Low-cost fees and a “fitness for everyone” brand works out well for this gym franchisor, helping it gain Uniform ROAs of 50%+

Gyms can be an intimidating and often costly place for beginners who want to start living healthier lifestyles. However, this company completely bucks that reputation.

With its “Judgment Free Zones” and low-cost membership fees, this company was able to grow its customer base and market share. Plus, using a franchising model, it was also able to expand its locations without having to shell out massive capital.

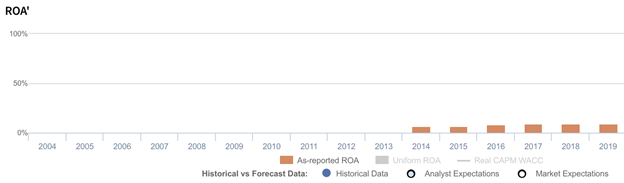

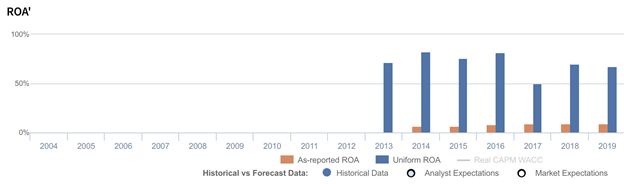

Looking at as-reported metrics, one would be confused as to how a company with an impressive national footprint is only earning below 10% returns. However, Uniform Accounting reveals that returns have actually been at far more robust 50%-80% levels.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

The only times you would hear “free food” and “gym” together in a sentence is if that sentence started with the words “there is no.” But if you were a member at Planet Fitness (PLNT), you know that that’s not always the case.

In 1999, one of the gym’s branches in New Hampshire didn’t have hot running water for a few days. As a way to make up to members who showed up despite being unable to take hot showers after, the owners ordered pizzas and gave everyone a slice.

The gesture was so well-received that it eventually became tradition—on the first Monday of each month, branches from across the country would give out free pizzas to all members present.

The popularity of Pizza Mondays gave rise to another tradition, Bagel Tuesdays, which occurs on the second Tuesday of the month. Although giving out free food might seem counterintuitive, it’s actually part of why its members continue to be members—to be part of a community.

Specifically, its brand revolves around a simple concept: providing fitness for everyone. All of its branches nationwide are labeled as Judgment Free Zones, where fitness junkies and beginners alike can feel like they belong.

What’s even better is that because Planet Fitness takes out non-essential amenities like pools or group classes, it has the lowest gym membership fees out of its competition. Rates start at $10 per month, as opposed to rival Anytime Fitness’ $30 per month rate or luxury fitness club Equinox’s rate that goes up as high as $500 per month.

Low-cost subscription fees enable the company to earn steady, recurring revenues. Plus, given that the fees are relatively immaterial, there is a lower probability that a member would cancel, providing even less revenue volatility.

Planet Fitness’ inclusive branding and highly accessible fees have led to success in pulling in the occasional gym-goer, as well as those who find the traditional gym setting too intimidating. Overall, the company holds about 20% of the market share for U.S. gym memberships.

Moreover, not only does its branding and accessibility work well in building its customer base, it is also a perfect complement for its franchising model.

Planet Fitness licenses the use of its brand to a third party, who then sets up operations under that brand in exchange for a fee. So, aside from membership fees earned from corporate-owned gyms, a massive chunk of the company’s revenues also comes from royalty fees from its franchise-owned gyms.

A franchising model benefits both the franchisee and franchisor in different ways.

Franchising makes it easier for franchisees to enter into highly competitive markets—like gyms—by making use of an already known brand with an established customer base. In that sense, the franchisee doesn’t have to spend as much on marketing and advertising as they would have to promote a new business.

If you recall, this franchising strategy is how major hotel brand Marriott (MAR) was able to aggressively expand and still maintain high profitability.

As for Planet Fitness, the company is able to expand its asset base without having to spend massively on capital investments. Consequently, this makes for operations with lower fixed costs and steady profits.

Looking at as-reported metrics, investors would be confused at how an asset-light business with an impressive national footprint is only earning sub-10% return on assets (ROAs).

However, with Uniform ROAs that are much more robust at 50%-82% since 2013, Uniform Accounting confirms expectations that franchising businesses are phenomenally profitable.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on Planet Fitness’ balance sheet. In recent years, goodwill sits at about $200 million to $220 million, making it the firm’s third largest long-term asset, arising from the reacquisition of franchising rights from franchisees.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Planet Fitness’ earning power. Adjusting for goodwill, we can see that the company isn’t actually performing poorly. In fact, it has been the opposite, with returns that are nearly 6x-12x greater.

Planet Fitness’ earning power is actually significantly more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

Planet Fitness’ Uniform ROA has actually been higher than its as-reported ROA in the past seven years. For example, as-reported ROA was 10% in 2019, but its Uniform ROA was actually nearly 7x higher at 68%.

Specifically, Planet Fitness’ Uniform ROA has ranged from 50% to 82% in the past seven years, while as-reported ROA ranged only from 7% to 10% in the same timeframe. Uniform ROA rose from 72% in 2013 to 82% in 2014, before falling to 50% in 2017 and rebounding to current 68%-70% levels.

Planet Fitness’ Uniform earnings margin is weaker than you think, but its Uniform asset turns make up for it

Strength in Planet Fitness’ Uniform ROA has been driven by trends in Uniform earnings margin and Uniform asset turns.

After increasing from 28% in 2013 to 30% in 2014, Uniform margins decreased to 19% in 2017, before stabilizing at 31%-32% levels through 2019. Meanwhile, Uniform turns improved from 2.6x in 2013 to a peak of 2.9x in 2015, before compressing to 2.1x through 2019.

At current valuations, markets are pricing in expectations for Uniform margins to remain near peak levels coupled with a recovery in Uniform turns.

SUMMARY and Planet Fitness Tearsheet

As the Uniform Accounting tearsheet for Planet Fitness, Inc. (PLNT:USA) highlights, its Uniform P/E trades at 41.1x, which is above the global corporate average of 25.2x and its own historical average of 35.0x.

High P/Es require high EPS growth to sustain them. That said, in the case of Planet Fitness, the company has recently shown a 34% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Planet Fitness’ Wall Street analyst-driven forecast is a 30% EPS decline in 2020, followed by a 74% EPS growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Planet Fitness’ $86 stock price. These are often referred to as market embedded expectations.

Planet Fitness is currently being valued as if Uniform earnings were to grow 20% annually over the next three years. What Wall Street analysts expect for Planet Fitness’ earnings growth is below what the current stock market valuation requires in 2020 but above that requirement in 2021.

Furthermore, the company’s earning power is 11x the long-run corporate average. Also, intrinsic credit risk is 230bps above the risk-free rate, but cash flows and cash on hand are about twice its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a moderate dividend and credit risk.

To conclude, Planet Fitness’ Uniform earnings growth is above peer averages, therefore, as is warranted, the company is also trading above its average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com