MONDAY MACRO: Despite rising inflation and peso depreciation, this indicator suggests investors are not yet seeking shelter in risk-free assets

When there are concerns about an economic recession, investors often look to this one indicator. In the US, its predictive power right before a recession is quite astounding. We apply this indicator to the Philippine context to help analyze what it could mean for the Philippine economy in the coming months.

This fixed-income-based indicator is suggesting clear skies for the Philippine economy, despite the many macroeconomic headwinds that are indicating otherwise.

Philippine Markets Newsletter:

The Monday Macro Report

Powered by Valens Research

The Bangko Sentral ng Pilipinas (BSP) is tasked with maintaining price stability conducive to a balanced and sustainable growth of the economy and employment. To do this, they employ controls on the economy in areas such as interest rates and treasury yields.

Treasury bond yields are often used as the risk-free rate by investors when they value assets, as nearly all investors would agree the government is the least likely borrower to default on its payments. Historically, the Philippines has never defaulted on its debts, save for a 90-day debt moratorium in 1983 to foreign creditors.

Because these bonds are issued by the government, when it starts running a deficit, the government can either print more money or raise national revenue by increasing taxes. Generally, governments are less likely to default, which explains why investors are willing to buy these securities despite their generally low returns.

In addition, treasury bond yields are used to measure upcoming economic cycles. Bond yields are the returns from government debt obligations. These securities range from 3 months up to 10 years, and act as a reflection of bondholder sentiments for the country’s economy.

Investors often note the difference between short-term and long-term bonds to be important in assessing bondholder sentiment.

Normally, shorter-term bonds offer lower yields while longer-term bonds offer higher yields because investors need higher returns to be incentivized to hold onto an investment over a longer period of time. Therefore, economic optimism is expressed by a rising long-term yield.

Moreover, a rising yield signals economic optimism because investors are pulling their capital out of government bonds to invest in other asset classes. Investors are willing to move their capital to riskier assets because they believe in the economy.

When long-term yields begin to decline, it may be a signal that investors should start looking for other signs of slowing economic growth.

The consequence of such an investment thesis would be lower treasury bond yields. As demand for a bond pushes up the price closer to face value, the return on the bond would fall as well.

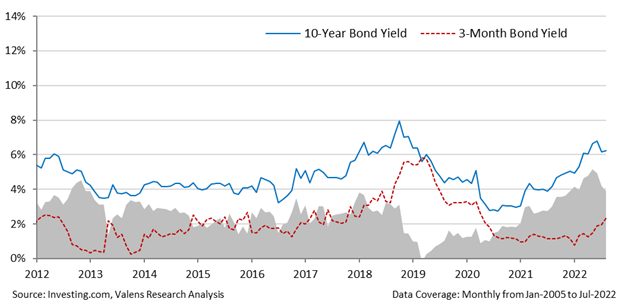

10-year bonds briefly fell to a level lower than 3-month bond yields in February 2019 before quickly recovering. For a brief moment, the yield curve inverted, signaling a potential recession at the time.

However, continued subsequent declines in treasury bond yields for both the 10-year and 3-month yields suggested investor confidence.

Following a series of economic shocks and other events including a global pandemic, yields further decreased until the latter part of 2020 as investors saw a capital flight toward safer assets such as government securities. At the time, investors were spooked even by gold as an asset given the questionable performance at the start of the pandemic.

As 2021 started, the 10-year bond yield started increasing from 3% in January 2021 to 6.2% in July 2022 while the 3-month bond yield remained between the 1%-2% range over the same time period.

The rising spread may signal investor optimism as the higher yield signals declining demand for safe assets in the long term. In other words, investors are finding investments worthy of their capital despite rising interest rates, inflation, and a plateauing GDP.

As fixed income and equities are often said to compete for capital, this signal for treasury bond yields could potentially signal strength in the Philippine economy.

About the Philippine Markets Newsletter

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com