MONDAY MACRO: Accounting distortions may have blinded investors on which companies are the most asset-efficient

One factor used to measure a company’s performance is how efficient it is in utilizing its assets. Computing a company’s asset turnover is simple, but removing the “dirt” on the financials of the company to get a more accurate result is another thing.

Uniform Accounting helps us to get a more accurate view of a company’s efficiency, as its methodology helps us get rid of the accounting distortions that may lead to poorer valuations.

Philippine Markets Newsletter:

The Monday Macro Report

Powered by Valens Research

We recently talked about the five Philippine companies with the highest Uniform return on assets (ROAs) that are trading on the Philippine Stock Exchange (PSE). In other words, these companies are the most efficient in generating profitability for every peso spent on assets.

Breaking the ROA computation down further, we get a company’s Earnings Margin (cost efficiency) and Asset Turns (asset efficiency)—two important metrics in understanding a company’s profitability. These main drivers of a firm’s ROAs tell where a firm is lacking and what it would likely need to do to expand ROAs.

A firm with high margins and low turns will likely find it easier to improve ROAs by evaluating its managing its operating costs better.

asset base. On the other hand, a business with low margins and high turns should look towards

Unfortunately, as-reported metrics provide a distorted view of a company’s margins and turns. Only through Uniform Accounting can we know what a company’s ROA drivers really look like.

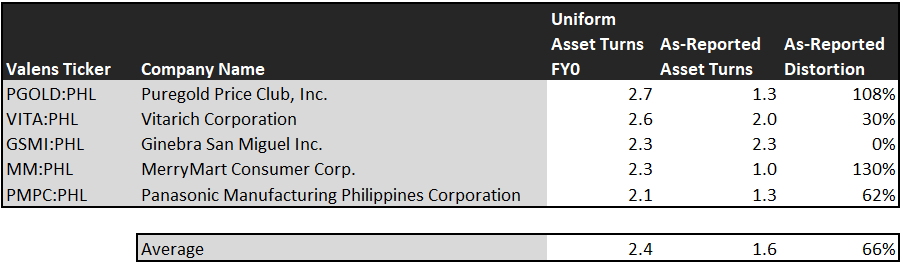

Today, we take a look at the top 5 companies with the highest Uniform asset turns in the PSE to see whether or not as-reported metrics make these firms appear weaker (or stronger) than they really are.

Thereafter, for the next couple of articles, we’ll focus on the top 5 companies with the highest Uniform earnings margin and then we’ll talk about how distortions in margins and turns have impacted the ROAs of these 10 companies.

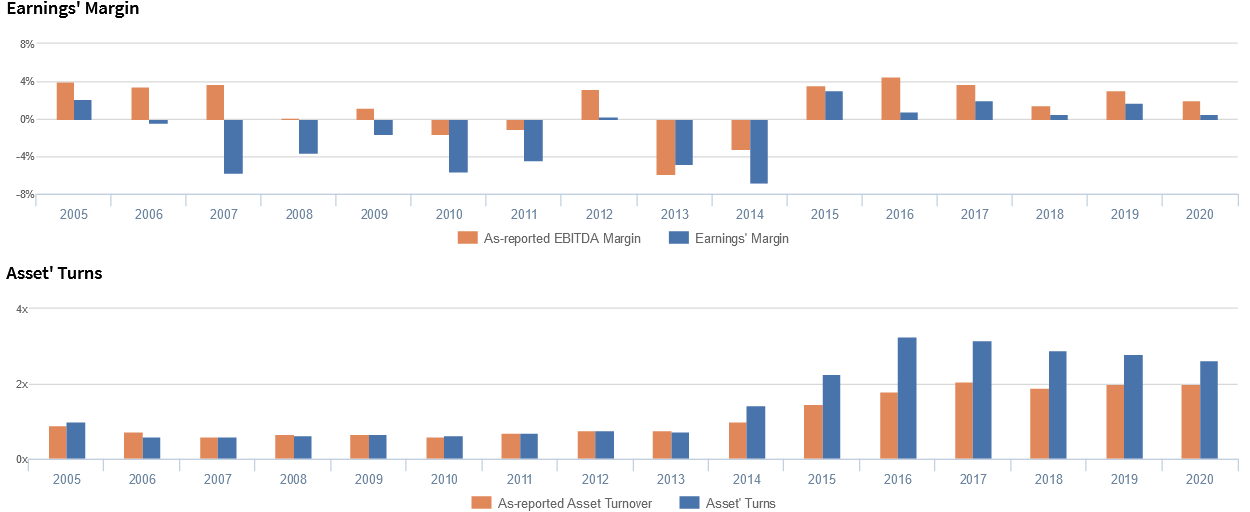

- Puregold Price Club, Inc. (PGOLD:PHL)

As of 2020, the most asset-efficient company in the PSE is Puregold Price Club, a well-known supermarket chain in the Philippines. Although Uniform margins have been historically lower than as-reported, its higher Uniform turns help push up its overall profitability.

One reason why asset turns are higher is the company has been holding a lot of cash in the balance sheet, more than what is operationally required. Another reason is Puregold’s balance sheet holds goodwill from the S&R acquisition. As readers of Valens’ work will know, goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance.

When we adjust for those two variables, along with other Uniform Accounting adjustments, we see how Puregold’s asset turns have led to strong Uniform ROAs.

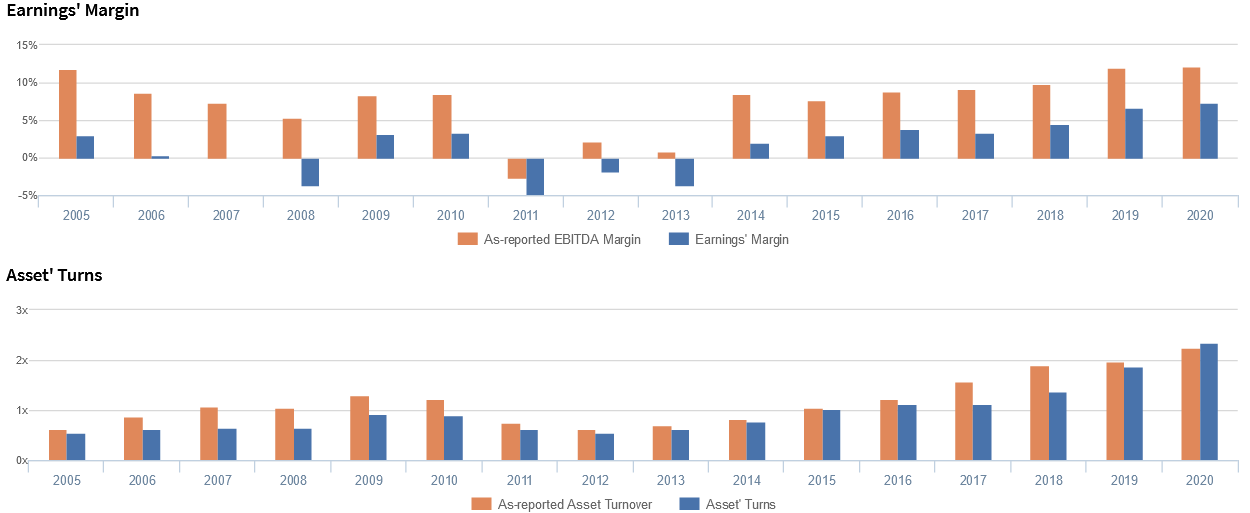

- Vitarich Corporation (VITA:PHL)

Second on the list is the animal feeds and poultry producer Vitarich Corporation, with 2.6x Uniform turns in 2020. The company has always focused on the modernization of its plants so its place on the list seems apt.

The firm’s corporate rehabilitation from 2007-2016 enabled the firm to ramp up sales growth and improve its working capital management, driving improvements in asset utilization.

That said, Vitarich has historically struggled to maintain profitability, due to its inability to manage raw material costs and the volatile prices of its product. If the company can find a way to address these problems, it would easily see ROAs improve.

- Ginebra San Miguel Inc. (GSMI:PHL)

Third, we have the famous liquor company Ginebra San Miguel, which enjoys its position as the largest gin brand in the largest gin market in the world.

Ginebra earned its status by providing affordable gin to Filipinos. While this has led to high sales volumes, it does place a cap on the margins the business can achieve. Coupled with the new excise tax structure for alcohol products, the company might need to continue relying on turns for its ROA expansion.

This is one instance where as-reported metrics got it right.

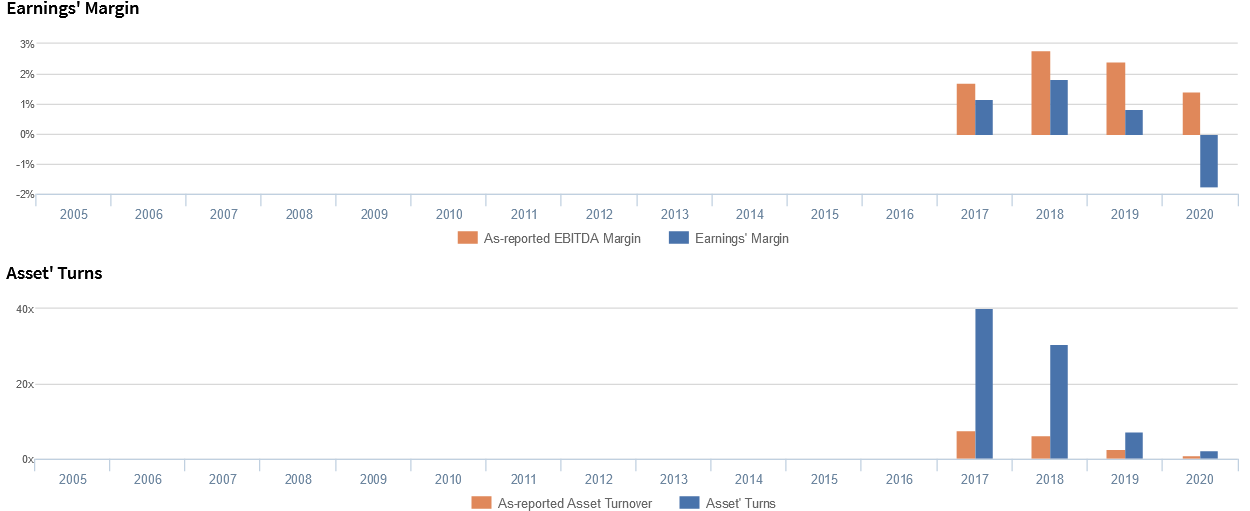

- MerryMart Consumer Corp. (MM:PHL)

With 2.3x Uniform turns in 2020, MerryMart scores fourth on this list. As a recent IPO, it’s normal for the company to have high asset turns, due to the large amount of excess cash still sitting in its balance sheet.

However, given MerryMart’s store expansion plans, Uniform turns will likely decline further over the next few years. The company also has plans to open up to franchising, an asset-light business model, but it’s still a small chunk of the business.

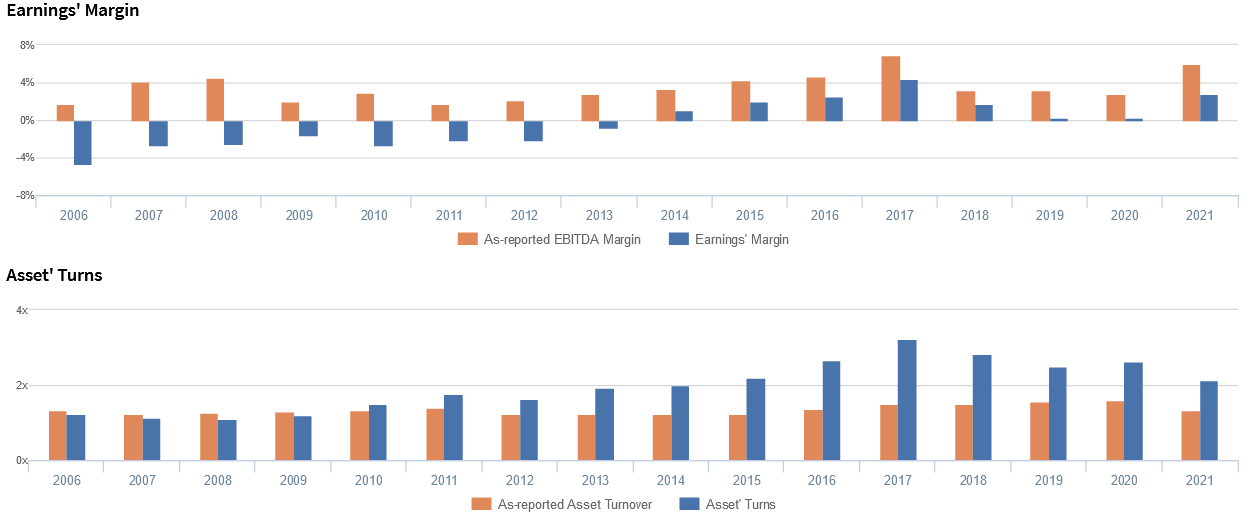

- Panasonic Manufacturing Philippines Corporation (PMPC:PHL)

Completing the top 5, we have home appliance manufacturer Panasonic Philippines, with 2.1x Uniform turns. The company’s sales have struggled during the pandemic, falling by 9%.

That said, the company was still able to generate high asset turns. Its relationship with Panasonic in Japan has enabled the company to spend little in factories, despite operating in the manufacturing business.

Instead, it imports many of its raw materials, equipment, and products from its affiliates. As a result, unlike many of its competitors, Panasonic Philippines’ balance sheet is mostly made up of working capital.

Looking at the as-reported margins and turns of the companies above, one would have arrived at the wrong conclusion of what was driving their ROAs.

In four of the five companies, Uniform turns were actually 30%-130% higher than as-reported metrics claim. Although there were few accounting distortions in the case of Ginebra San Miguel’s turns, we see how large the distortion is for its margins.

Using the right asset turns calculations to assess companies’ profitability is important, especially when looking at companies whose business models push for larger volumes versus larger margins per unit sold. When we don’t make these Uniform Accounting adjustments, we will more often than not dismiss companies with low profit margins as low-quality companies.

Next week, we take a look at the top 5 companies in terms of margins and see whether or not as-reported financials have also gotten their performances wrong.

About the Philippine Markets Newsletter

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com