MONDAY MACRO: Holiday season and lenient guidelines push consumer spending higher, but 3.3% inflationary pressure not yet a concern

People normally look at this economic indicator to decide how good or how bad the economy is doing. The higher it is, the more worried consumers get because of rising prices of goods and services.

However, we should remember to use the mosaic approach when dealing with this economic indicator–we need to look at the other indicators influencing it in order to understand how the economy is really doing and what can be expected going forward.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

In 2018, the BSP increased interest rates five times to manage the rising inflation rate due to the Tax Reform for Acceleration and Inclusion (TRAIN) Act.

Then, in 2019, the BSP decided to cut rates to spur economic growth once inflation had finally stabilized. A low interest rate environment can significantly boost the economy because of lower borrowing costs, and businesses are more likely to expand their operations when the cost of acquiring funds is cheaper.

The three rate reductions that year resulted in interest rates that were 75bps lower compared to 2018.

This year, the BSP has once again cut interest rates to help businesses get back on their feet to expedite the country’s economic recovery. The latest 25bps cut in November is the fifth one for the year, leading to an all-time low rate of 2%.

However, even with interest rates already 200bps lower than last year’s, we still need to see an increase in banks’ willingness to lend (and an increase in demand to borrow) together with improved consumer spending.

The Q3 2020 Senior Bank Loan Officers’ Survey (SLOS), a quarterly survey from the BSP that illustrates banks’ lending behavior, shows that banks have been hesitant to lend even with all the incentives from the BSP. Though fewer banks further tightened their credit standards, we have yet to see this translate to much higher lending activities.

That said, even if we’re currently in a favorable lending environment, we still need to take a look at the consumer side of things. Companies will only be able to survive and thrive if consumer spending picks up.

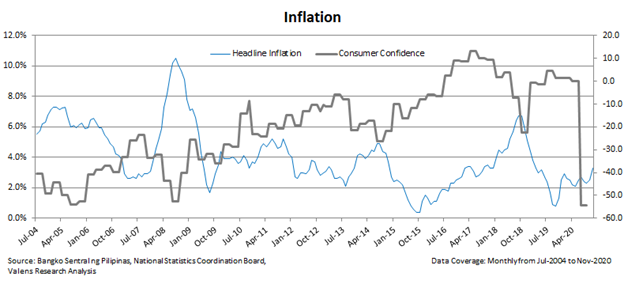

The Consumer Confidence Index (CCI), which is the degree of optimism consumers have on the economy, dropped sharply to a new low of -54.5% in Q3 2020. Lower consumer confidence means people are less likely to spend and are more likely to save what they have now.

As a leading indicator of inflation, a low CCI is telling us to expect inflation to remain at generally low levels. As consumers are not spending, there isn’t much driving up prices too high.

This relationship has generally held in the past, but we have to remember the circumstances now are a little bit different, especially with more than one black swan event in Q1 2020.

The pandemic abruptly temporarily halted business operations and activities in major cities in the country, causing unemployment levels to unexpectedly spike. In addition, it caused consumer confidence to drop to negative territory in Q3 2020 (Note: There was no Q2 2020 data gathered because of movement restrictions, so we aren’t able to tell how quickly or massively consumer confidence moved Q1 to Q3 figures.).

However, more cities are now starting to open up as travel restrictions have eased, which means we should be expecting some economic activities to slowly return to pre-pandemic levels.

As consumers start spending to go out, leading to higher demand for goods and services, we should see inflation rise even if we don’t see consumer confidence improving yet. This return to work and the opening of cities to tourists are one of the reasons why the inflation rate increased to 3.3% in November from 2.5% in October.

Another reason for the higher inflation rate in November is the back-to-back typhoons that disrupted the food supply chain in certain provinces, and the African Swine Fever (ASF), causing price increases. Additionally, those affected by the typhoons will now be forced to spend it on rehabilitating their homes.

This level of inflation is slightly higher than the BSP’s forecast of 2.4%-3.2%, where it will likely settle by 2022 because of the long-term effect of the pandemic on the economy.

This higher inflation rate is not a reason to worry about the Philippine economy, as long as it remains in its current range. Even though many businesses have closed, there are still a lot that have turned to non-brick-and-mortar platforms to survive. For example, many businesses have turned to online platforms. This reached over 700,000 registered online businesses, a 12% increase compared to approximately 600,000 last year.

With the holiday season coming in just a few days, businesses are more prepared than ever since the pandemic started. This increase in business activities should help hasten the Philippines’ economic recovery.

About the Philippine Market Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com