MONDAY MACRO: According to this indicator, concerns about the Philippines’ default risk may be overblown

When talking about the credit quality of a country, the debt-to-GDP ratio is usually one of the most popular indicators. However, it shows just one side of the coin, missing a lot of the underlying factors we need to look at to see a more accurate picture.

Today, we highlight another indicator that seems more accurate and that is actually showing a safer credit profile than what people might think.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

In January 2021, Fitch announced that it is maintaining its investment grade ‘BBB’ rating for the Philippines and that it is forecasting a ‘stable’ outlook. The credit rating agency is expecting the Philippine economy to finally embark on its recovery.

Shortly after, Standard & Poor (S&P) reaffirmed its own investment grade ‘BBB+’ credit rating for the country, citing similar reasons for its stable outlook for the Philippines.

These rating agencies’ confidence in the Philippines is important in keeping good credit standing with the international community. It makes it easier for foreign investors and creditors to evaluate the risk involved when investing and lending money in the country.

However, newly released data for 2020 has some people worried about the country’s ability to recover in the coming months.

For one, news articles have popped up talking about the Philippines’ rising debt-to-GDP ratio. The debt-to-GDP ratio is considered a measure of a country’s ability to pay its debt, by comparing total obligations to annual output.

From 2004-2019, the Philippines’ debt-to-GDP ratio has been on a general decline, from 72% to 40%. While total debt kept growing, economic growth outpaced it.

That said, the debt-to-GDP ratio broke from this trend in 2020. The pandemic caused the Philippine economy to shrink in 2020, while at the same time forced the government to increase its borrowings to respond to the health crisis.

As a result, the Philippine debt-to-GDP ratio spiked to 55% in 2020.

Combined with the resurgence of COVID-19 cases in March and April 2021, some have begun to worry that debt-to-GDP will remain at current levels or begin trending towards historical peaks. The debt-to-GDP ratio is currently expected to further rise to 58.1% in 2021 and 59.9% in 2022.

If such a case does materialize, then Fitch and S&P might downgrade their rating and the Philippines may lose its investment grade status. The country’s growth will further be hindered if investors believe the country cannot pay its obligations.

However, the debt-to-GDP ratio doesn’t accurately portray the Philippines’ credit profile. There are reasons to believe the ratio is given too much importance, given its imperfections.

One problem is it fails to consider how much debt is owned by local creditors. Nearly 70% of the Philippine government’s debt is peso-denominated and only 30% are based on foreign currency.

Since the majority of obligations are in the Philippine government’s own currency, then in dire circumstances, the government can print money to pay off the debt. This creates severe inflation in the long term, but it is outweighed by the stability offered by a government not going into default.

Another problem of the debt-to-GDP ratio is that it gives the impression that sovereign debts are usually settled within a year. In reality, sovereign debts last for multiple years—even decades.

By the time a particular debt is fully paid, its proceeds would have already been used to generate economic growth. The tax revenues from the new investments would offset the debt’s borrowing costs.

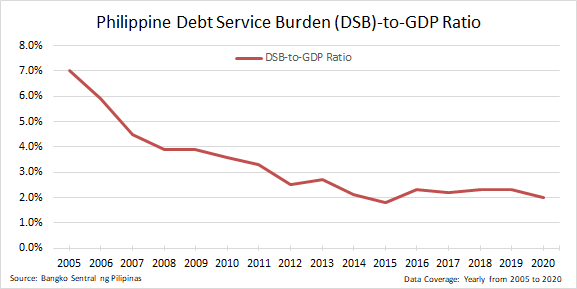

It’s more important to look at the principal and interest payments of the loan, to get a clearer picture of a government’s annual obligations. This is commonly known as the Debt Service Burden (DSB).

If we compare the Philippines’ DSB to its GDP, we see how safer the country’s credit profile actually is. Since 2012, the DSB-to-GDP ratio has remained near historical lows at 2% levels.

Furthermore, preliminary data shows that interest payments during January 2021 are 20% lower than in January 2020. If it is true, it may indicate the low borrowing costs of the Philippine government’s new loans, which further highlights the unlikelihood of default.

If Fitch or S&P do downgrade their credit rating of the country, the DSB-to-GDP ratio shows it won’t last long. For investors, there may even be security mispricing opportunities to capitalize on.

About the Philippine Markets Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com