MONDAY MACRO: At nearly optimal 85% capacity utilization rate, capex spending is necessary to maintain 6% Uniform ROA despite COVID-19’s global scare

The coronavirus disease 2019 (COVID-19) generated a global panic, negatively affecting global economies as travel and transportation take a heavy hit, especially in China.

In the past few weeks, the COVID-19 scare has contributed to the Philippine stock market tumbling despite preliminary assessments from the Bangko Sentral ng Pilipinas (BSP) showing that any impact on the country’s 2020 growth will be minimal.

The metric we highlight below shows that even with the potential slowdown in exports to China, Philippine economic growth is still attainable.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

The COVID-19 is a new respiratory virus that originated in Wuhan, Hubei Province, China. Some genetic analyses have suggested that this virus is a relative of the Severe Acute Respiratory Syndrome coronavirus (SARS-CoV) that resulted in more than 8,000 cases globally in 2002-2003.

When the World Health Organization declared the COVID-19 outbreak an international emergency in late January 2020, quite understandably, fear and panic ensued.

Not everyone had immediate access to information about the deadly virus, and any information available was usually met with distrust. Were these the real numbers or were governments significantly understating the threat?

The fear of the unknown has impacted stock markets around the world as investors tend to expect the worst. The Philippine stock market was not an exemption.

Share prices on the PSEi had been on the downtrend in the past weeks. It was only last week when it rebounded with a 4% rally as the world started to become more optimistic that the spread of COVID-19 has reached its peak and will no longer pose a major global problem.

Economists and the Philippine government forecast the economic impact of the disease on the country with a possible slight reduction in domestic growth of about 20bps in Q1 2020, and 40bps in Q2 2020.

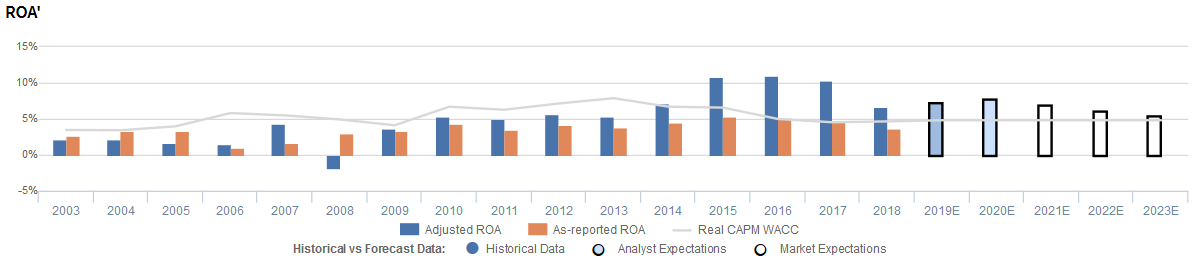

Though the market is concerned about this limited impact of the outbreak in the country’s target growth, Uniform Accounting continues to show that growth is still warranted despite the market’s current fears.

Last week, we took a look at the impact of the Net/Gross PPE ratio, which is a great proxy to identify how many old assets a company has. We linked this to growth expectations for Philippine companies and how, using Uniform Accounting, we see that investments in assets have been growing in recent years.

We also touched on capacity utilization last week. We’ll discuss a bit more on this metric today.

The capacity utilization rate is used to determine how much slack is currently in the system in terms of capacity to increase volumes without spending on capex. Companies operating at 85% capacity utilization are normally considered as operating at an optimal rate.

From 1999 until 2019, capacity utilization in the Philippines averaged 81%. After falling to 78% in January 2009, capacity utilization bounced back to 80% levels later that year.

Since reaching 83% levels in 2012, there has been very little change in capacity utilization in the Philippines. At 84.5% in November 2019, Philippine companies are nearing the optimal rate.

When businesses don’t actively spend on improving production capacities, they run the risk of either overworking their available fixed assets or increasing inefficiency in their production schedule.

Without additional investments in fixed assets, companies lose out on potential opportunities to grow their business. These capacity constraints, after all, will limit their growth prospects.

According to the Philippine Statistics Authority, 65% of the major industries in the Philippines operated at over 80% capacity utilization. Petroleum products recorded the highest average capacity utilization in September 2019, at 89.9%.

This means that in order to facilitate incremental growth in the Philippines, capex spending is very likely.

The capacity utilization rates for the Philippines’ major trading partners have had mixed performances from 2018.

US total capacity utilization reached 80% in late 2018, but has subsequently fallen off to 77% levels, towards the middle of 2019, indicating delay in capex spending.

Meanwhile, China’s industrial capacity utilization increased by around 40bps. At 76.4% in Q3 2019, China will strengthen management and oversight will be implemented in order for rates to return to appropriate levels.

As Uniform ROA highlights, Philippine corporate profitability would improve in a low interest rate environment. Together with the low credit risks that the Philippine market is experiencing, these all warrant the GDP growth rate even with concerns surrounding the COVID-19 outbreak.

About the Philippine Markets Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com