MONDAY MACRO: Borrowers’ financial struggle is still in the system

We’ve discussed and reached the consensus that the Philippine economy has successfully rebounded from the COVID-19-induced lockdowns, entering a new phase of the economic cycle. Both consumers and businesses appear to exude confidence in this revival.

In light of this positive outlook, it’s prudent to turn our attention to the state of the overall Philippine banking system, with a specific focus on its debt structure.

Philippine Markets Newsletter:

The Monday Macro Report

Powered by Valens Research

To obtain an understanding of the general financial health of the Philippine banking system, one effective method is to examine its distressed asset ratio.

Before delving into the interpretation of the distressed asset ratio, let us define what a distress asset is and what are the different variables into the distressed asset ratio calculation:

A distressed asset is an asset that faces challenges in sustaining its value. For banks, it usually refers to assets where borrows default or issuers are financially struggling or facing bankruptcy.

As per the BSP’s definition, it encompasses the total of non-performing loans (“NPL”), real and other properties acquired (“ROPA”), gross non-current assets designated for sale, and performing restructured loans.

NPLs are loans where borrowers have failed to make their periodic payments, raising doubts about their capacity to repay both the principal and interest in full. We discussed this topic in one of our reports last May.

ROPA comprises real estate assets that have come into the possession of the bank due to the failure of borrowers to meet their loan obligations. The primary objective for the bank in regard to these properties is their eventual sale to recover the outstanding debts.

Moreover, gross non-current assets represent assets that a bank intends to divest in the near future. These assets encompass items such as real estate properties, equipment, and investments that the bank currently possesses. The decision to sell these assets is driven by the bank’s strategic objectives or responsive measures to adapt to evolving market conditions.

Lastly, performing restructured loans are loans that were in trouble but have been adjusted by the bank, and now the borrowers are making regular payments. They’re monitored due to their past issues and potential future risks.

Now, the distressed asset ratio shows the portion of risky assets in relation to the bank’s total loans and real estate properties, without considering potential losses.

It basically helps investors assess the bank’s financial stability. Take a look…

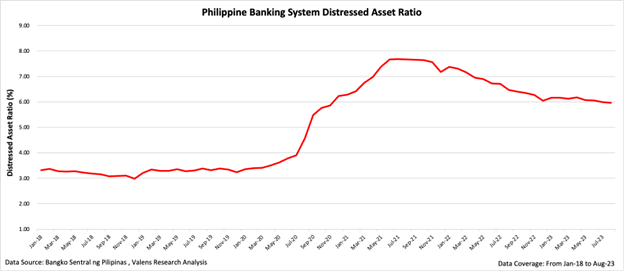

Following the initial data recording in 2008, when the financial crisis in the US started to materialize, the ratio stood at 12%. Since then, it exhibited a gradual decline, maintaining relative stability within the 3% to 4% range from 2014 to 2019. However, the onset of the pandemic marked a remarkable surge in this ratio.

The peak occurred in July 2021, reaching 7.68%. This means that this portion of the total loans faced challenges, including borrower defaults or the need for refinancing or restructuring due to financial difficulties or an inability to meet their payment obligations.

While showing improvement from its peak during the pandemic, it remains relatively high compared to pre-pandemic levels, ticking at 5.96% in August of this year. While it currently surpasses the pre-pandemic levels, it falls short of the pre-pandemic average of 6.16%.

This persistence is due to several factors: the enduring economic fallout from COVID-19, time-consuming distressed asset resolution, sectoral variations in recovery rates, diminishing government support measures, and banks’ strategies to manage distressed assets.

The distressed asset ratio in the Philippine banking system sheds light on the enduring impact of the COVID-19 pandemic. While various economic indicators convey optimism and a positive outlook, the financial challenges faced by businesses and borrowers have left a lasting imprint on the Philippine banking landscape.

About the Philippine Markets Newsletter

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com