MONDAY MACRO: Here’s how the PSE-listed companies’ profitability really fared in 2020

With the majority of PSE-listed companies having already filed their 2020 annual reports, it would be interesting to see how the group had performed during the recessionary year.

As expected, ROAs dropped in 2020. However, the PSE-listed companies still performed better overall than you might think. Under the Uniform Accounting framework, Philippine companies have been generating higher ROAs than what as-reported metrics are reflecting.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

In analyzing a company’s fundamentals, return on asset (ROA) is one of the most common metrics to look at. It is based on a simple formula (net earnings divided by total assets), and assuming you use the right numbers, this metric tells a lot about a company.

ROA is essentially a measure of a company’s operational efficiency. In other words, it quantifies how well a company makes a profit from its investments–how much earnings the company gets for every peso of assets.

Oftentimes, the most attractive companies for fundamental investors are those that can either sustain a high ROA or improve its current ROA, because it shows that the company is thriving in the marketplace.

The largest company isn’t necessarily the best company to invest in, as it may be spending its capital and debt recklessly.

For companies listed in the Philippine Stock Exchange (PSE), ROAs have varied widely for each firm. Some have been performing consistently well, while some have hardly been able to turn a profit.

However, it would be interesting to see how the PSE-listed companies have performed, in the form of their aggregate ROA. This offers two benefits.

First, it helps give a picture as to whether the Philippine equities market has been worth investing in, based on a 6% global corporate average ROA.

Second, it can also be a measure of the Philippine economy’s health, given the significant influence PSE-listed companies have in the economy. Many of the largest companies in the country such as SM, Ayala, and JG Summit are also publicly traded.

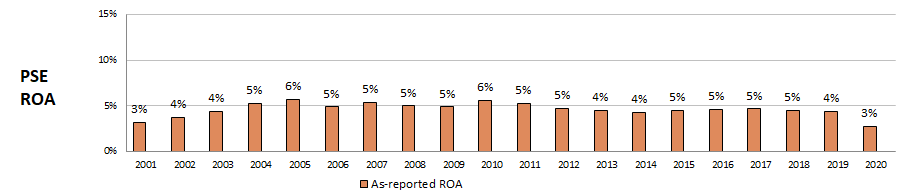

Based on as-reported metrics, Philippine corporate ROAs have mostly struggled to match global corporate averages of 6%, recording only 6% ROAs in 2005 and 2010. Excluding those years, as-reported ROAs have remained at 4%-5% levels from 2002-2019, or at cost-of-capital levels.

Then in 2020, as-reported ROA dropped to 3% in 2020, its lowest since 2001.

The performance in 2020 is troubling, though expected. The COVID-19 pandemic was the main news story for much of the year, as it drove the country into its first recession since 1998. Nearly every economic activity was disrupted by the pandemic, likely causing a permanent impact on how people live.

Even if we write off 2020, as-reported ROAs tell us that publicly traded Philippine corporations have not been effective at generating returns.

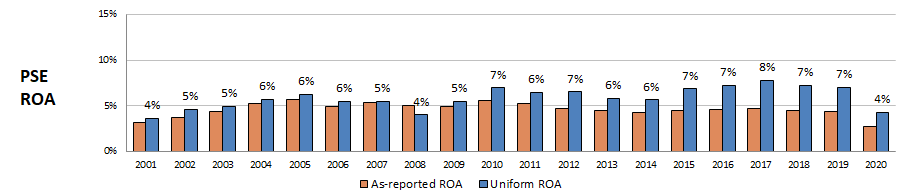

However, when removing the accounting distortions found in each company’s financial statements, we see quite a different trend. The Uniform ROA of Philippine corporates has actually been more cyclical, but generally improving over time.

From 2001-2009, Uniform ROA was somewhat similar to as-reported ROA, but the disparity started to grow from 2010 onwards. Specifically, Uniform ROA mostly ranged from 6%-7% levels in 2010-2019 and even rising to a peak of 8% in 2017, before falling to 4% in 2020.

From 2010-2019, Philippine corporates had begun to consistently perform near or above the 6% global corporate average, implying that the group had been fruitful for investors. Looking at the PSE All Shares Index, its price had more than doubled over the same timeframe.

Furthermore with Uniform data, the chart now also properly reflects the Philippine economy’s robust growth during 2010-2019. The decade saw Philippine GDP grow at an average of 6.4%.

As such, as-reported ROAs have been severely understating the aggregate performance of the PSE-listed companies, downplaying its attractiveness as an investment and also the improving macro fundamentals of the Philippine economy.

While Uniform ROAs also saw a decline in 2020, the recovery back to 6%+ levels may not be as difficult as initially thought, considering that true aggregate ROA is actually 4%, and not 3% as-reported.

About the Philippine Market Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com