to pay $0.99 per song (as in the case of iTunes) or having it illegally downloaded from file sharing sites.

Initially, free accounts were available only by invite, but paid subscriptions were open to everyone. Eventually, Spotify opened the platform for free public registration to the UK, the US, then to the rest of the world.

Users signed up because they realized how much more convenient streaming music is.

It’s free and requires no commitment, which makes it an easy decision to sign up. Plus, subscribers always have the option to upgrade to the premium version if their experience was satisfactory.

This “freemium” model, which we’ve talked about with Atlassian, is used by Spotify to attract a wider base of users who will hopefully get enough firsthand experience to upgrade to the premium product.

What Spotify does differently, other than using the “freemium” strategy to get users to upgrade, is to monetize the free version of the app through ads.

Free-version users of the service are targeted with audio advertisements in between songs that encourage them to upgrade to the premium version of Spotify. These users are then more likely to purchase the premium version to remove repetitive ads and gain unlimited use of the ‘skip’ button.

To retain those who have upgraded to the premium version, Spotify continuously develops new product features to make the platform even more engaging for users.

Using algorithms, it started introducing curated playlists and personalized recommendations. One of the more popular features is the “Discover Weekly” feature, which attracted 40 million new users to the platform, with more than 5 billion tracks streamed.

Spotify’s personalized user experience and better discovery features differentiate itself from competitors such as Apple Music or Tidal, enabling the company to dominate the music streaming space with a market share of ~35%.

However, looking at as-reported financials, it would appear that being a top-tier business with the ability to monetize all versions of its platform has not resulted in profits for Spotify. In fact, the company has had flat negative return on assets (ROA) historically.

In reality, Uniform Accounting tells us that not only are returns 5x the cost of capital, they have actually improved year-over-year.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics incorrectly treating R&D as an expense.

R&D is an investment in the long-term cash flow generation of the company. By recording R&D as an expense, this violates one of the core principles of accounting, which is that expenses should be recognized in the period when the related revenue is incurred.

Since as-reported accounting records R&D on the income statement, as opposed to as an investment on the balance sheet, net income can become materially understated.

Spotify materially spends on R&D to drive user engagement and innovate its advertising products. The company’s R&D spend has consistently been about 30% of total operating costs, or about $500 million annually in recent years.

After adjustments, we can see that Spotify’s Uniform ROA is at 19%-24% levels, which is materially higher than its as-reported ROA of negative levels. Without this adjustment, it will look like the firm is having less success with its R&D investments than it really is, leading to poorer valuations.

Spotify’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Spotify’s Uniform ROA has actually been higher than its as-reported ROA since its IPO in 2018. For example, as-reported ROA was -1% in 2019, but its Uniform ROA was actually materially higher at 24%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been positive. Spotify’s Uniform ROA has ranged from 19% to 24% in the past two years while as-reported ROAs remained in the negatives over the same timeframe.

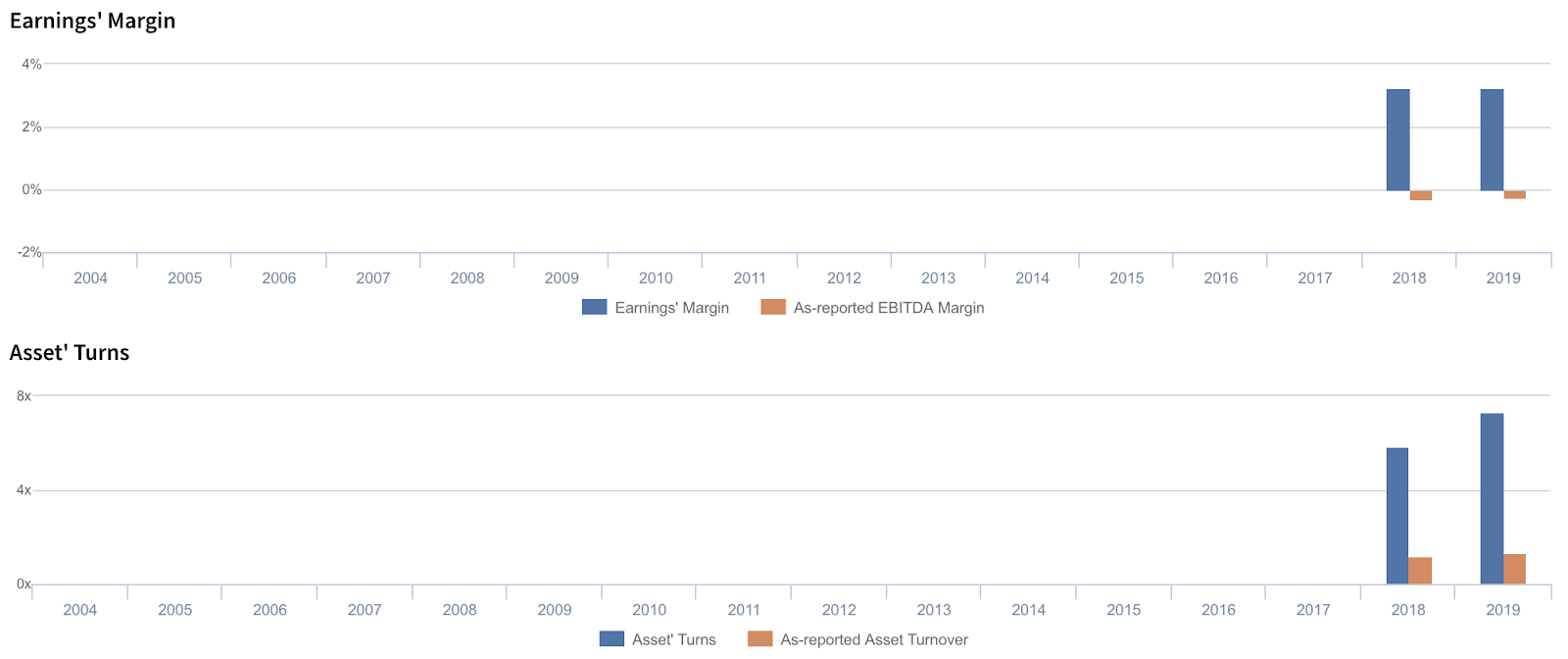

Spotify’s Uniform asset turns are driving its robust ROAs

Spotify’s strong profitability has been driven largely by trends in both Uniform asset turns, and to a much lesser extent, Uniform earnings margins.

Uniform earnings margins have been stable over the last two years, remaining at 3% levels. On the other hand, Uniform turns have improved greatly, improving from 5.9x in 2018 to 7.4x in 2019.

At current valuations, markets are pricing in an expectation for Uniform margins and Uniform turns to expand to new highs.

SUMMARY and Spotify Tearsheet

As the Uniform Accounting tearsheet for Spotify Technology S.A. (SPOT) highlights, the Uniform P/E trades at 135.1x, which is above corporate average valuation levels and its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Spotify, the company has recently shown a 5% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Spotify’s Wall Street analyst-driven forecast is a 40% Uniform EPS shrinkage in 2020 followed by a 167% growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Spotify’s $269 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 36% each year over the next three years to justify current prices. What Wall Street analysts expect for Spotify’s earnings growth is below what the current stock market valuation requires in 2020, but above its requirement in 2021.

Furthermore, the company’s earning power is 4x the corporate average. Also, cash flows are 3.5x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Spotify’s Uniform earnings growth is above its peer averages in 2020. Therefore, as is warranted, the company is trading above average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com